Key takeaways

- Correspondent bank charges are the hidden fees deducted as your client’s international wire hops through intermediary banks, they explain why your credited INR is lower than expected, as detailed in the Razorpay guide on inward remittance charges.

- Four cost layers typically hit Indian freelancers, intermediary fees, the lifting fee, FX spread, and the charge code setting in the SWIFT message, together they can total 3 percent to 5 percent per payment.

- Reading the MT103 reveals who handled your payment, which banks deducted fees, and whether charges were OUR, SHA, or BEN.

- Insist on OUR in Field 71A to push intermediary fees to the sender, then minimize your FX and lifting fee exposure with smarter routing or non SWIFT rails.

- Skip SWIFT when you can, receive via local rails into a virtual foreign currency account, for example Karbon Business lets clients pay via ACH, SEPA, Faster Payments, you avoid correspondent fees and bank lifting fees entirely.

Short credits, and what correspondent banks actually do

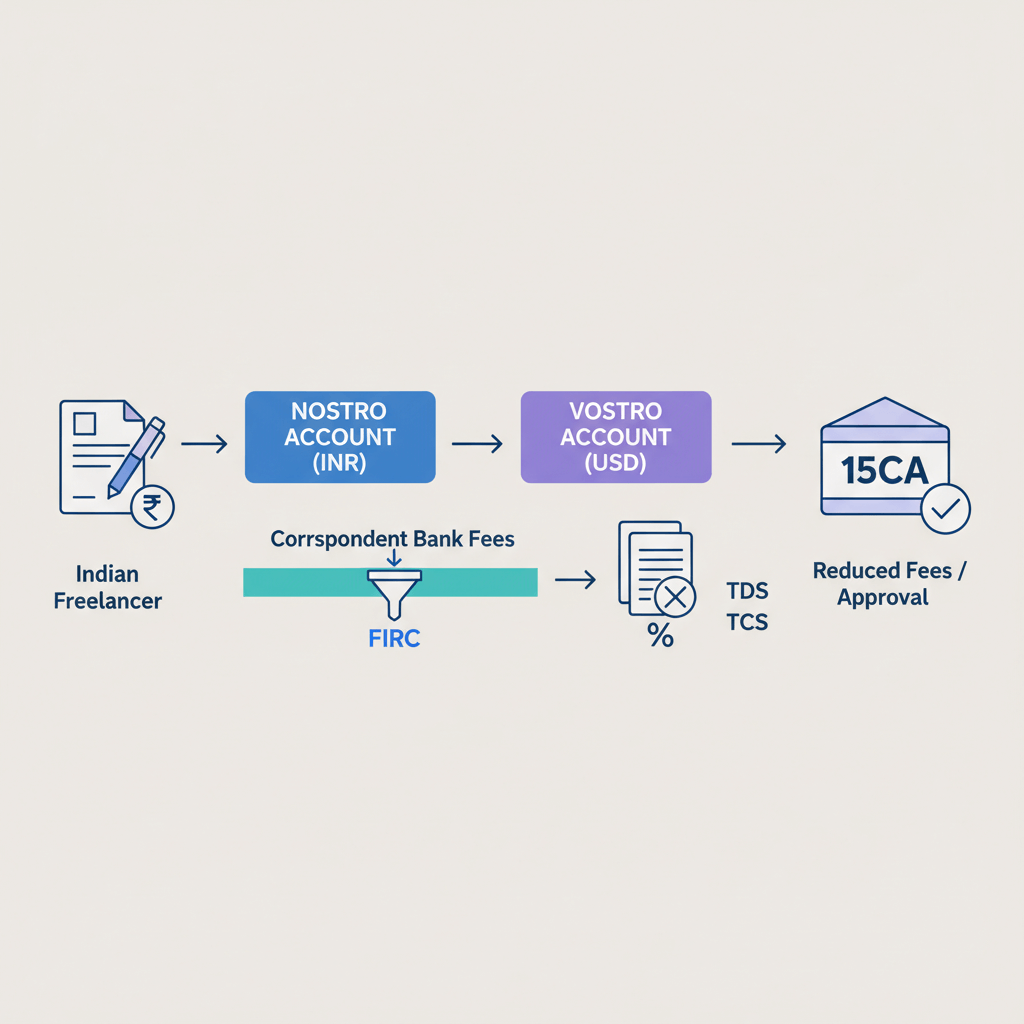

You invoice, your client pays, your statement still shows less, that shortfall is often correspondent bank charges. Banks do not connect to every other bank directly, so your payment moves through one or more intermediary banks on the SWIFT network, each may deduct a handling fee, then your Indian bank receives, converts, and credits the remainder.

India specific flow: Chase, or Barclays, or Deutsche Bank, sends your client’s payment, it may hop through a US correspondent, a global hub, an India facing correspondent, then land at SBI, HDFC, ICICI, or Axis. Every hop can shave off dollars before conversion.

You see a smaller INR credit, your client still sees “$1,000 sent,” the difference lives inside the SWIFT chain and your bank’s receiving and FX practices.

