Key takeaways

- For small and medium invoices, ACH to a virtual USD account is usually the cheapest, predictable route, with flat fees around 1%, mid-market USD to INR, and automatic e-FIRA.

- SWIFT bank wires suit very large, enterprise invoices, but invisible intermediary deductions and FX markups can bite, request OUR instructions so the sender covers all fees.

- Global wallets and card links are convenient, yet total costs often reach 3 to 6% or more, plus potential chargebacks and withdrawal delays.

- To reduce costs, consolidate invoices, prefer ACH, compare mid-market FX versus carded bank rates, and store every e-FIRA for your CA.

- India-focused fintechs like Karbon Business provide local US bank details in your name, INR settlement in 24 to 48 hours, the option to hold USD up to 60 days, and automatic compliance documentation.

Why Indian freelancers need a smarter way to receive USD from the USA

If you are a freelancer or solo consultant in India, figuring out the best ways to receive USD payments from USA to India can be confusing and expensive. You face high fees, unpredictable timelines, and FX markups hidden inside carded bank rates. Clients prefer ACH, PayPal, or cards, and you need a method that keeps costs low, compliance clean, and cash flow reliable.

This guide shows you, step by step, when to pick SWIFT bank wire versus alternatives, how funds actually move, and how to cut fees while staying fully RBI and FEMA compliant.

How funds travel from a US client to your Indian account

- SWIFT bank wire: A US bank sends money via intermediary banks over the SWIFT network to your Indian bank.

- Global wallets like PayPal or Payoneer: Client pays a wallet, the wallet converts and sends INR to your bank.

- Card payments or payment links: Client pays via a card gateway, conversion and settlement are handled by the processor.

- ACH to virtual USD account: Client pays a local US account via ACH, the fintech converts USD to INR, then credits your Indian bank.

- Other online remittance services: Client pays through an app, funds land in your account or UPI in INR.

Where fees and delays creep in

Across these routes, costs and time are driven by multiple factors:

- Sender bank fees for SWIFT wires, paid by your US client.

- Intermediary bank deductions inside SWIFT, you rarely see them upfront.

- Recipient bank fees on inward remittance and lifting charges, applied by your Indian bank.

- Platform or gateway fees from PayPal, Payoneer, card processors, and marketplaces.

- FX markup on USD to INR, the biggest hidden cost when the rate is worse than mid-market.

- Compliance checks on name matching, purpose codes, and AML reviews that can delay settlement.

Keep this flow in mind, it explains why bank wire can look cheap yet still pay out less than ACH to a virtual USD account.

Bank wire versus alternatives, what should Indian freelancers use?

1. Bank wire, SWIFT

How it works

Your client instructs their bank to send an international wire over the SWIFT network to your Indian bank account.

Pros

- Global standard, accepted by banks worldwide.

- Handles high limits well, suits large B2B invoices.

- Clear audit trail that enterprises appreciate.

Cons

- Sender fee often USD 20 to USD 50.

- Intermediary deductions mid-route, USD 10 to USD 40 or more.

- Speed can be 2 to 5 business days, longer around holidays.

- Opaque tracking with multiple intermediaries.

- Banks add FX markup over mid-market USD to INR.

- Possible compliance queries for purpose codes and invoices.

Best for

- Large B2B invoices around USD 15,000 to USD 20,000 and above.

- Enterprises with strict AP policies that only allow wires.

- Contracts that explicitly mandate SWIFT payment.

