Key takeaways

- BEN means you pay all bank fees, SHA splits fees, OUR makes the sender pay all fees, so your receipts depend directly on the charge code selected.

- On a $2,000 invoice, BEN can shave $35 to $70 before conversion, which is why ₹1,61,435 might hit instead of ₹1,66,000 at ₹83 per dollar.

- Specify OUR in contracts and invoices, confirm it before payment, and verify it after payment using the SWIFT MT103.

- Use local rails like ACH transfers, SEPA, and FPS via virtual accounts to bypass correspondent fees entirely.

- Even with OUR, expect FX markups unless you negotiate mid market conversion or use platforms that offer zero markup.

- For a plain English primer, see OUR, BEN, SHA charges and this concise Currencies Direct explainer.

- If a payment lands short, request the MT103, check Field 71A for BEN, SHA, or OUR, then reconcile and request reimbursement if needed.

- Indian freelancers can simplify compliance, lower costs, and get predictable receipts with platforms like Karbon Business.

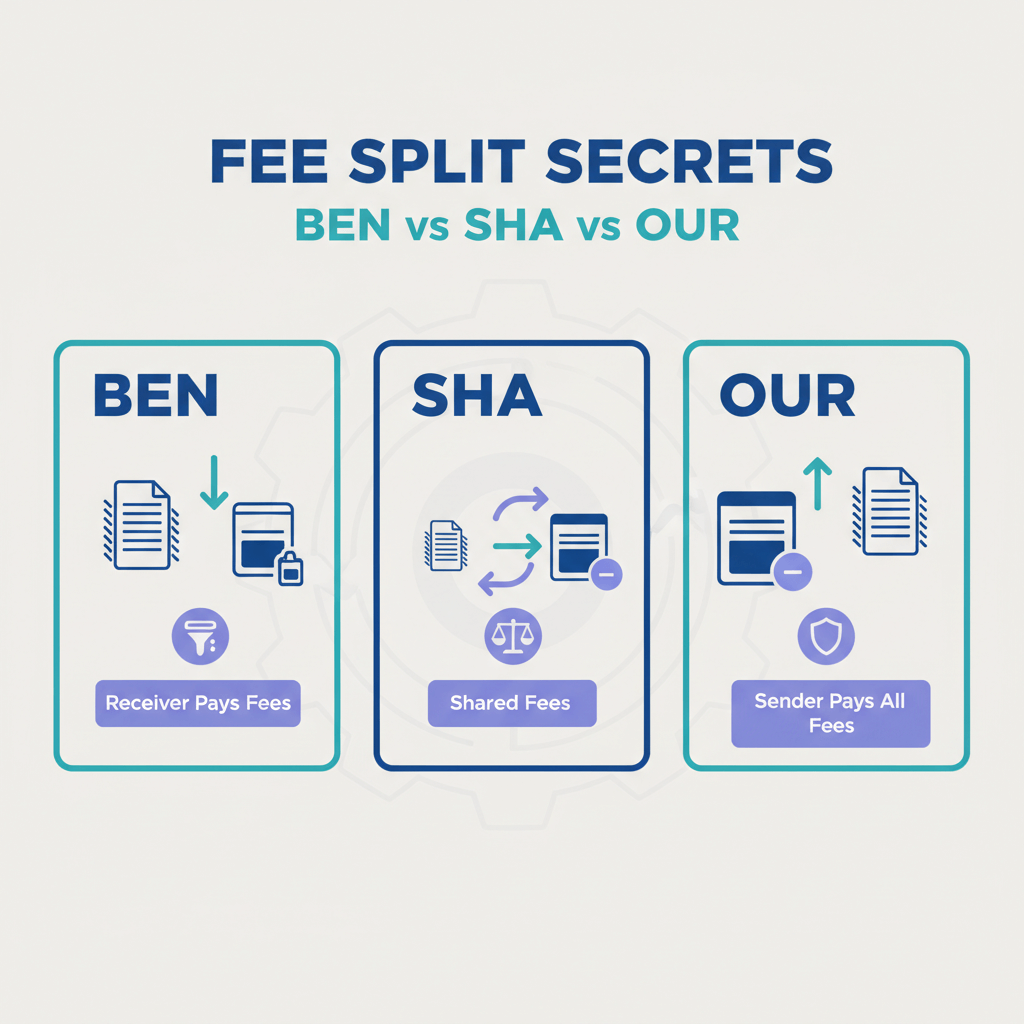

What are BEN, SHA, and OUR charges?

