Key takeaways

- Pick Payoneer if you rely on marketplace payouts like Upwork or Fiverr, want free e FIRA, and prefer holding USD, EUR, or GBP balances.

- Pick Wise for direct client invoices, clearer fees, better conversion at mid market rates, and faster INR credits on most transfers under 10,000 dollars.

- Typical total costs: Wise about 1.6 to 1.8 percent, Payoneer about 2 to 3 percent for many flows, but can climb toward 6.2 percent on cards or SWIFT heavy routes.

- Wise auto converts to INR for Indian entities, you cannot hold foreign currency, Payoneer lets you hold and time your conversion.

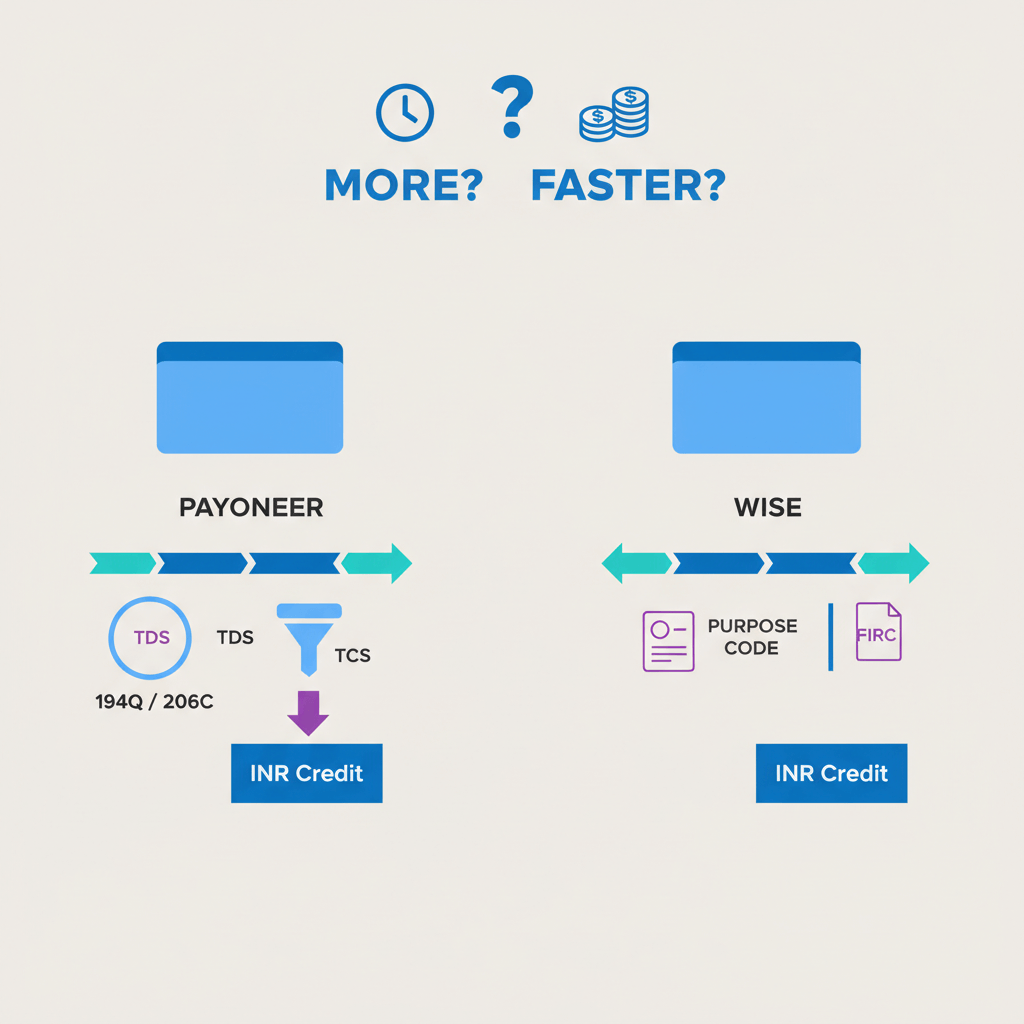

- Withdrawals to Indian banks: Wise often settles in one to two business days, Payoneer in two to four business days.

