Key takeaways

- Liberalized Remittance Scheme lets resident individuals invest abroad within an annual LRS limit of USD 250,000 per financial year.

- Permitted investments include foreign stocks and ETFs, bonds, overseas real estate, foreign currency accounts, and equity in overseas businesses.

- Documents you will need include PAN, KYC, Form A2 with the correct purpose code, bank statements, and purpose specific proofs.

- For most investment remittances, banks collect 20 percent TCS beyond INR 7 lakh, which you can claim as credit in your income tax return.

- Costs include forex markup, bank wire fees, and time to settle via SWIFT, usually one to three business days.

- Report foreign assets in Schedule FA, keep FIRCs and statements for at least seven years, and claim foreign tax credit for taxes paid overseas.

- Use authorized channels and compliant platforms, for example Karbon Business, to streamline documentation, rates, and reconciliation.

What is the Liberalized Remittance Scheme LRS?

The Liberalized Remittance Scheme is a Reserve Bank of India framework that allows resident individuals to send money abroad for permitted purposes without seeking specific RBI approval. Introduced in 2004, it enables global participation for ordinary Indians across investments, education, travel, medical treatment, gifts, and more. The scheme is limited to resident individuals, including minors, and excludes corporations, partnership firms, HUFs, and trusts.

Understanding the annual LRS limit

Each resident individual can remit up to USD 250,000 per financial year across all permitted purposes combined. The limit resets on April 1. Minors have their own separate limit, so a family of four could collectively remit up to USD 1 million in one year if each purpose is legitimate and documented. For deeper context, review this helpful overview of LRS limits 2024 to 2026.

Permitted investment categories under LRS

Equity and debt instruments

Invest in foreign stocks on recognized exchanges, mutual funds, ETFs, bonds, and other securities. Many Indian investors use LRS to gain exposure to US technology stocks, global index funds, or diversified international portfolios unavailable domestically.

Real estate abroad

Purchase residential or commercial property overseas, excluding agricultural land, farmhouses, or plantation assets where restricted.

Foreign currency accounts

Open and maintain bank accounts, including deposits and fixed deposits, with banks outside India for legitimate purposes.

Setting up companies and direct investments

Make direct investments, or set up wholly owned subsidiaries abroad, subject to conditions and reporting requirements. Prohibited uses include trading in foreign exchange, lottery purchases, or any activity violating FEMA.

