Key takeaways

- The LRS limit is USD 250,000 per financial year for each resident individual, it applies across all banks and fintech providers.

- Both current account and capital account transactions are permitted, think travel, education, medical, gifts on one side, investments, property, business on the other.

- Forex card loads, tuition wires, overseas tour packages, and foreign investments count toward your aggregate LRS usage.

- International credit card spends while you are abroad generally do not count, always verify the latest bank and RBI guidance before relying on this.

- TCS and LRS are different, TCS is advance tax that you can claim back, LRS is the RBI cap on outward remittances.

- Documentation is mandatory, PAN, Form A2, the correct purpose code, and category specific proofs.

- Common mistakes include misusing purpose codes and forgetting forex loads count, track your year to date dollar total to stay compliant.

- The USD 250,000 limit remains unchanged for FY 2026–27, plan across financial years and watch for Budget or RBI updates.

LRS in 60 Seconds (Primer)

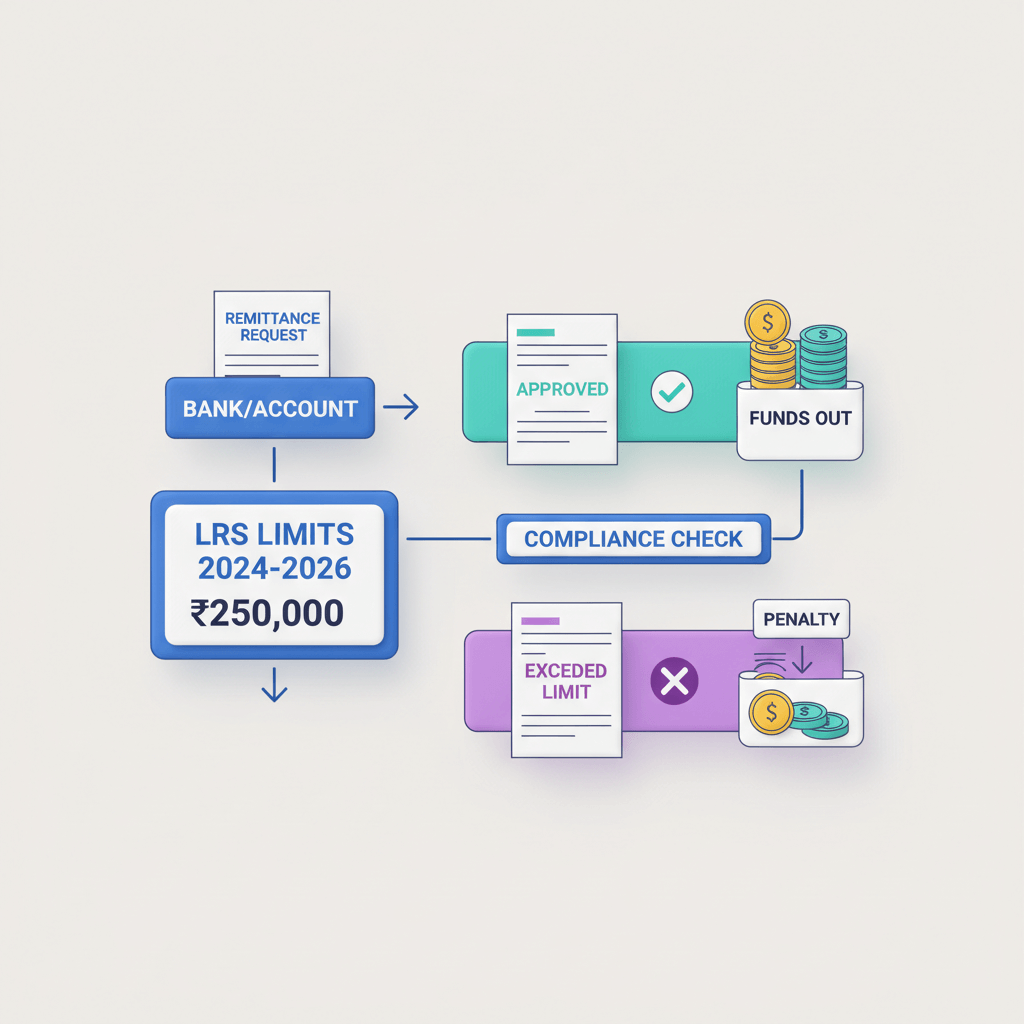

The Liberalised Remittance Scheme, or LRS, lets resident individuals remit money abroad for permitted purposes without prior case by case RBI approval, up to a generous annual cap. The current LRS limit is USD 250,000 per financial year, April to March, and it aggregates across all authorized dealer banks and platforms.

