Key takeaways

- Indian residents can legally invest abroad under the Liberalised Remittance Scheme, with an aggregate annual limit of USD 250,000 tracked against your PAN.

- Investments like listed stocks, ETFs, mutual funds, and bonds are allowed under Overseas Portfolio Investment, while crypto and unregulated platforms are off limits.

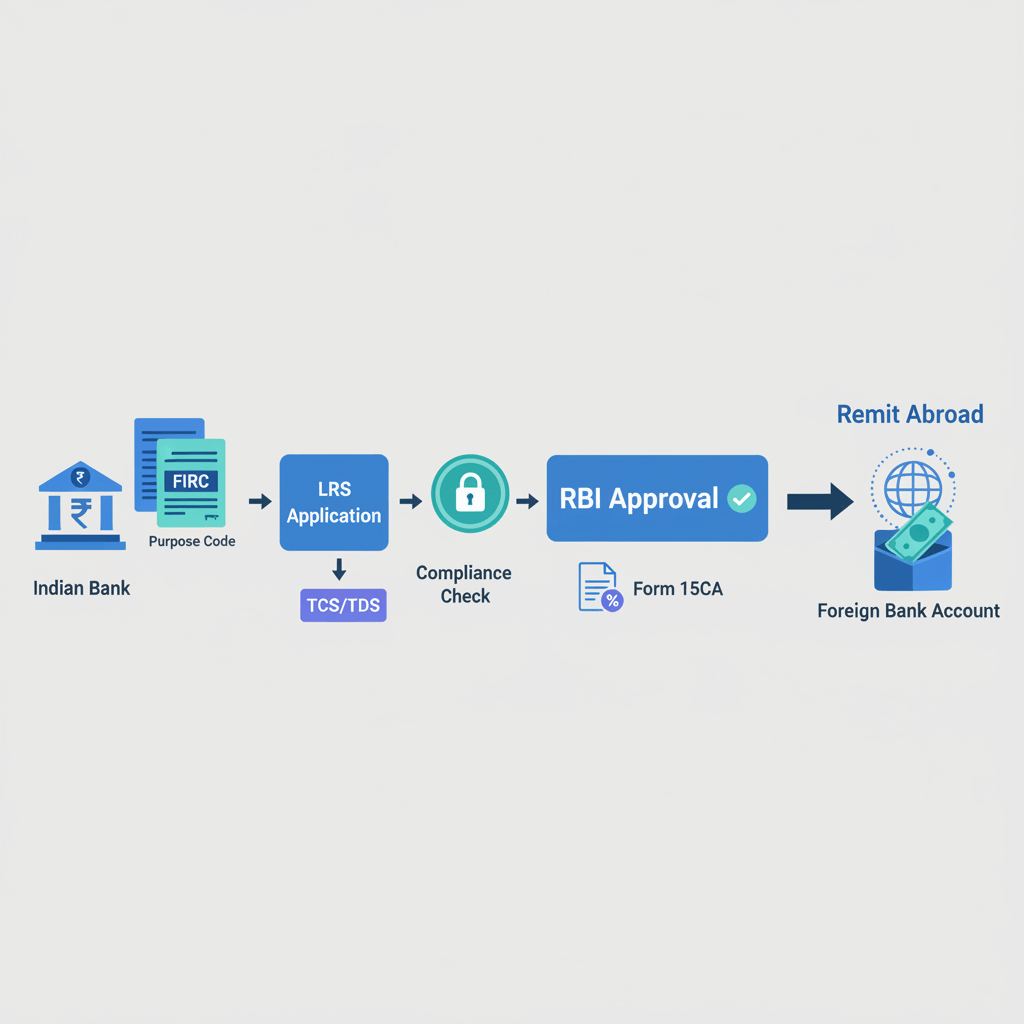

- You must remit through an authorised dealer bank, with correct purpose codes, precise beneficiary details, and a clean documentary trail.