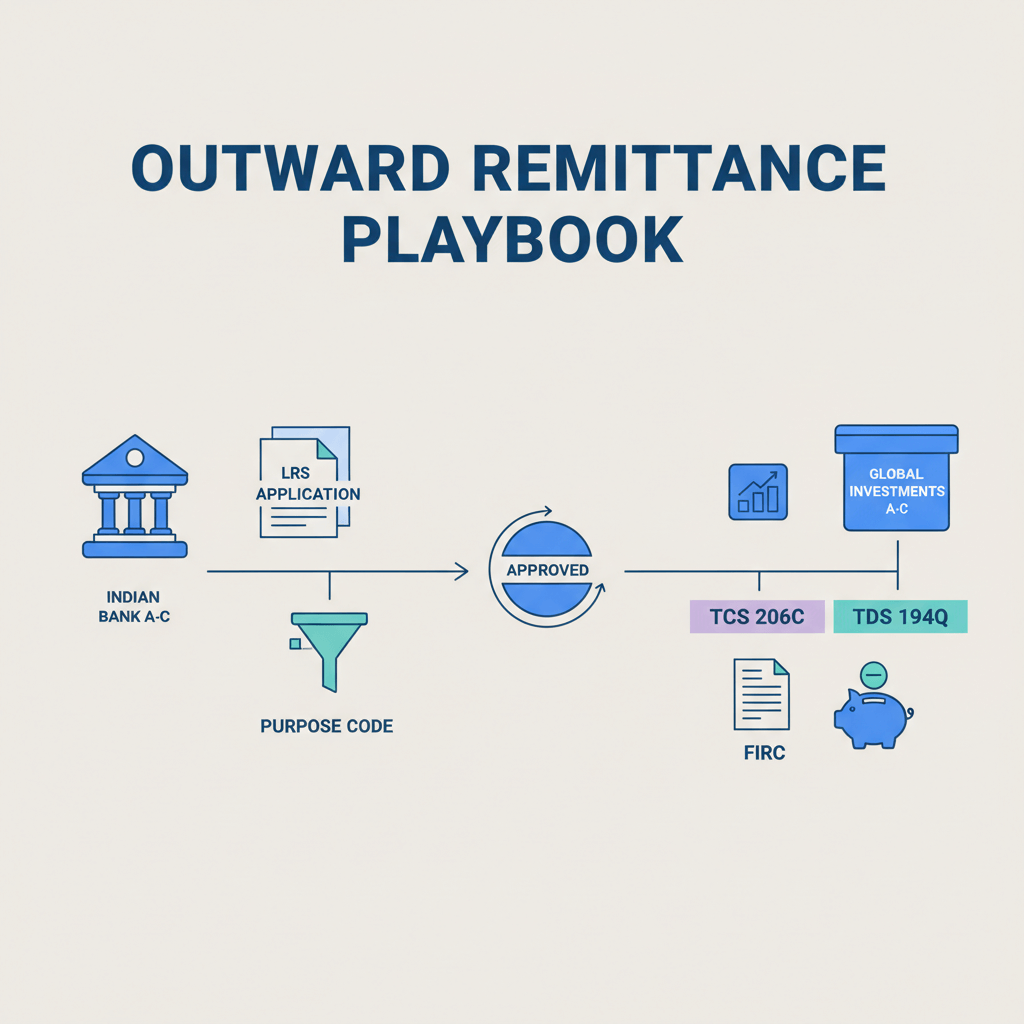

Required documentation for outward remittance

Identity and address proof

Provide PAN as mandatory identification, plus KYC documents such as Aadhaar, passport, voter ID, or driving license.

Form A2 and declaration

Submit Form A2 for each remittance with purpose code, amount, and beneficiary details, along with a self declaration confirming LRS compliance and adherence to the annual limit.

Purpose specific documents

- Stocks and funds, broker or platform account opening confirmation.

- Real estate, sale agreement, deed, or payment schedule.

- Business investment, incorporation papers, share certificates, or investment agreements.

Bank statements

Banks generally seek three to six months of statements to verify source of funds as part of anti money laundering checks.

Step by step process for making an outward remittance

Step one, choose your bank or authorized dealer

Pick a bank branch with a strong forex desk, or an authorized dealer, or a compliant fintech that supports outward remittances for investments. Fintechs often offer sharper rates and faster digital journeys.

Step two, submit documents and forms

Provide Form A2, KYC, and supporting documents. Select the correct purpose code to avoid downstream issues. Refer to this comprehensive purpose code list for outward remittance. Double check beneficiary details, SWIFT, and account numbers to prevent delays.

Step three, tax collection at source TCS

For investments, a 20 percent TCS typically applies on remittances beyond INR 7 lakh in a financial year, collected by the bank at the time of transfer. This is not extra tax, it is creditable in your income tax return. Education and medical remittances can have lower rates or exemptions up to INR 7 lakh, but investments generally do not.

Step four, currency conversion and transfer

After compliance checks, INR is converted at the bank’s exchange rate, which includes a markup, plus wire fees. Transfers are typically sent via SWIFT, settling same day to three business days depending on corridor and checks.

Step five, receive funds abroad

Ensure you obtain a Foreign Outward Remittance Certificate or equivalent proof. Preserve all records, Form A2 copies, bank statements, and investment confirmations for future audits.

Pro tip, before large transfers, compare all in costs across providers, forex markup plus fees, and ask for a net of fees quote to the beneficiary account.

Tax implications and compliance

Tax on foreign investment income

As a resident, worldwide income is taxable in India. Dividends and short term gains are taxed at slab rates, while long term capital gains on foreign equity are taxed at 20 percent with indexation. Where foreign tax is withheld, claim foreign tax credit under DTAA to avoid double taxation.

