Key takeaways

- Resident individuals can invest abroad under the Liberalised Remittance Scheme with a USD 250,000 limit per financial year; see the LRS limits 2024 to 2026 guide for a crisp overview.

- Permitted investments include foreign stocks, ETFs, bonds, and mutual funds, while margin products, gambling, and crypto are restricted.

- Use your personal resident savings account, not a business account, and always declare the correct purpose code, investment in foreign securities.

- Documentation is king, especially for freelancers, so prepare PAN, updated KYC, Form A2 and LRS declaration, broker proof, source of funds, and exact beneficiary details; here is a handy Form A2 checklist.

- TCS at 20 percent applies on total LRS usage above ₹10 lakh in a year, it is not a cost, it adjusts as credit in your ITR; refresh the basics with this LRS and TCS explainer.

- Biggest cost is the FX spread, not bank fees, so compare two or three banks or platforms before sending.

- Typical timelines are one to three business days after bank approval; see this concise LRS for investments process guide for reference.

Why outward remittance for investments under LRS matters

Your first big international payout has landed, and now you want to put that money to work in global markets. Outward remittance for investments under LRS lets Indian residents send money abroad to buy foreign stocks and funds, without prior approval, as long as you stay within limits and follow documentation. With a bit of preparation, you can fund your overseas brokerage smoothly, avoid rejections, and start investing with confidence.

Understanding LRS basics, your gateway to global investing

LRS, or Liberalised Remittance Scheme, allows resident individuals, including minors through guardians, to remit funds abroad for permitted current and capital account transactions. The annual limit is USD 250,000 per financial year, April to March, across all purposes combined. For current thresholds and examples, check the LRS limits 2024 to 2026 guide.

Permitted capital account transactions include buying foreign stocks, ETFs, bonds, and mutual funds, plus opening overseas brokerage accounts. Income from these assets can be retained or reinvested abroad, though direct JV or wholly owned subsidiary investments require extra FEMA compliance.

What you cannot do:

- Margin trading or any leveraged product

- Lottery or gambling

- Cryptocurrency purchases, most banks block these

- Remittances from business accounts, only personal resident accounts qualify

Banks also restrict transfers to sanctioned countries due to AML rules. Always declare your purpose accurately, or your wire may be reversed. For a clear overview of do’s and don’ts, read this LRS overview.

Tip: A rejected remittance can bounce back only after days, and you still pay wire charges, so double check every field before submitting.