Who can use LRS: any resident Indian, including minors with a guardian signing Form A2. Companies, HUFs, and non residents cannot use LRS.

What it is not: you do not need prior RBI permission within the limit, but if you need to remit more than USD 250,000 in a year, you must seek specific RBI approval.

Think of LRS as your annual quota to move money for education, travel, medical needs, gifts, investments, or property, all within a single cumulative cap.

For a friendly overview, see the Liberalised Remittance Scheme guide.

LRS Categories, with Everyday Examples

The RBI groups LRS into two buckets, current account and capital account transactions, the labels are technical, the use cases are familiar.

Current account transactions

- Private travel: loading a forex card for a Thailand trip, buying currency notes, paying for an international tour package.

- Gifts and donations: sending a wedding gift to a cousin in Canada.

- Maintenance of close relatives abroad: regular support transfers for parents settled overseas.

- Medical treatment: paying overseas hospital bills.

- Education fees: tuition, hostel fees, living expenses for a student abroad.

- Emigration: visa application charges, consultant fees, initial settlement funds.

Capital account transactions

- Investments in foreign securities: US stocks, ETFs, mutual funds, or bonds.

- Opening foreign currency accounts: USD, GBP, or EUR accounts abroad.

- Property purchase overseas: apartments, holiday homes, where permitted.

- Joint ventures or wholly owned subsidiaries: setting up or expanding business operations abroad.

Prohibited uses include lottery, gambling, certain margin trading, transactions to high risk jurisdictions, and bank restricted crypto remittances.

For more on categories and practical do’s and don’ts, see what is LRS for residents.

What Counts Toward the LRS Aggregate Limit

All permitted remittances add up to your USD 250,000 aggregate limit across all banks and platforms. The RBI tracks your total, not per bank usage.

- Bank wires, telegraphic transfers, or SWIFT payments with an LRS purpose code.

- Loading debit cards, forex cards, or prepaid travel cards for overseas use.

- Paying for overseas tour packages, even if the agent is in India.

- Transfers to your own account abroad, or to close relatives for maintenance.

- Investments in foreign stocks, bonds, mutual funds, or ETFs.

- Purchasing currency notes or loading a forex card before travel.

Example: June, USD 50,000 for tuition, August, USD 10,000 forex card load, November, USD 100,000 for US stocks. Total LRS usage equals USD 160,000, headroom left equals USD 90,000.

Remember, the cap is cumulative across categories, banks, cards, and the entire financial year.

What Doesn’t Count Toward the LRS Limit

Some transactions sit outside LRS, here is what generally does not count.

- International credit card spends while you are abroad: hotel, meals, shopping, usually outside LRS, verify your bank’s latest guidance.

- INR payments to Indian entities for domestic services: domestic packages do not count, overseas packages through Indian agents often do.

- Transactions by non residents or firms: these are not eligible under LRS.

- Prohibited uses under FEMA: lottery, gambling, and bank restricted crypto remittances.

- Crypto grey area: most authorized dealers decline crypto related remittances, confirm before attempting.

| Counts Toward LRS Aggregate Limit | Doesn’t Count Toward LRS Limit |

|---|---|

| Forex card loads for travel | Credit card spends abroad, subject to latest policy |

| Direct tuition wire transfers | INR payments for domestic services |

| US stock purchases via a broker | Prohibited uses like lottery or gambling |

| Overseas tour packages | Transactions by non residents or companies |

| Transfers to relatives abroad for maintenance | Many crypto transactions, bank dependent |

Policy evolves, especially for card spends and travel packages, always check your bank and recent RBI circulars before large payments.

TCS vs LRS, do not mix them up

LRS limit is the RBI cap on outward remittances, USD 250,000 per year. TCS is tax collected at source, in rupees, once your eligible foreign spends cross the threshold.

Budget 2025 raised the TCS free threshold to Rs 10 lakh for most purposes. Below Rs 10 lakh in the year, no TCS. Beyond that, rates vary by category, lower for education and medical with documentation, higher for tour packages and other uses.

Crucial point: TCS is advance tax, visible in Form 26AS and AIS, you can claim credit in your ITR.