2. ACH to virtual USD account, fintech route

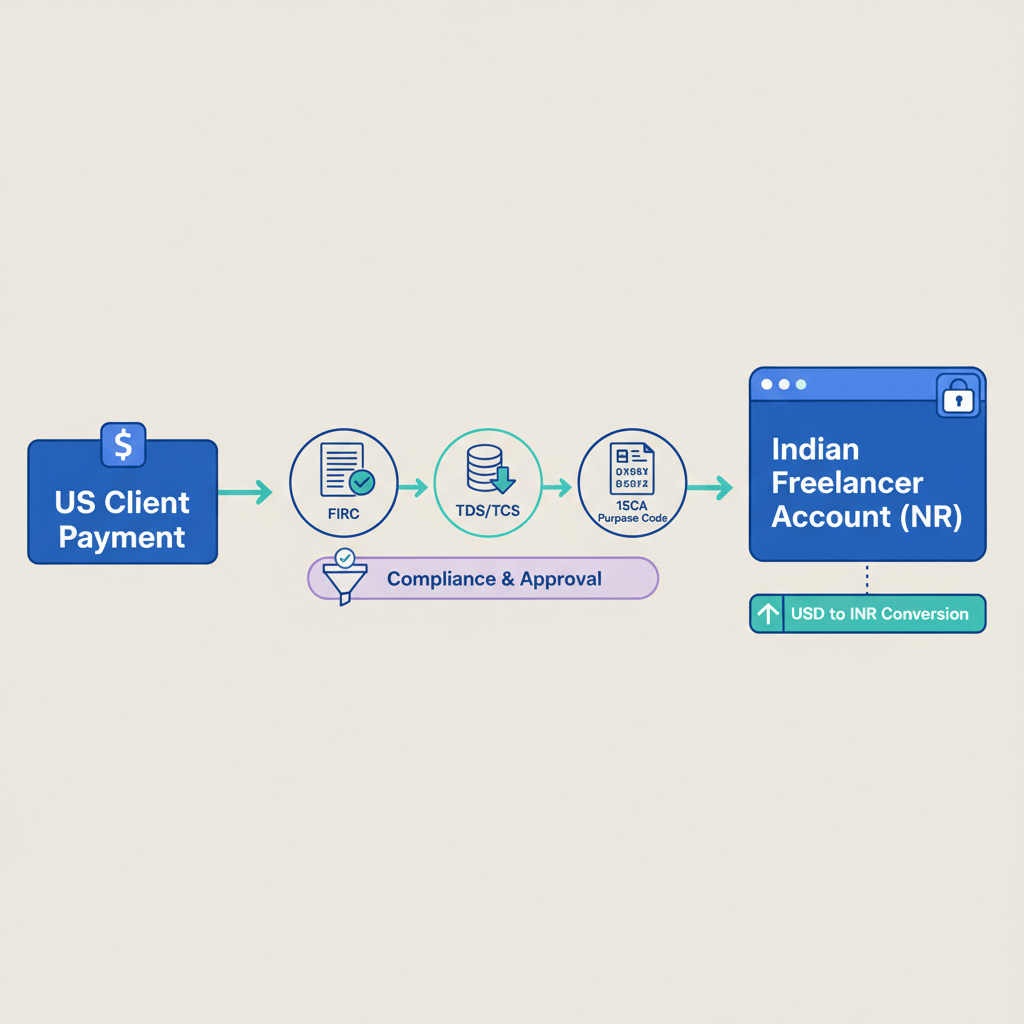

You use a virtual USD account in your own name, with real US routing and account numbers. Your client pays via ACH like a local vendor, the fintech converts USD to INR, then settles in your Indian bank.

Pros

- ACH is low or zero fee for US clients, familiar and easy.

- Predictable timing of 24 to 72 hours into your USD account.

- Transparent fees, often flat 1 to 2%, near zero FX markup at mid-market.

- Clear ledgering, easier reconciliation against invoices.

- Automatic e-FIRA and correct purpose codes with India-focused providers.

- Option to hold USD for a period, such as up to 60 days.

Cons

- Onboarding and KYC needed, PAN, Aadhaar, bank statements, proof of work.

- Per-transaction or annual limits may apply.

- Must choose an RBI and FEMA compliant provider.

Best for

- Recurring retainers and monthly invoices.

- US SMEs and startups that prefer ACH over wires or cards.

- Freelancers, SaaS, and service exporters seeking low fees and automated compliance.

3. Global wallets, PayPal, Payoneer

Pros

- High client familiarity, quick to initiate.

- Useful when marketplace payouts connect to wallets, see this freelancer payment method guide.

Cons

- Total platform and FX fees often 3 to 6%.

- Extra withdrawal fees and FX margins when moving funds to your bank, explained in freelance payment methods in India.

- Chargeback exposure if a client disputes.

- Withdrawal delays and rolling reserves can hold money for weeks.

Best for

- Small ticket, one-off buyers who insist on familiar wallet payments.

- Cases where marketplace payouts require a connected wallet.

4. Card payment links, Stripe, Razorpay, and others

Pros

- Instant client payments by card, simple hosted checkouts.

- Helpful for deposits or urgent, last-minute cash needs.

Cons

- Processing fees often start near 2.9%, plus FX and cross-border charges.

- Chargebacks and disputes are a risk.

- High-value international charges can be capped or scrutinized.

Best for

- Deposits on new projects, small urgent work when speed matters.

- Emergency payments when ACH or wire is not possible.

5. Fintech alternatives designed for India

Some platforms are built specifically for Indian exporters and freelancers:

- Karbon Business: Virtual USD, GBP, EUR, CAD accounts, local transfer capability, real US bank details in your name, ACH or domestic wire collection, flat 1% platform fee, zero FX markup with mid-market rates, INR settlement in 24 to 48 hours, hold USD up to 60 days, automatic e-FIRA.