- Total cost includes the bank’s FX spread, remittance fee, SWIFT or intermediary charges, potential broker deposit fees, and Tax Collected at Source above the INR 10 lakh annual threshold for investments.

- Freelancers should first realise export earnings in India, then move funds from their business account to a personal savings account before remitting under LRS.

- Keep proofs like the A2 form, SWIFT copy or UTR, and broker deposit confirmations for tax filings and compliance checks.

- Use a small test transfer, submit within your bank’s forex cut off time, and maintain a running log of your annual LRS usage.

What is LRS and how does it work for investments?

The Liberalised Remittance Scheme lets resident individuals send foreign exchange for permitted transactions without prior RBI approval. Think of it as a ready made allowance for overseas spending, education, investments, gifts, and more, with an annual cap of USD 250,000 per person, every April to March.

For stock market investments, you fall under Overseas Portfolio Investment, or OPI. This category allows you to buy listed securities abroad while keeping your stake and influence below control thresholds.

What can you invest in under LRS? Listed shares, exchange traded funds, foreign mutual funds, overseas bonds, and even fractional shares on regulated platforms are permitted. You can also exercise ESOPs and RSUs granted by foreign employers. Any income you earn dividends, interest, capital gains can be retained or reinvested overseas, there is no immediate repatriation requirement, as clarified in the HSBC LRS FAQs.

What is off limits? Crypto assets and other virtual digital assets are banned under LRS, as are leveraged products unless they are part of regulated brokerage offerings, and transfers to jurisdictions on RBI or FATF restricted lists. See the overview from Vidhi Centre for Legal Policy on the Liberalized Remittance Scheme.

A crucial distinction: OPI implies you hold under 10% and have no management control. Cross that and you enter Overseas Direct Investment territory, which requires separate filings and approvals, a line explained in this Winvesta guide to LRS and foreign investments.

How to remit money for stocks: the complete step by step workflow

Step 1: Pick a compliant overseas broker

Confirm the platform accepts India based individuals, maintains segregated client accounts, uses reputable custodians, and is regulated by a major authority like the SEC or FCA. Review the broker’s funding instructions carefully for beneficiary bank name, SWIFT or BIC, IBAN or account number, and any intermediary bank details. For more context, see this overview of LRS for investments.

Step 2: Calculate your LRS headroom and total costs

Check how much of your USD 250,000 limit you have already used this financial year. Then map the full cost so there are no surprises.

- Foreign exchange spread: banks quote above the mid market rate, commonly 0.5% to 2%.

- Bank charges: outward remittance fees often range from INR 1,000 to INR 5,000 plus GST, as outlined in this outward remittance explainer.

- SWIFT or intermediary fees: USD 10 to USD 30 may be deducted in transit.

- Broker deposit fees: some platforms charge for incoming wires.

- Tax Collected at Source: 20% TCS applies on investment remittances exceeding INR 10 lakh in a financial year, claimable as credit in your return.

Step 3: Gather your documentation

Have these ready, clearly named and easy to upload:

- PAN and Aadhaar or address proof matching your bank KYC.

- Form A2 cum LRS from your bank.

- Bank outward remittance request form, if applicable.

- Broker account confirmation showing your name, account ID, and funding bank details.

- Purpose declaration: “Remittance for Overseas Portfolio Investment under LRS, for listed stocks or ETFs via [Broker Name].”

- Source of funds evidence, such as bank statements or ITRs for larger amounts.

- Form 15CA and 15CB only if your bank requires them for the nature of payment, which is usually not the case for capital remittances.

Pro tip: compress PDFs if needed, and avoid fuzzy scans. Clear, legible documents speed approvals.

Step 4: Initiate the remittance through your bank

Add the beneficiary exactly as per broker instructions, select the correct purpose code for investments under LRS, upload documents, declare source of funds, review rates and fees, then authorise with OTP or second factor. Processing timelines are typically same day approval if submitted within business hours, with credit in one to three working days.