All the fees, correspondent bank charges explained

Intermediary fees

These are deductions by middle banks that route the wire, usually $10 to $30 per bank, unpredictable because you do not control the path, see the Razorpay inward remittance explainer for context.

Lifting fee

Your Indian bank’s receiving charge for processing the SWIFT, typically ₹200 to ₹1,000 plus GST, often labeled inward remittance, SWIFT receipt, or cable charges, outlined in the same Razorpay guide.

FX spread or markup

Not a line item, but a worse than mid market rate adds 1 percent to 3.5 percent cost, learn more in Winvesta’s FX markup explainer. A small looking rate difference compounds into thousands over a year.

Charge codes, OUR, SHA, and BEN

Field 71A in the SWIFT message sets who pays what, see charge code fundamentals.

- OUR, sender covers all fees, ideal for freelancers, verify it on the MT103.

- SHA, fees are shared, you bear intermediary, receiving, and lifting fees in India.

- BEN, beneficiary pays everything, avoid this, it results in maximum deductions.

Add them up and the total hit is often 3 percent to 5 percent of your payment, as noted in the Razorpay overview.

On ₹10 lakh received, that is ₹35,000 to ₹50,000 gone.

Deep dive, the lifting fee in India

The lifting fee is your bank’s charge to receive and process cross border wires, handle compliance, convert currency, credit your account, and generate e FIRC or e FIRA. Typical range, ₹200 to ₹750 plus GST, sometimes higher for large credits, details in the Razorpay inward remittance guide.

- Public sector banks, lower fee, slower credit.

- Private banks, faster credit, higher fee.

- Some banks charge additionally for physical FIRC copies, see Winvesta.

Can it be waived? Rarely, you may negotiate if your volume is high, otherwise plan for it.

Deep dive, intermediary fees

These charges are deducted upstream by correspondent banks before your money reaches India, $15 to $30 each depending on routing, as seen across cases in the Razorpay explainer and Winvesta’s write up.

Why it varies: different banks have different correspondent relationships, so the same payment corridor can take two hops today, three tomorrow.

Example, a €2,000 wire with SHA routes via Germany and New York, two intermediaries deduct fees, your Indian bank applies its lifting fee and FX markup, you end up several thousand rupees short, as stories like this surface in Archway’s freelancer payment costs post.

How to read the MT103, trace your money step by step

The MT103 is the payment instruction that lets you audit a transfer end to end, it shows who sent, which intermediaries touched the payment, who pays fees, and what was deducted, a process also referenced in the Razorpay guide.

- Field 20, transaction reference, use it for traces or escalations.

- Field 32A, value date, currency, amount sent, your baseline for reconciliation.

- Field 33B, original currency and amount if there was upstream conversion.

- Field 50 and 59, sender and beneficiary details, confirm accuracy.

- Field 52A, 53A, 54A, ordering and correspondent institutions.

- Field 56A, intermediary bank, count the hops here, and sometimes 57A shows account with institution.

- Field 71A, charge code, OUR, SHA, or BEN.

- Fields 71F and 71G, sender and bank charges, can explicitly show deducted amounts.

Mini snippet, purely illustrative:

:32A: USD 1000,00

:56A: CHASUS33XXX

:71A: SHA

:71G: USD 25,00

This means an intermediary likely deducted $25, and charges were shared, so you bear receiving side costs.

Got a short payment, do this

- Collect evidence, the MT103, your credit advice, and your statement.

- Reconcile, compare Field 32A with your INR credit, note Field 56A or 57A for intermediaries, check Field 71A, 71F, 71G for the fee split and amounts, a workflow described in the Razorpay inward remittance post.

- Escalate if needed, if your invoice specified OUR but you still got deductions, ask your client’s bank to run a SWIFT trace with your Field 20 reference, they can raise claims to correspondents, timelines can be 5 to 10 business days.

- Prevent repeats, explicitly state OUR on invoices and contracts, share the exact SWIFT BIC, ask the sender to minimize intermediaries, see additional pointers in Xflow’s bank charges overview.

Practical playbook, reduce or avoid correspondent bank charges

- Insist on OUR, standardize this in every invoice, and verify it on the MT103, a position explained in HiWiPay’s plain English guide.

- Minimize the correspondent chain, give the exact BIC, ask the sender’s bank for direct correspondents where possible, see notes in Xflow’s guide.

- Skip SWIFT when feasible, have clients pay locally into your virtual foreign currency account using ACH, SEPA, or Faster Payments, this removes intermediary fees and lifting fees.

Platforms to consider:

- Karbon Business, virtual USD, GBP, EUR, CAD accounts, client pays locally, flat 1 percent fee, mid market rates, INR settlement in 24 to 48 hours, auto e FIRA, and optional 60 day currency hold.

- Wise Business, low transparent fees and multi currency holding.

- Payoneer, multi currency receiving accounts, widely used by marketplace freelancers.

- RazorpayX International, India focused workflows.

- Revolut Business, multi currency accounts depending on availability.

Compare three scenarios on $1,000

SWIFT with SHA, roughly $20 in intermediaries, ₹500 lifting, 2.5 percent FX markup, net around ₹83,000.