When a client sends money via SWIFT, a small field called 71A decides who pays fees across the chain, the sender bank, intermediary banks, and your receiving bank. That field can be BEN, SHA, or OUR, and the choice determines whether you receive your full invoice or a short credit.

BEN, beneficiary pays all charges: Every fee is deducted from the incoming amount, you receive less without warning.

SHA, shared charges: The sender pays their outgoing bank fee, you pay intermediary and beneficiary bank fees, deducted from the principal on the way in.

OUR, sender pays all charges: The sender covers every fee in the chain, you should receive the full principal amount, barring rare anomalies.

For more context and examples, review OUR, BEN, SHA charges.

Think of it this way, BEN burdens you, SHA splits the pain, OUR protects your invoice amount.

BEN vs SHA vs OUR, side by side

| Charge type | Fees you pay | Net receipt | Pros for freelancers | Cons for freelancers |

|---|---|---|---|---|

| BEN | All fees, sender, intermediary, beneficiary | Principal minus all fees | None for you | Unpredictable short payments |

| SHA | Intermediary and beneficiary fees | Principal minus those fees | Sender shares cost | Still short, hard to predict |

| OUR | Ideally none | Full principal amount | Predictable, clean reconciliation | Some clients resist higher upfront costs |

Another quick explainer worth saving, the Currencies Direct explainer.

How BEN, SHA, and OUR impact amount received, real examples

Example 1, US client sends $2,000

BEN: Intermediary and receiving banks take about $55 combined, you receive $1,945, that is roughly ₹1,61,435 at ₹83, a ₹4,565 shortfall.

SHA: Sender covers their own bank, you still lose about $25, you receive ~$1,975, or ₹1,63,925.

OUR: Full $2,000 should land, ₹1,66,000 at ₹83. If your bank applies a 1.2 percent FX markup, the final INR could be ~₹1,64,000, the loss is conversion, not fees.

For clarity on the charge field, see the LetsDeel guide.

Example 2, EU client sends €1,800

SWIFT with SHA: Intermediaries may deduct €40 to €60, you might receive about €1,750.

SWIFT with OUR: Full €1,800 should arrive, conversion markup still applies if your bank adds a spread.

SEPA to a EUR virtual account: Usually €0 to €5 all in, near full net receipt, no SWIFT intermediaries.

For a plain language refresher, check the ExTravelMoney overview.

Small deductions compound fast, repeated BEN payments can quietly erase lakhs over a year.

How to choose the right charge option, step by step

Step 1, specify OUR everywhere. Add this to your invoices and contracts, Please initiate payment with charge code OUR, Field 71A, beneficiary must receive full invoice amount without deductions.

Step 2, if the client insists on BEN or SHA, price for it. Add a 2 to 3 percent buffer, or a separate line item, SWIFT fee surcharge, $50, refunded if payment sent via OUR.

Step 3, prioritize local payment rails. Ask for ACH transfers for US clients, SEPA for EU, FPS for UK, EFT or Interac for Canada. Virtual local accounts make this effortless, and they bypass SWIFT fees.

Step 4, verify details upfront. Confirm exact beneficiary name, account number, IFSC or IBAN, bank name and address, then confirm the charge type before they press send.

Step 5, match the account name exactly. Even minor mismatches can trigger holds or reroutes, which create extra costs and delays.

For quick backup reading, keep a tab on the global overview of BEN, SHA, OUR.

How to check what charge type was used, verification

Ask for the SWIFT MT103. The MT103 is the official wire confirmation, Field 71A shows BEN, SHA, or OUR, remittance lines display deductions.