For a clear explainer, see TCS foreign remittance guidance.

How to Calculate and Track Your LRS Headroom

Use a simple three step approach to stay within the cap.

- List all LRS transactions for the year, include purpose code, INR amount, and date.

- Convert to USD at your bank’s rate on the transaction date, then sum across banks and categories.

- Subtract from USD 250,000 to find your remaining headroom.

Tracking tips

- Maintain a spreadsheet, columns for date, category, INR, USD, and year to date total.

- Request a year to date LRS statement from each authorized dealer bank.

- Save signed Form A2 copies and transaction slips.

Family limits: each resident individual has a separate USD 250,000 cap. Do not club limits for capital transactions, keep individual ledgers separate.

| Date | Category | Purpose Code | INR Amount | USD Equivalent | YTD USD Total |

|---|---|---|---|---|---|

| 15-Apr-2025 | Education | S0201 | ₹40,00,000 | 48,000 | 48,000 |

| 10-Oct-2025 | Travel card | S0301 | ₹8,00,000 | 9,500 | 57,500 |

| 20-Dec-2025 | Investment | S0001 | ₹50,00,000 | 59,000 | 116,500 |

Remaining headroom equals USD 250,000 minus USD 116,500, which is USD 133,500.

Reporting and Documentation, what to expect

Every LRS transaction needs correct paperwork, banks enforce KYC and AML checks, especially for large amounts.

Mandatory requirements

- PAN for every LRS transaction.

- Form A2, declaration of purpose, amount, and beneficiary.

- Purpose code, for example S0201 for education, S0301 for travel, S0001 for investments.

- KYC and AML checks, identity verification and source of funds where needed.

- Form 15CA and 15CB for certain capital account or investment remittances, your bank will guide you.

Supporting documents by category

- Education: admission letter, fee invoice, prior payment receipts.

- Medical: hospital estimate, doctor’s referral, treatment plan.

- Property: sale agreement, valuation, legal clearances.

- Investments: broker account confirmation, investment plan details.

- Travel: visa copy if applicable, trip itinerary, forex card application.

- TCS certificates: keep bank issued TCS certificates, verify in AIS or Form 26AS.

Record keeping checklist

- Form A2 copies for every transaction.

- Purpose code proof and supporting invoices.

- TCS certificates from banks.

- Bank remittance statements with applied forex rates.

- Email confirmations from banks or forex platforms.

- Category specific supporting documents.

Retention for at least seven years is prudent for tax and FEMA compliance.

Edge Cases and Common Mistakes

- Splitting across banks does not bypass the limit, the cap is per individual, RBI sees the aggregate.

- Wrong purpose codes invite scrutiny, report accurately, do not mask investments as travel.

- Forgetting forex loads count, card loads and currency purchases add to your total.

- Domestic payments for overseas tours often count, because the underlying service is foreign.

- Attempting prohibited transactions like lottery or crypto remittances gets blocked, can trigger AML flags.

- Uncoordinated family remittances cause confusion, keep ledgers per individual.

LRS Limit 2026, what to expect

As of December 2025, the LRS cap remains at USD 250,000 per financial year, there is no official change announced for FY 2026–27.

- Plan across years for large commitments, spread payments to stay within annual limits.

- Monitor Budget and RBI updates in February and through periodic circulars.

- Keep a forex buffer, rupee moves impact INR cost for the same USD usage.

- Review RBI FAQs regularly before large remittances.

Quick Decision Tree and Checklist

Question 1: are you a resident individual? If yes, proceed, if not, LRS does not apply.

Question 2: is the transaction permitted, education, travel, medical, gifts, investments, property? If yes, proceed, if not, it is not allowed.

Question 3: is it a wire transfer, card load, or tour payment? If yes, it counts toward your aggregate, use Form A2 and the correct purpose code. If it is an international credit card spend while you are abroad, it generally does not count, confirm the latest policy.

- Provide PAN.

- Fill and sign Form A2.

- Attach category specific documents.

- Tag the remittance with the correct purpose code.

- Add the USD equivalent to your year to date total.

- Store copies of all forms and certificates.

Wrapping Up, stay informed, stay compliant

LRS lets resident Indians fund education, travel, medical care, gifts, investments, and property abroad, within a single USD 250,000 annual cap. The keys are correct categorization, careful tracking, proper documentation, and clear separation from TCS. Bookmark this guide, keep meticulous records, and when unsure, consult your authorized dealer bank or a qualified chartered accountant.