TCS credit in ITR

The bank collected TCS appears in Form 26AS and AIS. Claim it as tax already paid while filing, reducing net liability or generating a refund if excess.

Foreign asset reporting

Report foreign assets in Schedule FA, bank accounts, securities, immovable property, and other capital assets. Disclose even if no income accrued. Non disclosure can invite significant penalties under the Black Money Act.

Common mistakes to avoid

- Exceeding the annual limit, track your cumulative remittances across banks to stay within USD 250,000.

- Using funds for prohibited purposes, stick to permitted investments and jurisdictions.

- Incorrect purpose codes, choose carefully to prevent regulatory mismatches and tax issues.

- Poor record keeping, store FIRCs, Form A2, statements, and confirmations for at least seven years.

- Ignoring repatriation rules, understand documentation when selling assets and bringing funds back.

Popular platforms and brokers accepting LRS transfers

US stock brokers

Interactive Brokers, Charles Schwab International, and TD Ameritrade accept international clients, providing access to US stocks, ETFs, options, and bonds.

Global investment platforms

Vanguard for mutual funds, Saxo Bank, and eToro offer broader access to Europe and Asia.

Real estate investment

Funds are sent to seller or escrow per the agreement, coordinating with local agents, lawyers, and banks.

Foreign bank accounts

Banks such as Citibank, HSBC, Standard Chartered, and DBS offer foreign currency accounts that can be funded via LRS and then used for investments or payments.

Tools and platforms for managing remittances

Digital platforms can streamline rate discovery, documentation, and reconciliation. Karbon Business supports international payment needs with competitive forex rates and compliance assistance, Wise Business offers multi currency accounts with transparent exchange, while marketplaces like BookMyForex and ExTravelMoney help compare bank quotes. For students and first time remitters, providers like RemitOut and Niyo Global focus on simpler, mobile first experiences.

Recent changes and updates to LRS rules

TCS rate changes

TCS has evolved over time, rising to 20 percent on many investment and tour remittances. Always verify the prevailing rate before initiating a transfer.

Digital reporting improvements

Banks now provide online LRS limit trackers and increasingly support end to end digital remittances, improving transparency and speed.

Sector specific restrictions

At times, the RBI may tighten scrutiny for certain destinations or purposes based on macroeconomic conditions. Expect extra checks during periods of currency volatility.

Planning your international investment strategy

Assess your investment goals

Clarify whether you are seeking diversification, access to specific sectors, retirement planning, or education funding. Your goals guide allocation and risk.

Understand currency risk

Returns are impacted by both asset performance and INR movement. Consider timing remittances, or holding some foreign currency assets as a hedge.

Factor in all costs

Include bank fees, forex markup, TCS cash lock in, broker commissions, and account fees. Small tickets can suffer from proportionally higher costs.

Plan for tax efficiency

Study treaty benefits, dividend withholding, capital gains, and estate rules in the destination. Complex cases merit a cross border tax advisor.

Build a repatriation strategy

Plan documentation and timelines for bringing proceeds back to India. Some investors keep a portion abroad for long term diversification.

Compliance best practices for long term LRS users

- Maintain a master tracker, log date, purpose, currency, purpose code, bank, TCS, and status for every remittance.

- Organize documents by year, store Form A2, FIRCs, statements, and tax proofs digitally and physically.

- File accurate returns, share full foreign income and asset details with your CA to ensure correct Schedule FA and FTC claims.

- Review updates annually, each April, verify changes in limits, codes, and TCS.

- Use authorized channels only, never use informal routes, these violate FEMA and attract severe penalties.

Conclusion

Outward remittance under LRS gives Indian investors a practical route to global markets. By understanding limits, permitted uses, documentation, TCS treatment, and reporting, you can invest confidently while staying compliant. Combine careful planning with meticulous records and competitive channels, and LRS becomes a powerful tool to build a truly global portfolio.

FAQ

I am an Indian freelancer, how do I receive USD from clients and does that count under LRS?