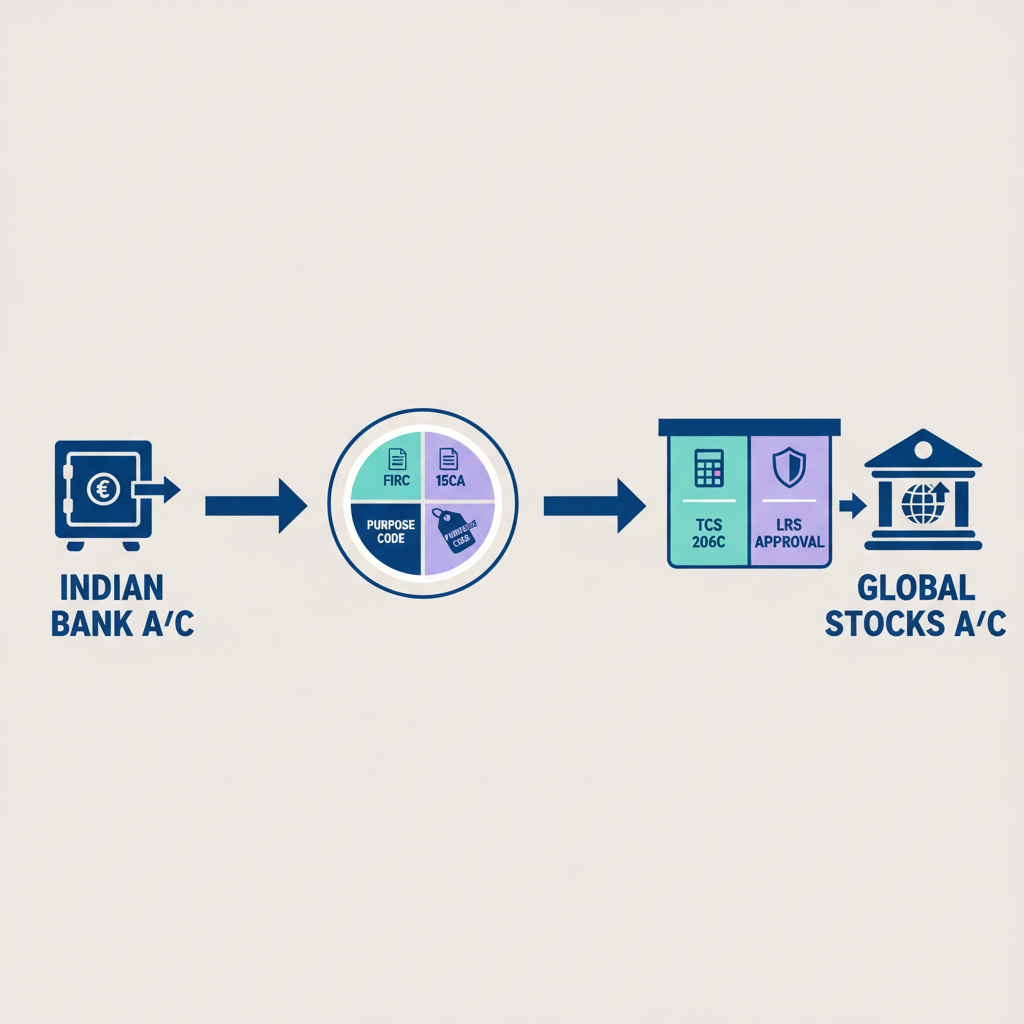

How to remit money for stocks, complete step by step process

Step 1: Open and verify your overseas brokerage account

Complete KYC with your broker, then collect exact beneficiary details, broker name, bank name, account number or IBAN, SWIFT or BIC, address, and your unique client reference or memo. Many brokers use omnibus accounts, so your reference is critical to credit funds to your trading account.

Step 2: Choose your Authorised Dealer bank

Compare FX spreads, total fees, speed, and LRS experience. A one percent difference on INR 10 lakh is INR 10,000, so shop around. Digital platforms can be faster, while global banks often have deeper LRS expertise.

Step 3: Prepare your documentation checklist

- PAN card, mandatory for LRS

- Updated bank KYC

- Form A2 and LRS declaration, most banks offer digital signing, see this Form A2 supporting documents checklist

- Purpose code, investment in foreign securities

- Broker proof, welcome email, account statement, or funding instruction letter

- Source of funds, bank statements, ITR, salary slips, for freelancers, invoices and e FIRA documents

- Form 15CA and 15CB, rarely needed for plain LRS investments, confirm with your bank or CA

For freelancers, source of funds evidence carries extra weight. If your payment platform auto generates e FIRA within 24 hours, like Karbon Business, verification is smoother; more on this in the LRS for investments explainer.

Step 4: Submit your remittance request

Enter beneficiary details exactly as given by your broker. Declare year to date LRS usage accurately. Fund the transfer from your savings account. If your total LRS usage crosses the threshold, TCS applies, which we cover below.

Step 5: Track and confirm receipt

Wire transfers usually credit within one to three business days. If your broker has not confirmed after three days, request a SWIFT copy from your bank and share it with the funding desk. Keep every document for tax and audit trails, see this how to track and document LRS remittances.

Understanding costs, taxes, and TCS on outward remittance

Bank charges breakdown:

- Remittance processing fee, roughly ₹500 to ₹2,000

- SWIFT or wire fee, roughly ₹500 to ₹1,000

- FX spread, often 0.5 percent to 2 percent above mid market, the largest cost

- GST at 18 percent on bank fees

On a ₹5 lakh remittance, expect total costs in the ₹5,000 to ₹15,000 range, primarily driven by FX markup.

TCS, not a cost, but a cash flow hit

The Budget 2025 rules apply TCS at 20 percent on total LRS remittances above ₹10 lakh in a financial year. It appears in your Form 26AS, and you claim it as credit or refund while filing your ITR. Plan liquidity so your remittance does not fail for shortfall.

Taxation on foreign investments:

- Dividends are taxed in India per slab, claim DTAA credit for any foreign withholding

- Capital gains follow holding period rules, short term under 24 months taxed at 20 percent, long term at 12.5 percent with indexation, as per recent changes

- Always disclose foreign assets and income in Schedule FA

Refresh the fundamentals and compliance points in this LRS tax and compliance guide.

Practical examples, real scenarios from Indian investors

Example 1, freelance designer investing ₹5 lakh in US ETFs

Priya, a Bangalore based designer, receives USD payments via Karbon Business and wants to invest through Interactive Brokers. She compiles Form A2, LRS declaration, broker welcome email, ITR, six months statements, and Karbon e FIRAs for source of funds. Fees are around ₹1,800 processing, ₹800 SWIFT, and a one percent FX spread. Her year to date LRS usage is ₹2 lakh, so no TCS. Funds reach in three to four days. Case notes similar to this LRS for investments walkthrough.