SWIFT with OUR, sender bears routing fees, you still face FX markup and lifting, net around ₹83,500.

Local ACH to a virtual USD account, for example via Karbon Business, flat 1 percent, mid market FX, net around ₹83,160, meaning the largest savings against SWIFT.

Where Karbon Business fits

If unpredictable correspondent deductions frustrate you, a local rails approach helps. Karbon Business gives you client friendly local details, ACH in the US, SEPA in the EU, Faster Payments in the UK, EFT in Canada, then converts at mid market xe.com rates with no markup, settles INR fast, and auto generates your e FIRA. You remove intermediary fees, remove lifting fees, and remove FX markup, paying a simple flat platform fee instead. For freelancers billing several thousand dollars monthly, these changes can save lakhs annually.

India specific compliance, what to keep

- MT103 or equivalent receipt, retain for at least seven years, as also highlighted by the Razorpay inward remittance guide.

- Invoice or contract, export of services evidence for RBI or tax scrutiny.

- e FIRA or e FIRC, needed for tax filings and refunds, see reminders in Xflow’s notes.

- Tax reporting, track foreign income, INR equivalent, fees, net credit, and e FIRA references.

- Bank and corridor differences, timelines and fees vary by bank and route, confirm with your RM and your CA.

Quick checklist for every payment

Before invoicing

- State “All bank charges OUR.”

- Share your exact SWIFT BIC or virtual account details.

- Ask the client to minimize correspondent hops, or pay via local rails.

After payment

- Request the MT103.

- Check Field 32A, 56A or 57A, 71A, 71F and 71G.

- Reconcile sent versus credited, note every deduction.

If short paid

- Collect MT103, credit advice, statement.

- Compute intermediary, lifting, and FX costs.

- Ask for a SWIFT trace if OUR was agreed.

- Fix your templates and terms to prevent repeats.

FAQ

What exactly are correspondent bank charges in international payments to India?

They are fees taken by intermediary banks that route your client’s wire through the SWIFT network, plus your Indian bank’s lifting fee, and the FX spread, the Razorpay inward remittance guide breaks these down in plain English.

Why did my client send $1,000 but I got less INR credited in my Indian bank?

Because intermediaries likely deducted $10 to $30 each, your bank applied a lifting fee, and the conversion used a marked up rate, request the MT103 to see exactly where the money went.

How do I make sure I receive the full invoice amount from overseas clients?

Put “OUR” in your invoice terms, confirm Field 71A shows OUR on the MT103, and ask your client’s bank to minimize correspondent hops, or have clients pay locally into a virtual foreign currency account via Karbon Business so you skip SWIFT altogether.

What is the lifting fee and can I avoid it completely?

It is your Indian bank’s incoming wire processing charge, typically ₹200 to ₹1,000 plus GST, you can reduce its impact by avoiding SWIFT and receiving via local rails with platforms like Karbon Business, which eliminate bank lifting fees.

What are OUR, SHA, and BEN in SWIFT, and which one should I choose?

They are fee split codes in Field 71A, OUR means sender pays all routing fees, SHA shares fees, BEN makes you pay all, choose OUR for full protection, see this Field 71A overview for details.

How do I check which intermediary banks deducted fees on my payment?

Look at Field 56A and sometimes 57A on the MT103 guide, then compare Field 32A to your credit, and inspect Fields 71F and 71G for explicit charges.

Is the FX markup really that costly on freelancer receipts?

Yes, a 1 percent to 3.5 percent spread versus mid market adds up over time, on $10,000 a year that can mean ₹84,000 to ₹2,94,000 lost, see Winvesta’s FX markup explainer for examples.

How can I avoid correspondent charges if my client refuses OUR charges?

Offer a non SWIFT option, ask them to pay locally via ACH, SEPA, or Faster Payments into your virtual account on Karbon Business, they pay domestic fees, you avoid intermediaries and lifting fees, and both sides see transparent pricing.

What documents should I keep for RBI and tax compliance when I get paid from abroad?

Keep the MT103 or equivalent receipt, your invoice or contract, and the e FIRA or e FIRC for each payment, as emphasized in the Razorpay guide to inward remittances.

My payment is short, how do I recover fees after the credit has arrived?

Reconcile using the MT103, if your invoice specified OUR but the payment came with SHA or BEN, ask your client’s bank to run a SWIFT trace referencing Field 20, they may claw back certain charges, though it can take several business days.

Which is cheaper for a $1,000 invoice, SWIFT wire or local ACH to a virtual USD account?

In most cases, local ACH to a virtual USD account wins, SWIFT with SHA might cost you $35 to $60 in total, while a platform like Karbon Business charges a flat 1 percent with mid market FX, and no lifting or intermediary fees.

What should I write in my invoice to stop short credits from happening again?

Add “All bank charges borne by sender, OUR charges mandatory” and include your exact SWIFT BIC, also offer a non SWIFT option like Karbon Business with ACH or SEPA details, so your client chooses the path with fewer deductions.