- Wise Business: Multi-currency accounts with transparent fees and mid-market rates.

- Payoneer: Virtual receiving accounts across currencies, widely used by global freelancers.

- RazorpayX International: Local account details to collect foreign payments.

- WorldFirst: International business payments and currency services for exporters.

Pros of India-focused fintechs

- Local USD accounts in your name, clients pay via ACH or domestic wire like a US vendor.

- Flat, transparent pricing around 1%, predictable costs.

- Zero FX markup, conversion at mid-market USD to INR.

- INR settlement typically in 24 to 48 hours after conversion.

- Hold USD up to 60 days to time your conversion.

- Automatic e-FIRA for every inward remittance.

Cons

- Requires onboarding and KYC.

- Check client fit, are they able to pay via ACH or domestic wire.

Best for

- Small and medium invoices where every percentage matters.

- Recurring retainers with multiple monthly payments.

- Freelancers standardizing a low-fee, transparent, compliant process across US clients.

Quick comparison, choosing the right rail per situation

- SWIFT bank wire: Total costs often USD 30 to 90+ including sender, intermediary, and FX, speed 2 to 5 business days, low chargeback risk, strong audit trail, best for large enterprise invoices.

- ACH to virtual USD account: Around 1 to 2% all-in with minimal FX markup, USD lands in 24 to 72 hours then INR in 24 to 48 hours, low dispute risk, automatic e-FIRA, ideal for retainers and recurring SME clients.

- Wallets: 3 to 6%+ including platform and FX, hours to wallet then 1 to 2 days to bank, higher chargeback risk, weaker documentation, good for one-off or marketplace payouts.

- Card links: Often 3 to 4%+ plus FX and cross-border fees, minutes to charge then days to payout, highest chargeback risk, suitable for urgent small payments or deposits.

- India-focused fintechs: Around 1% flat, conversion at mid-market, INR within 24 to 48 hours, automatic e-FIRA, the default choice for most freelance exports from the US.

Fees decoded, what you really pay

Visible versus hidden fees

- Sender fee: Your client’s bank or platform charge to initiate the payment.

- Intermediary bank fees: Deductions inside SWIFT that you do not see until money arrives short.

- Recipient bank fees: Inward remittance and lifting charges at your Indian bank.

- Platform fees: PayPal, Payoneer, card gateways, or remittance services.

- FX markup: Spread between mid-market USD to INR and your actual rate, often the biggest hidden cost.

- Conversion charges: Explicit currency conversion fees.

- GST on fees: 18% on Indian-side fees and platform charges.

Example cost scenarios

Assumptions, wire costs USD 30 sender plus USD 20 intermediary, plus 2% FX markup, wallet costs 4% total, ACH to virtual USD account costs 1% flat with zero FX markup at mid-market.

A. Small payment USD 500

- SWIFT wire: USD 50 fixed, effective cost roughly 10% before FX.

- Wallet: 4% equals USD 20.

- ACH to fintech: 1% equals USD 5.

B. Medium payment USD 3,000

- SWIFT wire: USD 50 fixed plus USD 60 FX markup, total about USD 110.

- Wallet: 4% equals USD 120.

- ACH to fintech: 1% equals USD 30.

C. Large payment USD 15,000

- SWIFT wire: USD 50 fixed plus USD 300 FX markup, total roughly USD 350.

- Wallet: 4% equals USD 600.

- ACH to fintech: 1% equals USD 150.

When a cheap sender fee still costs more

On USD 5,000, a 2.5% FX markup equals USD 125, a 1% all-in fintech fee equals USD 50, the “cheaper bank” option can still cost USD 75 more due to FX spread alone.

Tips to reduce fees

- Consolidate invoices, fewer, larger payments reduce fixed fees.

- Prefer ACH to virtual USD accounts, eliminates intermediary deductions.

- Minimize intermediaries, ask for direct correspondents on SWIFT if wires are required.

- Negotiate the method upfront, show clients how their wire creates short credits on your side.

- Standardize one low-fee process, document it in proposals and contracts.

USD to INR essentials, understanding the FX impact

Mid-market versus bank carded rates

The mid-market rate is the neutral real rate you see on Google, banks often use carded rates that are worse, embedding a margin. India-focused fintechs offer conversion at or near mid-market, charging a transparent fee instead.

How FX markup compounds on large payments

On USD 10,000, at USD 1 equals ₹83 you expect ₹8,30,000, at USD 1 equals ₹81.5 you get ₹8,15,000, a small 1.8% difference costs ₹15,000, before visible fees.