Cross check the credit. If no MT103 is available, compare the credited INR against your invoice using the bank’s exchange rate, a shortfall usually means BEN or SHA.

Reconcile methodically. Net foreign currency received times the bank rate should equal your INR credit. If the foreign currency amount is short, fees were deducted upstream.

Another quick reference is the LetsDeel guide.

Avoiding surprises and lowering costs, practical tips

Use platforms with local virtual accounts. Clients pay domestically, you skip correspondent banks entirely. Explore Karbon Business, Wise Business, Payoneer, PayPal, and RazorpayX International. For background on bank fees in transfers, see Payoneer’s SWIFT money transfer and fees guide.

Confirm FX rates in advance. Ask for proof of the mid market rate, compare with Xe or Google, and avoid silent markups when possible.

Skip cards for large invoices. Card fees are usually higher, and chargebacks add risk, bank transfers with OUR are cleaner.

Hold foreign currency tactically. Where permitted, consider holding up to 60 days to convert when the rate improves.

Even with OUR, glitches happen. If a fee is deducted despite OUR, share the MT103 with your client and request reimbursement.

Karbon Business, built for Indian freelancers

Karbon Business gives you virtual USD, GBP, EUR, and CAD accounts, so clients pay via local ACH, SEPA, or FPS, you avoid SWIFT intermediary fees entirely. You pay a flat 1 percent platform fee, with zero FX markup at live mid market Xe rates, INR arrives in 24 to 48 hours. e FIRA is auto generated within 24 hours, and support on WhatsApp or email responds quickly.

The result is simple, predictable receipts, faster settlement, and clean compliance that lets you focus on your craft instead of chasing missing dollars.

Edge cases and important caveats

OUR is not a magic wand. Rare network errors can still cause small deductions, the MT103 will reveal them.

SHA varies by bank. IntermediARY cuts are not standardized, which makes SHA hard to predict across corridors.

Typos are expensive. Wrong SWIFT, IBAN, or name mismatches can trigger reroutes or returns, often adding $20 to $50 in fees.

FX markups are separate from fees. OUR covers fees, not conversion margins, negotiate clearly for mid market conversion where possible.

Compliance for Indian freelancers, e FIRA and documentation

RBI and FEMA expect proper documentation for inward remittances. Your bank issues e FIRA as proof of receipt and conversion, and you may need Form 15CA and 15CB, plus invoice, agreement or scope, payment proof, and the MT103. If you are under GST for export of services, retain proof of foreign remittance for zero rated invoices and reconciliation. A helpful recap is this ExTravelMoney overview, and platforms like Karbon Business auto generate e FIRA to simplify the process.

Quick checklist, before, during, and after each payment

Before invoicing:

- Specify OUR, Field 71A, in your contract and invoice terms

- Confirm the client’s bank supports OUR

- Share exact beneficiary details, name, account, IFSC or IBAN, bank name and address

- Prefer local rails, ACH, SEPA, FPS, or EFT via virtual accounts

Before payment initiation:

- Get written confirmation that the client will select OUR

- Double check every character of your bank details

- Clarify expected exchange rate or confirm zero FX markup

After payment received:

- Request and review the MT103

- Reconcile net foreign currency times bank rate to INR credited

- Verify deductions match the expected charge type

- File e FIRA, 15CA or 15CB if applicable, and GST records

- If short beyond expectation, contact the client with MT103 proof

FAQ

BEN charges meaning kya hota hai for Indian freelancers?

BEN ka matlab hota hai ki saare bank charges aap par lagenge, sender bank, intermediary banks, aur aapka receiving bank, ye sab fees incoming amount se kat li jaati hain, isliye aapko invoice se kam credit milta hai.

OUR charges select karne se full amount milega ya bank phir bhi kuch kaatega?

OUR select hone par sender sab fees pay karta hai, isliye principal amount poora aana chahiye, fir bhi FX markup alag hota hai, bank 1 se 3 percent tak conversion margin laga sakta hai, platforms like Karbon Business zero markup par settle karne mein madad karte hain.