- Compliance: Payoneer auto issues free digital FIRA equivalents, Wise charges per e FIRA, plan your paperwork accordingly.

- Always run a live quote before choosing a route, small changes in rates or fees can swing thousands of rupees on large invoices.

- India first alternatives like Karbon Business combine automatic e FIRA, mid market rates at zero FX markup, and 24 to 48 hour INR settlement.

Why this matters

If you have ever stared at two dashboards wondering which one will actually put more rupees in your bank account faster, you are not alone. Both tools work for Indian freelancers, consultants, and agencies, yet fees, forex, and documentation differ in important ways. The goal is simple, more INR, fewer delays, cleaner compliance.

Bottom line: compare total cost, conversion rate, and time to INR, then decide. A cheaper receive fee can be cancelled out by a weaker rate, and vice versa.

Quick decision summary

Choose Payoneer if you rely on marketplace payouts with built in integrations, want free e FIRA, and like the option to hold USD, EUR, or GBP before converting. It excels at marketplace simplicity and compliance.

Choose Wise if you invoice clients directly through local rails like ACH or SEPA, want mid market conversion and lower all in costs for small to medium transfers, and prefer faster INR settlement. Note that Wise converts to INR automatically for Indian entities.

For a neutral overview, see the Skydo comparison.

How Payoneer works for Indian businesses

Payoneer issues Global Payment Service details for USD, EUR, and GBP that look like local account numbers. You can connect marketplaces, receive client payments, then convert and withdraw to your Indian bank.

- KYC: GSTIN, PAN, and bank proof, usually verified in one to three days.

- Receiving: ACH into USD often costs about one percent, SEPA for EUR and UK local for GBP are often free, SWIFT can be costly.

- Holding and conversion: You may hold balances, then convert with a markup of about 0.5 to 3 percent over mid market.

- Compliance: Free digital FIRA equivalents for most transactions, GST invoices on fees.

More color in the Skydo comparison.

How Wise Business works for Indian businesses

Wise offers local account details for major currencies, free receiving where supported, and clear conversion fees. Indian entities face a few limits like automatic INR conversion, no debit card access, and restricted outbound transfers. There is also a per invoice cap of 10,000 dollars.

- KYC: Entity documents and GSTIN, typically verified in one to two days.

- Receiving: Local methods like ACH or SEPA are usually free, SWIFT has a fixed fee, e FIRA costs extra.

- Auto conversion: Funds convert to INR on arrival, removing the ability to time your forex.

For context on alternatives, scan this Winvesta guide to Payoneer alternatives.

Core comparison of fees

Fees come from receiving, converting, withdrawing, and sometimes intermediary banks.

- Receiving: See Payoneer fees in India for common charges like one percent on ACH to USD and higher on cards. Wise usually charges zero for local receives, a fixed amount for SWIFT, and a small fee for e FIRA.

- Conversion: Payoneer applies a spread of about 0.5 to 3 percent over mid market. Wise shows the mid market rate, then adds a transparent fee, often between 0.3 and 1.8 percent.

- Withdrawal: Payoneer may charge up to about 3 percent or a flat sum by amount, Wise charges a small variable percentage.

- Hidden costs: SWIFT intermediary deductions and 18 percent GST on platform fees for both.

Independent takes like the Xflow comparison arrive at a similar conclusion, Wise tends to be cheaper for direct client payments, Payoneer can be cheaper for marketplace flows.

Core comparison of conversion rates

Conversion can dwarf flat fees. A two percent weaker rate on a five thousand dollar invoice costs several thousand rupees.

- Payoneer: You can hold and time conversions, yet the spread over mid market reduces the final INR.

- Wise: Uses the mid market rate you see on Google, then a visible fee, auto converts to INR for Indian entities.

Worked examples in resources like the HiwiPay guide generally show Wise yielding more INR per dollar on non marketplace payments.

Core comparison of withdrawal times

- Receipt to wallet: Wise often processes within one to two days, Payoneer about two to four days depending on route.

- Wallet to Indian bank: Wise typically one to two business days, Payoneer about two to three business days.

- End to end: Wise often completes in two to three days, Payoneer in three to six days, timing shifts around weekends and bank holidays.

See the benchmarks in the Exiap comparison.