Example 2, software engineer funding ESOP exercise

Rahul needs USD 15,000 for his ESOPs. He submits ESOP allotment letter, Form A2, salary slips, ITR. His remittance crosses ₹10 lakh, so TCS applies on the excess at 20 percent. He keeps a buffer to avoid failure, and will claim TCS in next year’s ITR. For bank side FAQs on LRS, see HSBC’s LRS FAQs.

Example 3, content writer building a USD buffer

Meera receives client payments in USD via a virtual account, waits for better rates, converts to INR, then funds her Charles Schwab account through LRS. With auto e FIRAs and zero FX markup on inbound, her compliance trail is clean, and banks process within two days. For LRS basics and disclosures, refer to this LRS overview.

Risk management and good practices for LRS investments

Mitigate FX risk

Stagger transfers over weeks, compare your bank’s rate to mid market rates, and avoid sending everything in one go. A one and a half percent markup on ₹10 lakh is ₹15,000, which you can reduce by shopping around.

Name matching and third party payments

Names on bank account, PAN, and broker account must match exactly. Third party credits are rejected. Your client reference or memo is non negotiable, get the format right or your funds sit unallocated.

Documentation archive system

- A2 forms and LRS declarations

- SWIFT confirmations

- Broker credit statements

- E FIRAs and invoices

- ITR acknowledgments

- Form 26AS showing TCS

Family member LRS tracking

Limits are per person, per PAN. A family of four can remit up to USD one million collectively, but track each person separately to avoid compliance errors. For a compact checklist, see this foreign investments under LRS guide.

Stick to eligible instruments

Do not try to mask crypto or leverage under vague purpose codes. Systems flag prohibited purposes, and misdeclaration can invite blacklisting. A refresher is here, LRS overview and restrictions.

Documentation and compliance cheat sheet

Must have documents

- PAN, updated KYC

- Form A2 and LRS declaration, investment in foreign securities

- Overseas brokerage proof and funding instructions

- Source of funds, bank statements, ITR, salary slips, invoices, e FIRAs

- Beneficiary bank details and your client reference

- Form 15CA and 15CB if your bank or CA asks, rare for plain stock purchases

Compliance checkpoints

- Stay within the USD 250,000 cap across all purposes

- Use the correct purpose code, equity, debt, mutual funds as applicable

- Budget for TCS if total LRS usage crosses ₹10 lakh

- File Schedule FA in your ITR

- Keep records for seven years

For bank side process clarity, scan this LRS FAQ page.

Answering common bank queries during LRS application

What is the purpose of this remittance?

Say, investment in foreign securities, specifically stocks and ETFs listed on NYSE or NASDAQ, avoid words like trading or speculation.

What is your source of funds?

Salary, supported by payslips and Form 16, or freelance income supported by invoices, e FIRAs, ITR. Keep the files ready.

Why are you sending to an omnibus account instead of an account in your name?

I am funding my personal trading account with the broker, the client reference number ensures the funds credit to me. Share the broker’s official funding note, similar to this LRS process explainer.

Have you used LRS earlier this year?

Be precise, mention the month, amount, and purpose, and your remaining headroom.

Do you have ongoing income from abroad?

If yes, confirm it is received under RBI rules, converted to INR, declared in ITR, and supported by e FIRAs. Organized records speed approvals.

Special tips for Indian freelancers using LRS for investments

Source of funds is your strongest card

Maintain every invoice, every e FIRA, and a clear trail, client paid you, money entered India, converted to INR, now you invest.

Use only your personal resident account

LRS is for individuals. Do not initiate from current accounts or company accounts.

Convert inbound foreign income to INR first

Receive USD, hold briefly if your platform permits, convert to INR, then remit under LRS. This keeps your documentation straightforward for the bank.

Cushion for TCS

Irregular income means timing matters. If your cumulative LRS use crosses ₹10 lakh, keep the 20 percent TCS buffer ready to prevent failure.

Tools that simplify inbound and outbound workflows

- Karbon Business, virtual USD, GBP, EUR accounts, INR settlement in one to two days, auto e FIRA, flat one percent fee with zero FX markup on mid market rates, and currency holding up to 60 days.

- Wise Business, transparent fees with multi currency accounts, e FIRA may need manual follow up.

- Payoneer, popular with freelancers, FX markup can be higher and support response varies.

- Razorpay X International, useful for scaling small businesses, focused more on business accounts.

Efficient inbound makes outbound LRS smoother, your bank sees clean e FIRAs, and approvals are faster.

Final takeaway checklist before you remit money for stocks

- Verify year to date LRS usage, ensure you are under USD 250,000.