Step 5: Confirm receipt and archive proof

Download the SWIFT copy or UTR from netbanking. Check your broker account for funds within two to three business days, note any intermediary deductions, and file everything together for tax and audit readiness.

Documentation deep dive: checklists and pro tips

- Match beneficiary naming precisely. If the format says “For the benefit of [Broker] Client [Your Name],” use that exact phrase.

- Keep a reusable purpose email template. A crisp note with your broker account ID and attached A2, broker letter, and purpose declaration handles most queries, as seen in this guide to outward remittance.

- Mind file sizes. Many portals cap uploads at 2 MB or 5 MB per file.

- Update bank KYC before you start. Address mismatches trigger manual reviews.

- Know your bank’s forex cut off. Submit before the desk closes, often early afternoon, as noted by DBS.

Sample field entries:

Purpose: Investment under LRS, OPI in listed securities

Beneficiary: As per broker custodian details

Relation: Self

Currency: USD, EUR, GBP as required

Amount: Exact foreign currency figure

Compliance: understanding RBI and FEMA rules inside out

The USD 250,000 annual limit is aggregate. That includes travel, education, gifts, and investments. Track your usage across all banks. For a practical explainer, see this LRS limits guide and the overview on ClearTax.

Stay within OPI boundaries. Keep holdings below 10% with no control rights. For background on OPI versus ODI, refer to this primer.

TCS on investment remittances. Budget 2025 puts the threshold at INR 10 lakh annually, with 20% on the excess, claimable as credit. See this LRS investments explainer.

Tax on outcomes and foreign tax credit. Overseas dividends and gains are taxable in India, and you can claim foreign tax credit via Form 67. See the HSBC FAQs on LRS and taxes.

Red flags that cause rejections: business or current account funding, crypto or unregulated destinations, mismatched beneficiary names, vague purpose codes, unclear sources of funds, or attempts to split remittances to dodge limits or TCS, as highlighted in this comprehensive LRS guide.

Costs, timelines, and cashflow planning

Understand every cost layer before you click “Submit.”

| Component | Details | Typical range |

|---|---|---|

| FX spread | Bank rate above mid market | 0.5% to 2% |

| Bank remittance fee | Flat fee plus GST | INR 1,000 to 5,000 |

| SWIFT and intermediary | Deducted en route | USD 10 to 50 |

| Broker deposit fee | Incoming wire charge | USD 0 to 25 |

| TCS | On amount above INR 10 lakh | 20% creditable |

Example: Invest USD 5,000. With an INR 84.50 bank rate versus 84.00 mid, spread is roughly INR 2,100, bank fee about INR 2,000 plus GST, SWIFT USD 20. Expect a total debit around INR 4.26 lakh. When cumulative investment remittances cross INR 10 lakh in the year, TCS of 20% applies on the excess, as described in this outward remittance explainer.

Timelines: approvals can be same day to two working days, credits usually T+1 to T+3. Avoid late Friday submissions to reduce weekend drift.

Pro tip: do a USD 500 test run to validate routing and landed costs, then scale up.

For freelancers: linking your export earnings to LRS investments

Step one: realise your export income in India within prescribed timelines, keep inward remittance proofs like e FIRA handy, and reconcile your client receipts. See this primer on the Liberalised Remittance Scheme for context.

Step two: transfer from business current account to your personal savings account. LRS remittances must go from a resident individual’s personal account.

Step three: follow the standard LRS workflow with a clear source of funds trail, including inward remittance proof, inter account transfer statement, and outward SWIFT copy. This keeps you compliant and audit ready.

Why this loop? FEMA requires realisation in India before deploying overseas. Once realised, you can remit under your annual LRS cap with timing flexibility on FX and markets.

Common pitfalls and how to fix them

- Vague purpose leads to rejection: resubmit with a precise OPI purpose note and broker account letter, as advised in this LRS investment guide.