FAQ

As a freelancer in India, do I even need to care about LRS when I am receiving payments from foreign clients?

Inbound payments from clients are not LRS, they fall under foreign inward remittance rules, e FIRA, FEMA, and your bank’s export documentation. LRS applies when you send money out, for example, investing in US ETFs or paying a contractor abroad. For receiving client funds, a platform like Karbon Business can help you settle international payments into your Indian account with compliant paperwork.

How do I pay for USD priced software subscriptions or online tools from India, does that fall under LRS?

Yes, outward payments for SaaS or tools are current account transactions under LRS, they count toward your aggregate. If you pay using a forex card or a bank wire, it adds to your LRS usage. If you pay with an Indian credit card while abroad, it generally does not count, verify the latest bank guidance. Karbon Business can route subscription payments through permitted channels with correct purpose codes.

I receive money from Upwork and direct clients, can I still invest part of my earnings in US stocks under LRS?

Yes, investing in foreign stocks, ETFs, or mutual funds is permitted under LRS and counts against your USD 250,000 cap. You will likely need Form 15CA and 15CB, plus Form A2 and the correct purpose code. Karbon Business can help you document remittances cleanly while you keep inbound client payments separate.

Can I pay a US based designer for a one off project from India, what paperwork does the bank ask?

Yes, paying a foreign contractor is a permitted current account remittance, it counts toward LRS. Expect PAN, Form A2, invoice copy, and the correct purpose code. For larger amounts, banks may ask for source of funds. Karbon Business supports outward service payments with streamlined documentation.

Bro, I am planning a Europe trip and also sending money for my sister’s fees, how do I track the combined LRS usage across banks?

Make a simple ledger, date, category, INR, USD equivalent at the bank’s rate, and a running year to date total. Ask each bank for your LRS statement. Your travel forex card loads and the tuition wire both count. Platforms like Karbon Business provide transaction summaries that make it easier to reconcile across providers.

Does TCS eat my money when I pay abroad for ads or tools, how do I claim it back?

TCS is advance tax collected by your bank once your eligible foreign spends in the year cross Rs 10 lakh. You can see it in Form 26AS or AIS and claim credit in your ITR. TCS is not the LRS limit, it is separate. For clarity on collection thresholds and rates, see TCS foreign remittance. Karbon Business provides TCS certificates and reconciliations so you can claim credit easily.

Credit card spends abroad count or not, I am confused, what should I rely on for compliance?

Generally, international credit card spends while you are physically abroad do not count toward LRS, but policy has changed over time. Always confirm with your card issuer and check recent RBI guidance before high value spends. If you are using forex card loads or bank wires, those do count, track them carefully.

Can I remit to my own multi currency account like USD or EUR for business travel and future expenses?

Yes, opening and funding a foreign currency account in your name for permitted purposes is allowed under LRS, it counts toward your cap. Use the correct purpose code and keep statements for audit. Karbon Business can help with clean documentation and reminders for tracking your headroom.

I want to move money to a US brokerage for dollar cost averaging every month, is that okay under LRS?

Yes, periodic investment transfers to a foreign brokerage are permitted capital account transactions under LRS, they add up against your USD 250,000 cap. Prepare Form A2, the right purpose code, and Form 15CA or 15CB where applicable. Karbon Business offers reminders and statements to keep your monthly remits compliant.

If my total outward payments for tools, travel, and investments cross USD 250,000 this year, how do I proceed?

Once you need to go beyond USD 250,000 in a financial year, you must seek specific RBI approval, your bank will guide you on documents and justification. Without approval, you should spread payments across financial years to stay within the cap. Karbon Business can help plan schedules so you remain compliant.

What exactly is the difference between LRS for outward remittance and inward payments I get from US clients?

LRS governs outward remittances by resident individuals. Inward payments are export receipts, they need e FIRA from your bank, invoices, and FEMA compliance, not LRS. Keep two folders, one for outward LRS, one for inward receipts. Karbon Business supports both sides with purpose code tagging and proper records.

How do I keep proofs so that my CA can file ITR and claim TCS credit without drama?

Maintain a digital folder per financial year, include signed Form A2, purpose code proofs, invoices, remittance statements with forex rates, and TCS certificates. Verify TCS in Form 26AS or AIS. Karbon Business lets you export transaction level documents and summary sheets for smooth ITR filing.