Key takeaways

- SWIFT sends secure messages, it does not move money, your funds travel through correspondent banks that can deduct fees at each hop.

- Nostro accounts at intermediary banks are a major source of deductions, each hop can cost $15 to $50.

- Understand the three charge code options to control who pays fees, OUR protects your full invoice, SHA and BEN lead to unpredictable shortfalls.

- Fewer intermediaries mean fewer deductions, routing chosen by the sender’s bank determines how much you actually receive.

- Use local rails like ACH, SEPA, FPS via virtual currency accounts to bypass SWIFT, eliminate nostro hops, and cut costs.

- When SWIFT is unavoidable, insist on OUR, provide precise details to avoid repair fees, and request gpi tracking for transparency.

- Manage FX actively, receive in the original currency first, then convert at better rates, and consolidate invoices to reduce per transfer overhead.

- Automate compliance with e-FIRA and correct purpose codes, platforms built for Indian freelancers simplify documentation and reduce costs.

Understanding SWIFT, it is just messages, not money

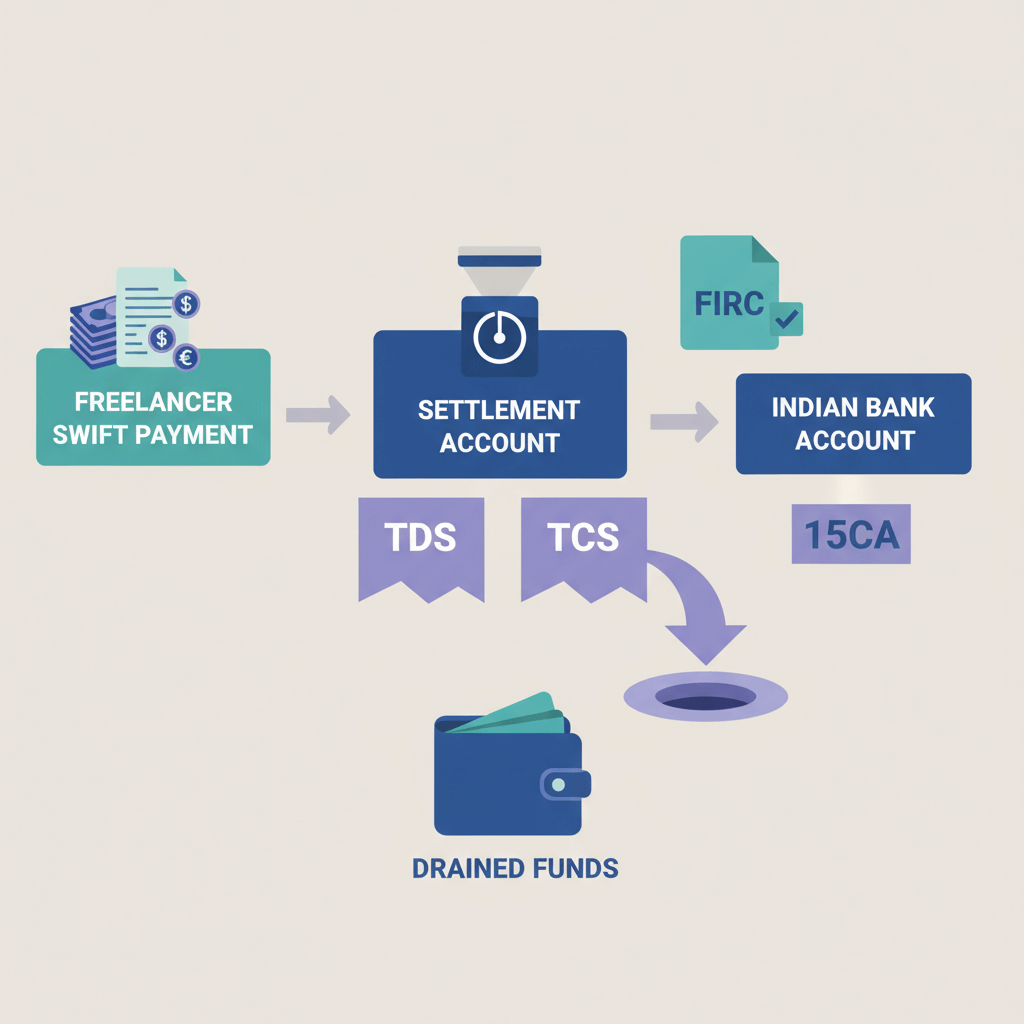

Here is something most freelancers miss, SWIFT is a secure messaging network, not a value transfer system. Your client’s bank sends instructions, correspondent banks execute settlement across accounts, and your Indian bank credits you after conversion.

Think of SWIFT like WhatsApp for banks, the message says, credit $1,000 to this account in India, the actual money moves through correspondent relationships.

A typical cross border payment involves the sender’s bank, one or more intermediary correspondent banks, and your beneficiary bank in India. Each stop can levy fees, which is why your $1,000 invoice may arrive short.

Who pays what, charge codes explained

Before nostro accounts, you need the basics on charge codes, see the three charge code options.

- OUR, the sender pays all fees, you receive the full amount.

- SHA, fees are shared, your client pays their bank’s charges, intermediaries deduct from your payment.

- BEN, you bear all fees, the worst outcome for freelancers.

With SHA or BEN, intermediary deductions happen before the funds reach your account, which is why $1,000 can land as $978 or less.

What is a nostro account and how it drives up fees

A nostro account is a foreign currency account your bank holds with a bank abroad. Your Indian bank uses a USD nostro in New York, a GBP nostro in London, and so on, to move funds along local rails and settle transactions.