SHA charges ka practical impact kya hota hai mere INR credit par?

SHA mein sender apna outgoing bank fee deta hai, baaki intermediary aur receiving bank fees aapke amount se cut hoti hain, typical $20 se $50, isliye INR credit invoice se kam hota hai, reconciliation thoda messy ho sakta hai.

US client ko OUR choose karne ke liye polite kaise bolun?

Invoice terms mein likhiye, Please select charge code OUR, Field 71A, beneficiary must receive full invoice amount without deductions, email pe send karte hue ek line add karein, Just confirming you will select OUR for full payment, correct, clear instruction se confusion khatam hota hai.

Client ne SHA me bheja aur amount short aaya, ab kya recovery possible hai?

First MT103 mangaaiye aur Field 71A check keejiye, agar SHA ya BEN dikhe to shortfall calculate karke client se reimbursement politely maangiye, future invoices me 2 se 3 percent buffer add karke protect kariye, ya surcharge line item likhiye, Karbon Business jaisa platform use karenge to yeh problem mostly avoid ho jaati hai.

MT103 me charges kaise identify karun, exactly kya dekhna hota hai?

MT103 me Field 71A me BEN, SHA, ya OUR likha hota hai, remittance details me intermediary deductions line by line aate hain, USD ya EUR me net amount compare karke aap FX rate se multiply karke INR credit verify kar sakte hain.

SEPA directly Indian account me aata hai kya, ya mujhe EUR virtual account chahiye?

SEPA India me direct nahi aata, better hai ki aap EUR virtual account use karein, client EU me domestic transfer karta hai, aapko near full amount milta hai, phir INR settlement hoti hai, platforms like Karbon Business aise local accounts provide karte hain.

Karbon Business, Wise, Payoneer me se USD receive karne ke liye best option kaunsa hai?

Agar aapko predictable INR settlement, zero FX markup, aur e FIRA automation chahiye to Karbon Business strong option hai, Wise aur Payoneer bhi workable hain with transparent pricing, lekin fees plus FX structure compare karke hi decide kariye, high value invoices ke liye local rails aur mid market rate sabse bada saving dete hain.

RBI, FEMA, aur GST compliance ke liye kya documents rakhu jab client international payment bhejta hai?

Invoice, scope of work ya agreement, SWIFT MT103, bank statement credit, e FIRA, aur jab zarurat ho to Form 15CA aur 15CB, zero rated GST invoices ke liye foreign remittance proof attach rakhiye, Karbon Business jaise platforms e FIRA auto generate karke workload kam kar dete hain.

OUR select hua tha phir bhi thoda short credit kyun aaya, kya karun?

Ye usually FX markup ya rare network anomaly hota hai, MT103 me OUR confirm karke client ko share kariye, agar intermediary deduction visible hai to politely reimbursement request bhejiye, future me rate and fee confirmation email pe upfront le lijiye.

Invoice pricing me SWIFT fees ka buffer kaise add karun taki mera net amount protected rahe?

Aap 2 se 3 percent top up kar sakte hain, ya separate line item, SWIFT fee surcharge, $50, add karke likh sakte hain, Refunded if payment sent via OUR, isse client OUR choose karne ke liye incentivized hota hai, warna aapka net protect ho jata hai.

US client ke liye ACH better hai ya SWIFT, aur kaise start karun quickly?

High value invoices par ACH almost always cheaper aur predictable hota hai, local rails use karne ke liye aapko US bank details chahiye, jo virtual account se mil jaati hain, Karbon Business mein USD virtual details milti hain, client domestic ACH bhejta hai, aapko full value ke near credit milta hai.

Take control of your international payments

Every rupee you earn should reach you in full. Learn BEN versus SHA versus OUR, set OUR in your terms, move clients to local rails where possible, verify with MT103, and consider purpose built solutions like Karbon Business for predictable receipts and faster compliance. Review your last three payments today, identify any BEN or SHA deductions, and update your templates so your next invoice lands in full.