Receiving international payments from clients is an inward flow, it does not use your LRS limit. You can accept funds via compliant platforms or bank inward remittances, then if you want to invest abroad or pay for tools in foreign currency, that outward leg would use LRS. Platforms like Karbon Business can help streamline compliant collections and reconciliations.

Which is the cheapest and safest way to pay for foreign SaaS tools from India under LRS?

Use a bank or authorized dealer that supports outward remittances for services, select the correct purpose code, and compare forex markups plus fees. Fintechs that integrate with banks, for example Karbon Business, can offer competitive rates, invoice support, and audit trails, which reduce total cost and compliance friction.

Can I invest my freelancing income in US stocks using LRS, what documents are needed?

Yes, resident individuals can invest up to USD 250,000 per year. You will need PAN, KYC, Form A2 with the investment purpose code, recent bank statements, and proof of your brokerage account. Keep FIRC and trade confirmations for records. If you use a workflow with Karbon Business for funding, ensure the outward transfer maps to the correct code.

Do I have to pay 20 percent TCS on every international payment I make as a freelancer?

No, TCS applies to outward remittances under LRS beyond INR 7 lakh in a year for specified purposes, and rates differ for education and medical. For investment related remittances, 20 percent typically applies and is claimable as credit in your ITR. Inward receipts from clients are not subject to TCS.

What purpose code should I pick for paying a US based contractor or designer from India?

Service payments have dedicated purpose codes, which must be selected accurately on Form A2. Refer to the official purpose code list, and when in doubt, ask your bank’s forex desk or a CA. Platforms with compliance support, such as Karbon Business, can guide you on correct coding and documentation.

How long do outward remittances take, and how do I track them end to end?

International wires usually settle within one to three business days via SWIFT, depending on corridor and checks. Ask your bank for a UTR or SWIFT reference, and maintain Form A2 and FIRC. A unified dashboard from providers like Karbon Business helps track statuses, references, and reconciliations in one place.

If I get paid in USD, can I keep funds abroad and pay for tools directly without bringing money to India?

As a resident Indian, FEMA places conditions on holding funds outside India. You can open and fund foreign currency accounts under LRS for permitted purposes, but consult your CA to ensure proper disclosures in Schedule FA. Many freelancers prefer receiving in India, then remitting outward for tools or investments using compliant channels like Karbon Business.

What is the total cost of an outward remittance, and how do I reduce forex markup?

Total cost includes the bank’s forex markup, wire fees, correspondent charges, and any TCS cash lock in. To reduce it, compare multiple provider quotes, ask for all inclusive rates, batch smaller payments where practical, and remit during market hours for tighter spreads. Fintech assisted remittances via Karbon Business often secure competitive rates and transparent fees.

Will my foreign investment income from US stocks be taxed in India, and how do I claim credits?

Yes, residents must report worldwide income. Dividends and short term gains are taxed at slab rates, long term gains on foreign equity at 20 percent with indexation. Claim foreign tax credit for withholding in the US as per DTAA. Keep broker statements and 1042-S or similar proofs, and match them with your Indian ITR. Your TCS credits from remittances also appear in Form 26AS.

Can I use LRS to buy crypto on an overseas exchange from India?

The regulatory position is cautious, and many banks do not process remittances explicitly marked for crypto. Some investors route funds to foreign currency accounts and then invest, but this can sit in a grey zone. Consult a qualified advisor before attempting any such transfer, and prioritize clear purpose coding and documentation.

As a freelancer, how do I stay compliant with Schedule FA and audits when I invest abroad?

Maintain a master tracker of remittances, purpose codes, amounts, and TCS, store all FIRCs, Form A2, broker and bank statements, and disclose all foreign assets in Schedule FA, even if there is no income. Solutions like Karbon Business can help centralize documentation and export audit ready reports.

Is pooling LRS limits with my spouse or teammates allowed for a single investment abroad?

No, LRS is individual specific. Each person may remit up to USD 250,000 for their own permitted purpose, with proper documentation and PAN. You cannot remit on someone else’s behalf, but multiple family members can invest separately, each within their limit and with their own paperwork.