- Double check documents, PAN, KYC, Form A2, LRS declaration, broker proof, source of funds, and beneficiary details with client reference.

- Confirm beneficiary and client reference, match the broker’s instructions character by character.

- Buffer cash for TCS and fees, if crossing ₹10 lakh, add 20 percent plus bank charges and GST.

- Set up tax tracking, folder for documents, calendar reminder for ITR and Schedule FA, and check Form 26AS for TCS credit.

- Consult your RM or CA for edge cases, a short consultation can save weeks of rework.

- Optimize inbound flows, platforms with auto e FIRA and zero inbound markup leave you with more INR to invest.

Outward remittance for investments under LRS opens global diversification for Indian residents. Follow this step by step, keep paperwork tight, and you will invest abroad as smoothly as you invest at home. For a compact process map, scan this LRS investments guide.

FAQ

How can I receive USD from my client and then invest abroad under LRS without drama?

Receive the client payment through a compliant channel, convert it to INR in your personal resident savings account, and then initiate the LRS remittance with Form A2 and the correct purpose code. If you use a platform like Karbon Business that auto generates e FIRA and settles INR quickly, your source of funds trail is clean, which makes the bank approval faster.

USD 250k limit under LRS is yearly, can I send in multiple tranches or do I need to do one big transfer?

The USD 250,000 cap is per person per financial year, and you can send multiple tranches as long as the aggregate stays within the limit across all purposes. Many investors stagger wires to manage FX risk and to time TCS thresholds, which is often smarter than one large transfer.

Do I need Form 15CA and 15CB for investing in US stocks via LRS or is Form A2 enough?

For straightforward LRS investments in listed securities, banks usually accept Form A2 and the LRS declaration without 15CA or 15CB. That said, each bank has its own risk policy, so confirm with your Authorised Dealer or CA. Keep your source of funds documents ready to avoid delays.

Which bank is best for LRS remittance, HDFC, ICICI, SBI, or an international bank?

Pick based on FX spread, fees, digital experience, and LRS familiarity. Some global banks have seasoned investment remittance teams, while large Indian banks offer faster digital flows. Compare two or three banks on the same day, since FX spreads change, and choose the one that offers a tighter rate and faster processing.

Can I send money from my current account for LRS or only from my personal savings account?

LRS is for resident individuals only, so use your personal savings account linked to your PAN. Do not initiate LRS remittances from current accounts tied to your business, OPC, or LLP. If you freelance, receive funds, convert to INR, and remit from your personal account.

TCS at 20 percent on LRS is too high, will I get it back in my ITR or is it a final loss?

TCS is not a cost, it is an advance tax collected on LRS usage above ₹10 lakh in a financial year. It will reflect in your Form 26AS, and you can claim it as a credit when filing your ITR. If your total tax liability is less, you can get a refund. Budget accordingly so your remittance does not fail for shortfall.

My broker uses an omnibus account, will the bank allow it and how do I make sure money credits to me?

Most major brokers use omnibus accounts, which banks accept as long as you provide the official funding instructions and include your unique client reference or memo. Enter that reference exactly, and keep the SWIFT copy to share with the broker if credit is delayed.

What documents do freelancers need to show source of funds for an LRS investment wire?

Expect to submit the last six months bank statements, ITR acknowledgment, invoices for international clients, and e FIRA documents for inward remittances. If your platform, for example Karbon Business, auto generates e FIRA within 24 hours, it strengthens your case and speeds verification.

How much time does an LRS wire take to reach Interactive Brokers or Charles Schwab, and what if it gets stuck?

After bank approval, wires usually credit within one to three business days. If funds do not appear after three days, request a SWIFT copy from your bank and share it with your broker’s funding desk. Most delays come from typos in beneficiary fields or missing client reference numbers.

Can I use LRS to buy crypto or do margin trades on offshore platforms?

No, banks flag and block crypto and leveraged trading under LRS. Stick to permitted securities like listed stocks, ETFs, bonds, and mutual funds. Misdeclaring the purpose can lead to rejection and impact your future LRS requests.

I am close to the ₹10 lakh TCS threshold, should I split transfers to reduce cash blockage?

You can plan tranches to manage TCS cash flow, but once your cumulative LRS usage crosses ₹10 lakh in the year, TCS applies to the amount beyond that limit. Keep a buffer so fees and TCS do not cause a shortfall, and remember that TCS is claimable at ITR filing.

How do I track LRS usage for my family, and can we combine limits for a larger portfolio?

Each person gets a separate USD 250,000 limit per financial year, tied to their PAN. A family of four can collectively remit up to USD one million if each member initiates from their own personal account and files their own forms. Track each person’s usage separately to avoid compliance issues and to plan taxes and TCS smartly.