Business features and usability

- Invoicing: Both provide basic invoicing and payment links, Payoneer is stronger for marketplace pulls and auto paperwork.

- Local account details: Both provide details for USD, EUR, GBP, though Wise limits Indian entities to auto converted balances.

- Accounting: Both connect to major tools, Payoneer eases reconciliation with auto FIRA, Wise needs a manual e FIRA download.

- Support: Ticket based for both, typical response times in a couple of days.

Pro tip, match the legal name on your platform, bank, and GST exactly. Minor mismatches can stall credits for weeks.

Compliance and documentation that matter

- e FIRA and FIRC: Payoneer auto generates free digital FIRA equivalents. Wise charges a small fee per certificate, which adds up over many small invoices.

- RBI and FEMA: Use purpose code 102 for export of services, store invoices, contracts, and email trails for seven years.

- Best practices: Save every e FIRA and GST invoice with a clear naming format, for example ClientName, InvoiceNumber, Date.

Worked example, the INR you actually receive

Scenario: You invoice five thousand dollars via ACH, mid market is about ₹83 per dollar.

- Payoneer route: About one percent receive fee leaves four thousand nine hundred fifty dollars, a two percent FX markup implies an effective ₹81.34, roughly ₹4,02,633. A two percent withdrawal cost trims more, ending near ₹3,94,580. Time, about two to three business days after conversion.

- Wise route: Local receive is free, a total fee near 1.6 percent implies an effective about ₹81.67, roughly ₹4,08,350. A small withdrawal fee brings you near ₹4,06,308. Time, one to two business days after conversion.

Independent comparisons like Exiap echo this pattern, Wise tends to deliver more INR on direct client payments at these sizes.

How to choose, a simple decision path

- Are you paid mainly by marketplaces? Yes, choose Payoneer.

- Do you want free e FIRA for every transaction? Yes, choose Payoneer.

- Are most payments direct bank transfers from clients, and you want the lowest total cost? Yes, choose Wise.

- Do you need the fastest INR credit? Yes, choose Wise.

Mini experiment: Send a 100 dollar test on both, download documents, compare INR received and time to credit. Let the data decide.

Step by step setup for Indian businesses

Payoneer setup

- Register a business account, choose business during sign up.

- Upload PAN, GST certificate, and bank proof.

- Wait for verification, usually one to three days.

- Enable Global Payment Service for USD, EUR, GBP details.

- Link marketplaces, send or receive a small test, then withdraw to INR.

Wise setup

- Open a Wise Business account, submit entity documents and GSTIN.

- Wait one to two days for verification.

- Share local details with clients if eligible, note India specific limits.

- Receive a small test, withdraw to INR, download e FIRA.

On both, use descriptive invoice lines like software development services, attach contracts on first payments, and avoid vague terms like payment that can trigger reviews.

India first alternatives to consider

- Karbon Business offers virtual USD, GBP, EUR, and CAD accounts with local rails, INR settlement in 24 to 48 hours, automatic e FIRA within a day, a flat one percent platform fee, zero FX markup at mid market rates, the ability to hold currency for up to sixty days, and WhatsApp friendly tracking.

- Wise Business remains strong for transparent mid market rates and broad currency support, with Indian limits noted above.

- Payoneer remains a go to for marketplace payouts and free e FIRA.

- PayPal Business is convenient for small invoices, fees are higher in total.

- RazorpayX International can work for startups with GST compliant invoicing.

Test a small invoice across two options, measure net INR and time to credit, then standardize on the winner.

Pitfalls and troubleshooting for Indian users

- SWIFT deductions: Ask clients to use ACH for USD or SEPA for EUR to avoid intermediary fees, share local account details, not SWIFT, when possible.

- Purpose code issues: Use 102 for export of services, if a credit shows pending verification, contact your bank with invoice and e FIRA right away.

- Name mismatches: Align names across platform, GST, PAN, and bank records.

- First payment reviews: Start with 100 to 500 dollars, attach a contract, build history before larger amounts.

- Weekend lag: Plan conversions early in the week for same week credit.

- Large first invoices: Inform the platform before a big first payment, use clear service descriptions, for example UI or UX design for mobile app.