Every time your payment passes through a correspondent bank’s nostro account, that bank can trigger deductions such as maintenance recovery, lifting fees, handling and compliance charges. More hops, more deductions.

Direct correspondent ties might mean one hop, a complex route can mean two or three, potentially $15 to $50 per hop.

Breaking down the costs, three types of charges

Nostro fees

Charges by correspondent banks for using and maintaining their foreign currency accounts, often blended into deductions or FX spreads. Typical range, $15 to $30 per hop.

Intermediary charges

Lifting or handling fees for routing, screening, and repairs when message data is incomplete. Typical range, $15 to $50 per intermediary.

Receiving bank fees in India

Your bank’s inward remittance fee plus an FX markup, often 2 percent to 5 percent over mid market rate. Typical range, ₹500 to ₹1,500 flat, plus spread.

Example cascade with SHA, client sends $1,000, one intermediary lifts $20, your bank receives $980, applies processing plus 3 percent FX markup, you land well below your expected INR amount.

Routing 101, why the path your payment takes matters

Routing is the sequence of correspondent banks your payment traverses. The sender’s bank chooses the path based on relationships, corridor norms, speed, and their own costs. More hops mean more deductions and potential delays due to cut off times across time zones.

You usually cannot control routing as a recipient, which is why shifting clients to local rails like ACH, SEPA, or FPS removes the entire routing problem.

Why fees vary wildly between identical transfers

- Bank relationships and pricing, different correspondent deals change costs.

- Charge code selection, a mistaken BEN instead of SHA can swing the outcome.

- Amount thresholds, flat versus percentage fees change at certain levels.

- Corridor norms, USD to INR may need more hops than EUR to INR via SEPA linked banks.

- Message errors, repairs add $10 to $50.

- Compliance screening, false positives can delay and add costs.

- FX spreads, your bank’s markup moves with volatility and liquidity.

Even with gpi tracking, you typically see fees only after each hop, not before the transfer.

Worked examples, what actually gets deducted

Example A, USD $1,000 SWIFT SHA from a US client

Client sends $1,000, the New York correspondent lifts $20, your Indian bank receives $980, charges inward fees, converts with a 3 percent markup. Net INR is roughly ₹80,000 to ₹80,500 when the mid market is ₹82, a material shortfall versus expectation.