Holding USD to hedge rate risk

Some providers let you hold USD up to 60 days, if you expect USD to INR to move in your favor, timing conversion can add value. Example, USD 5,000 at ₹82 equals ₹4,10,000, at ₹84 equals ₹4,20,000, a ₹10,000 gain before considering risk.

Communicating rates to clients

Quote in USD yet track INR internally against a mid-market reference, include a currency clause such as, “USD to INR assumed at ₹83, if it moves by more than 3%, future project rates may be revised.”

How to receive payment USA to India, step-by-step

- Agree the payment method: Decide between SWIFT wire, ACH to virtual USD account, wallet, or card, based on amount, urgency, and client preference.

- Share accurate beneficiary or virtual USD details: For SWIFT, share SWIFT code, account number, full bank address, and exact beneficiary name, for ACH, share US routing and account numbers issued to you.

- Issue a proper invoice: Legal name matching KYC, unique invoice number and date, payment method instructions, due date and late fee terms.

- Track incoming funds and timing: Ask for invoice reference in memo fields, note US and Indian holidays, monitor status in your bank or fintech dashboard.

- Convert USD to INR, or hold: Check live USD to INR, decide to convert now or hold if allowed.

- Collect compliance documents: Ensure e-FIRA is generated for each remittance, store invoices, contracts, and purpose codes for CA and tax filings.

- Reconcile and account for GST on fees: Match payments to invoices, record fees and GST as expenses, keep statements organized for assessments.

Real-world scenarios for Indian freelancers

Scenario 1, USD 800 design retainer, client prefers ACH

You are a UI or UX designer in Bangalore working with an agency in Austin, you set up a virtual USD account via Karbon Business. The client pays USD 800 via ACH to your US account details, the platform charges 1% equals USD 8, converts at mid-market, INR settles in 24 to 48 hours, e-FIRA is generated automatically. At ₹83, you net about ₹65,736, versus roughly ₹63,744 via a 4% wallet fee, you save about ₹2,000 monthly, ₹24,000 yearly.

Scenario 2, USD 6,000 development milestone, SWIFT versus ACH

Option A, SWIFT bank wire: Sender fee USD 25, intermediary deductions USD 45, FX markup 2% equals USD 120, total roughly USD 190, 2 to 5 business days, amount arrives short and at a worse rate.

Option B, ACH to virtual USD account: Client sends USD 6,000 via ACH, flat 1% equals USD 60, mid-market conversion, INR in 24 to 48 hours, predictable payout and automated e-FIRA, net at ₹83 is about ₹4,93,020, a gain near ₹19,020 versus wire.

Scenario 3, USD 20,000 consulting project, when SWIFT makes sense

Large enterprise in New York allows only SWIFT, include a contract clause, “Client will bear all sender and intermediary charges, beneficiary must receive USD 20,000 in full.” Ask for OUR instructions or clarify BEN versus SHA, confirm the first payment and adjust if short. On very large single payments, SWIFT can be acceptable when fees and FX are negotiated and absorbed by the client.

Compliance, documentation, and safety

FEMA and RBI in brief

Export of services is regulated under FEMA, supervised by RBI, banks and compliant fintechs capture purpose codes, remitter and beneficiary details, amounts, dates, and currencies for every inward remittance.

Why e-FIRA matters

e-FIRA is official proof of foreign income for exports, essential for income tax and GST audits, benefits, and clean CA records, keep an e-FIRA per payment.

Name matching and documentation

Ensure your legal name is consistent across PAN, Aadhaar, Indian bank account, fintech KYC, and invoices, even small mismatches can cause holds, store contracts, invoices, and payment proofs by client and year.

Chargebacks and disputes

Cards and wallets allow reversals, bank wires and ACH to virtual USD accounts are much harder to reverse, safer for B2B amounts and new clients.

Data security and fraud monitoring

Use RBI-regulated or FEMA-compliant providers, enable two-factor authentication, verify any change to payment details via a known phone number, fraudsters often send fake wire instructions.

Choosing the best method, a quick decision guide

- Small to medium, recurring payments: Prefer ACH, see get paid from USA, flat fees, mid-market USD to INR, automatic e-FIRA.

- Large enterprise clients: Use SWIFT, clarify who pays intermediary fees, request correspondent banks that minimize deductions, and ask for OUR instructions.

- Urgent, small payments, client prefers cards: Use payment links, price 3 to 4% gateway costs into your quote or list a processing surcharge.

- Always evaluate: Total fees, FX rates versus mid-market, speed to INR, e-FIRA quality, and client convenience.