Deeper reading, see the Skydo comparison for additional context.

Making your final decision

If you run most earnings through marketplaces and want hands off compliance, Payoneer is likely simpler even if fees are a bit higher. If you invoice clients directly and care about every rupee, Wise typically nets more INR and pays out faster.

Prefer an India first flow with auto e FIRA, zero FX markup, and chat friendly support, try Karbon Business alongside one global option, then keep the one that consistently pays more, faster, with less admin.

Ignore the marketing and run the numbers, your own 100 dollar test, your own timing. Let that evidence guide your stack.

FAQ

Wise vs Payoneer, which gives better rates and lower fees for Indian freelancers?

For direct client payments, Wise usually wins because it converts at the mid market rate with a transparent fee that often lands between 0.3 and 1.8 percent, while Payoneer uses a spread over the mid market and can be costlier overall. For marketplace payouts, Payoneer may be cheaper on the receive side, which can balance out the spread depending on your mix.

Can I hold USD or EUR as an Indian business on Wise or Payoneer?

With Wise in India, balances auto convert to INR on arrival, so you cannot hold foreign currency. With Payoneer, you can hold USD, EUR, or GBP in your wallet and convert later. If you want a middle ground with hold plus auto e FIRA, consider Karbon Business which allows holding for up to sixty days.

How long does it take to get money into my Indian bank from Wise or Payoneer?

Wise typically lands INR in one to two business days after a payment clears, while Payoneer often takes two to four business days. End to end from client pay to bank credit, Wise often completes in two to three days, Payoneer in three to six days.

Does Wise provide e FIRA or FIRC for Indian freelancers, and what does it cost?

Yes, Wise offers e FIRA for Indian receipts, but it charges a small fee per certificate which you download manually. Payoneer generally auto issues a free digital FIRA equivalent for most transactions. Platforms like Karbon Business auto issue e FIRA within about a day at no extra charge.

What purpose code should I use for export of services when receiving international payments?

Use purpose code 102 for export of services, keep invoices, contracts, and email trails for seven years, and make sure your CA or accountant stores your e FIRA and GST invoices for every payment to avoid bank queries later.

Is there any per invoice cap or limit on Wise for Indian business accounts?

Yes, Indian Wise Business accounts often have a per invoice cap of about 10,000 dollars for incoming transfers. Payoneer does not publish a strict invoice limit for most users, yet very large first payments can still trigger reviews on any platform.

Which is better for Upwork or Fiverr withdrawals, Payoneer or Wise?

For marketplace withdrawals, Payoneer is usually the easier and cheaper route because of native integrations and low or zero receive fees, plus auto e FIRA. Wise can still work for direct client invoices, where its mid market pricing shines.

Will SWIFT transfers eat into my payout on either platform?

Yes, SWIFT often incurs intermediary bank charges that reduce the amount you receive, regardless of platform. Ask clients to pay via ACH for USD or SEPA for EUR and GBP, or use a provider like Karbon Business that gives local account details to avoid SWIFT wherever possible.

What documents do I need for business KYC on Wise or Payoneer in India?

Expect GSTIN, PAN, and bank proof at a minimum, plus entity formation documents for companies. Name and address must match across records. Wise verifies in about one to two days, Payoneer often in one to three days.

I send small invoices under 500 dollars, which platform makes more sense?

For small direct invoices, Wise tends to be cheaper due to mid market rates and low percentage fees, so you usually net more INR. If you want auto compliance documents without extra steps, Payoneer or Karbon Business may save you time even if the fee difference is small.

How do I avoid payment holds or compliance freezes on my first large invoice?

Warm up your account, start with a 100 to 500 dollar test, use clear descriptions like software development services, attach a basic contract, and notify support if you expect a first payment above 5,000 dollars. This applies to Wise, Payoneer, and even India first platforms like Karbon Business.

Between Wise, Payoneer, and Karbon Business, which puts the most INR in my bank for direct client work?

It depends on amounts and routes, but for many freelancers Wise wins on pure FX math for direct transfers, Payoneer can win on marketplace flows due to low receives and free e FIRA, while Karbon Business often balances both by using mid market rates with zero markup, a flat platform fee, and automatic e FIRA, which can net out better once you include documentation costs and time saved.