Example B, GBP £1,000 from a UK client

SWIFT SHA, London correspondent lifts £15 to £30, you receive around £960 to £970 equivalent in INR after local fees and FX.

Local rails alternative, client uses FPS to a virtual GBP account, zero intermediaries, you get the full £1,000, then convert at transparent rates. The difference is stark.

Visualize it, SWIFT shows multiple fee boxes between client and you, local rails show a direct line.

Charge code comparison

| Option | Sender pays | Recipient gets | Best for |

|---|---|---|---|

| OUR | All fees including intermediaries | Full invoiced amount | Predictable net receipts |

| SHA | Sender’s bank charges | $970 to $980 after deductions | Compromise, but variable |

| BEN | Minimal or none | $950 to $970 after deductions | Avoid if possible |

How to reduce or avoid unpredictable SWIFT deductions, step by step

Step 1, default to local payment rails

- ACH in the US to your virtual USD account, low cost, one to two business days.

- SEPA in Europe to your virtual EUR account, free or minimal, same day to next day.

- FPS in the UK to your virtual GBP account, instant to a few hours, no intermediary deductions.

No correspondent banks, no nostro hops, no mystery shortfalls.

Step 2, use payment links for cards and bank transfers

For clients who prefer cards or local transfers, send a payment link, you get transparent, flat pricing instead of variable SWIFT deductions.

Step 3, when SWIFT is unavoidable, insist on OUR

Put it on the invoice, “All bank charges to be borne by sender, OUR.” Explain it ensures you receive the full amount, which simplifies reconciliation.

Step 4, provide precise payment details to avoid repair fees

- Correct SWIFT or BIC.

- IBAN where applicable.

- Registered address exactly as per bank records.

- Correct purpose code for services export.

- Reference or invoice number as required.

Double check your name, even minor mismatches can trigger compliance holds.

Step 5, match currency to minimize conversions

Receive USD to USD first, then convert at better rates. A multi currency account lets you hold funds, watch rates, then convert when favorable, often saving 2 percent to 4 percent.

Step 6, consolidate invoices

Bill monthly instead of weekly, you pay the nostro and SWIFT overhead once, not four times.

Step 7, confirm routing and request gpi tracking

Ask for the correspondent route and gpi reference. You gain real time visibility, faster dispute resolution, and a clear audit trail.

India specific solution, use platforms built for freelancers

Platforms designed for Indian freelancers provide local receiving details in USD, GBP, EUR, CAD, so clients pay via ACH, FPS, or SEPA, bypassing SWIFT entirely. You avoid intermediary and nostro deductions, enjoy flat fees, mid market FX, and quick INR settlement. Automated e FIRA generation, WhatsApp updates, and dashboard reconciliation cut paperwork and delay.

Compliance and documentation for Indian freelancers

Every SWIFT inflow routes through authorized dealer banks under RBI and FEMA. Your role is to keep records clean and timely.

- Purpose codes must match the service exported.

- e FIRA should be obtained within 24 hours of credit for your tax files.

- Maintain supporting docs, invoices, contracts, emails, payment confirmations.

- KYC readiness, PAN, masked Aadhaar, recent bank statements, and proof of business like a portfolio or freelance platform profile.

Modern platforms automate e FIRA and reconciliation, saving weeks compared to traditional branch based processes.

Quick checklist, before, during, and after payment

Before invoicing

- Prefer ACH, SEPA, FPS over SWIFT.

- Specify OUR if SWIFT is used.

- Share exact beneficiary details, no abbreviations.

- Confirm the client’s bank supports the chosen method.

Before client sends payment

- Verify expected route, ask for gpi reference.

- Test with a small transfer for first time payers.

- Align on timelines, ACH one to two days, SWIFT three to five days.

After receipt

- Reconcile net amount against invoice and expected fees.

- Investigate unusual shortfalls with gpi and MT103.

- Download and file e FIRA promptly.

- Record actual fees to refine pricing for future work.