Light product walkthrough, ACH and fintech route

- Generate invoice with US bank details: Platform issues routing and account numbers in your name, add them to your invoice.

- Client pays via ACH: For them it is just like paying a domestic contractor, often no ACH fee.

- Claim payment and settle: Funds reach your USD account in 1 to 3 business days, you see mid-market USD to INR, the exact INR you will receive, and a flat fee.

- INR settlement in 24 to 48 hours: After conversion, INR arrives via NEFT or RTGS.

- Automatic e-FIRA: Generated within about 24 hours with all regulatory fields.

- Optional, hold USD up to 60 days: Convert when you are comfortable with the rate, batch multiple invoices.

Common mistakes to avoid

- Focusing only on sender fee and ignoring FX spread and hidden charges.

- Underestimating intermediary deductions in SWIFT, leading to short credits.

- Missing invoice references in payment memos, causing reconciliation delays.

- Skipping e-FIRA, creating tax and compliance pain later.

- Using personal accounts or mismatched names, triggering compliance holds.

Conclusion

Choosing how to receive USD payments from USA to India can materially change your earnings. Base your decision on total cost including hidden FX markups, settlement speed, documentation quality with e-FIRA, and client convenience. Standardize a low-fee ACH or fintech flow for most US clients, keep SWIFT for large enterprise mandates, and document every inward remittance carefully. This way you keep more of what you earn, stay compliant, and free up time to deliver great work.

FAQ

What is the cheapest way to receive USD payments from the USA to India for freelancers?

In most cases, an ACH payment to a virtual USD account with a flat 1 to 2% fee and zero FX markup at mid-market beats SWIFT and wallets for small and medium invoices. Platforms like Karbon Business are optimized for this flow.

SWIFT bank wire or ACH to virtual USD account, which one is faster for Indian freelancers?

ACH to a virtual USD account often reaches your USD balance in 24 to 72 hours, then INR in 24 to 48 hours, while SWIFT wires typically take 2 to 5 business days and can be delayed by intermediaries and compliance checks.

How do USD to INR rates impact the money I finally receive in my Indian bank?

Even a 2% difference from mid-market can reduce your INR payout substantially on larger invoices. Compare the rate your provider shows against mid-market to understand hidden FX loss before you convert.

My US client only pays via ACH, how can I receive funds in India without PayPal?

Open a virtual USD account with an India-focused provider. You will receive real US routing and account numbers in your name. The client pays via ACH, you convert at mid-market, INR arrives in your Indian bank with automatic e-FIRA. Karbon Business is a practical example.

Is PayPal cheaper than ACH for international freelance payments to India?

Usually no, wallets often cost 3 to 6% of the payment after platform and FX fees. ACH to a virtual USD account commonly costs around 1%, plus transparent conversion at mid-market, making it cheaper for regular invoices.

What documents or compliance do I need to stay RBI and FEMA compliant for USD receipts?

Ensure correct purpose codes, name matching across PAN, Aadhaar, bank, and invoices, and keep an e-FIRA for every inward remittance. India-focused platforms like Karbon Business generate e-FIRA automatically, simplifying CA and tax filings.

How do I avoid short credits due to intermediary bank fees on SWIFT wires?

Ask your client to use OUR instructions so the sender pays all fees. Include a contract clause that you must receive the full invoice amount, and verify the first payment before proceeding with future transfers.

Can I hold USD and convert later to get a better USD to INR rate?

Yes, many fintechs let you hold USD for up to 60 days. If you expect the rupee to weaken, timing conversion can increase INR proceeds. Use this prudently and consider your cash flow needs.

How can I reduce total costs if my client insists on card payment links?

Price card fees into your quote, typically 3 to 4% or more for international cards. Offer ACH to your virtual USD account as a cheaper alternative in your proposals. If card is unavoidable, keep amounts small and avoid using it for large invoices.

What is e-FIRA and why is it important for freelancers receiving money from the USA?

e-FIRA is the electronic Foreign Inward Remittance Advice, official proof that you received foreign currency for export of services. Your CA will need it for ITR and GST audits. Platforms like Karbon Business generate e-FIRA automatically, saving time and compliance risk.

How do I explain fees and FX to my US client so they agree to ACH instead of wire?

Share a simple comparison showing that ACH to your virtual USD account costs them little, while SWIFT wires create hidden intermediary deductions and slower settlement. Show how mid-market FX with a flat fee keeps more money on your side and smooths their AP workflow.

Is it okay to receive USD payments in my personal account or should I use a business account?

Use an account that matches your invoicing legal name and KYC. Mismatches between personal and business names can trigger compliance holds. India-focused platforms onboard you properly and ensure name matching across documents.