Protect your earnings by understanding the payment chain

Nostro accounts are invisible until they eat into your invoice. Each correspondent hop is a chance for deductions, which compound across your annual foreign income. Default to local rails where possible, insist on OUR when SWIFT is required, provide precise details, consolidate invoices, hold and convert currency smartly, and use tools that automate compliance.

Audit your current flow, calculate what you lose to nostro and intermediary charges each month, then try local rails on the next invoice. Your net receipts will improve immediately.

Your work has value, keep more of it. Platforms like Karbon Business, Wise Business, and Payoneer exist to replace legacy processes with transparent, predictable outcomes.

FAQ

How do SWIFT and nostro account fees actually reduce my freelance payment in India?

When your client sends an international wire, the payment moves through correspondent banks that hold nostro accounts. Each intermediary can deduct lifting or maintenance fees, then your Indian bank applies inward charges and an FX markup. Together, these reduce your net INR receipt, especially on SHA or BEN charge codes.

Which charge code should I ask my client to use to make sure I get the full amount?

Request OUR, it makes the sender pay all bank and intermediary fees, so you receive the full invoice. If your client insists on SHA, budget for 2 percent to 3 percent deductions. Avoid BEN because it pushes almost all costs to you.

Is there a way to receive USD, GBP, or EUR without SWIFT deductions to my Indian account?

Yes, ask clients to pay via local rails to virtual accounts, ACH for USD, FPS for GBP, SEPA for EUR. For example, with Karbon Business you can share local account details, the client pays domestically, and you avoid SWIFT and nostro hops entirely.

What is MT103 and how can it help if I receive less than expected?

MT103 is the standardized SWIFT payment message. A copy shows sender amount, charge code, and deductions at each intermediary. Share it with your client and your bank to trace shortfalls and verify who deducted what, it is crucial for resolving disputes.

How do I politely tell a new US client to select OUR on their wire form?

Add a clear line on your invoice, All bank charges to be borne by sender, charge code OUR. In your email, explain that OUR ensures you receive the full amount, which simplifies accounting and prevents month end reconciliation delays.

ACH versus SWIFT for Indians, which is better for freelancers?

ACH is usually better for USD because it is domestic, low cost, and avoids intermediaries. SWIFT is only necessary when a client cannot use ACH. With a platform like Karbon Business you can receive USD via ACH into a local USD account, then convert to INR at mid market rates.

How can I reduce FX loss when converting from USD to INR?

Receive in USD first, hold funds for a short period, then convert when rates are favorable at a platform that uses mid market rates with a transparent fee. This approach can save 2 percent to 4 percent versus immediate conversion at a bank’s retail spread.

Can I avoid repair fees and delays, what exact details should I share with clients?

Share precise beneficiary name as per bank, correct SWIFT or BIC, IBAN if required for EUR, full registered address, purpose code for services export, and invoice reference. These details reduce manual repairs, which otherwise add $10 to $50 and delay credits.

Is Karbon Business compliant for Indian freelancers receiving international payments?

Karbon Business is built for Indian exporters of services, it supports purpose codes, generates e FIRA for every eligible payment, and settles INR within standard timelines. This helps with RBI and FEMA compliance while reducing manual paperwork.

How do I estimate how much a SHA transfer will short pay me?

As a rule of thumb, expect 2 percent to 4 percent total deductions on SHA transfers, combining intermediary fees and FX spread. Amount, corridor, and routing will influence the final figure, so confirm with gpi tracking and MT103 after the transfer.

Should I consolidate multiple small invoices to cut fees?

Yes, consolidating weekly invoices into a single monthly invoice reduces per transfer overhead. If you pay $20 to $40 in intermediary fees per payment, merging four transfers into one can save $60 to $120 each month.

What documents should I keep for taxes and audits when I get paid from abroad?

Maintain invoices and contracts, bank credit advice, MT103 copies for SWIFT payments, and e FIRA for each inward remittance. These records prove the source and nature of funds, and they simplify income tax filing for freelance export income.