- Intermediary charges eat into credit: ask your bank about shared or “OUR” charges, or remit a bit extra, and confirm the broker’s preferred routing, per this explainer.

- Unexpected TCS: check Form 26AS to track cumulative LRS and TCS, then plan cashflow accordingly, as outlined by ClearTax.

- Name mismatch bounce: mirror the broker’s “For Further Credit to [Your Full Legal Name]” format exactly.

- Bank asks for 15CA or 15CB: clarify nature of payment as capital transfer. If insisted, obtain 15CB from your CA, a position explained by DBS.

- Year boundary confusion: remember LRS resets each April 1. Escalate with last year’s A2 forms if the bank system misattributes usage.

Quick reference checklists

Pre remittance

- Broker accepts Indian residents and shared funding instructions

- Verified LRS headroom for the current financial year

- Estimated total cost: FX, bank fee, SWIFT, broker fee, TCS

- Collected PAN, address proof, A2, broker letter, purpose note, bank statements

- All names and account details match exactly

At remittance

- Beneficiary added with correct SWIFT, IBAN or account number

- Correct purpose code for investment under LRS

- Uploaded A2, broker confirmation, and supporting docs

- Declared source of funds clearly

- Reviewed FX, fees, total debit, and TCS if applicable

- Captured confirmation screenshot and authorised with OTP

Post remittance

- Downloaded SWIFT copy or UTR

- Checked broker credit T+1 to T+3

- Noted intermediary deductions for next time

- Filed SWIFT, broker deposit mail, and A2 form together

- Updated your personal LRS usage tracker

Sample email to your bank’s forex desk

Subject: LRS Investment Remittance Request – PAN [Your PAN]

Dear Forex Team,

I request an outward remittance of INR [Amount] to fund my overseas portfolio investment account under the Liberalised Remittance Scheme.

Details:

Purpose: Overseas Portfolio Investment, listed stocks and ETFs

Beneficiary Bank: [Broker’s Bank Name]

SWIFT: [Code]

IBAN or Account: [Number]

Beneficiary Name: [As per broker funding instructions]

My Account with Broker: [Account ID]

Broker: [Platform Name]Attachments:

1. Signed A2 cum LRS

2. Broker account confirmation letter

3. Purpose declaration

4. Recent bank statementPlease confirm receipt and expected processing timeline. Let me know if anything else is required.

Thank you,

[Your Name]

[Mobile]

[Email]

Where does Karbon Business fit into the LRS picture?

Karbon Business helps Indian freelancers receive international payments quickly and compliantly, with local rails like ACH or SEPA, auto generated e FIRA, mid market FX, and fast INR settlement. Learn more at Karbon Business.

However, Karbon handles inward remittances. For outward investment under LRS, you must remit from your personal savings account via your authorised dealer bank, following the workflow in this guide.

- Earn overseas via Karbon, receive documentation like e FIRA.

- Move realised funds to your personal savings account.

- Remit under LRS to your foreign broker, up to USD 250,000 a year.

- Invest, track, and report income while continuing to receive client payments efficiently.

Final compliance note and disclaimer

Rules evolve. Limits, purpose codes, TCS thresholds, and documents can change mid year. Verify current norms on the RBI and Income Tax portals, align with your bank’s forex desk requirements, and consult a CA for complex or high value cases. For foundational context, read this overview of the Liberalised Remittance Scheme.

This article is educational, not financial, legal, or tax advice. Your situation may differ, and compliance responsibility rests with you.

Wrapping up: your roadmap to investing abroad legally and confidently

Outward remittance for investments under LRS gives you access to global markets, diversification, and currency exposure. Choose a regulated broker, prepare clean documents, coordinate with your bank’s forex desk, respect the USD 250,000 cap, and keep immaculate records. The process becomes a repeatable playbook after your first successful transfer.

Whether you are a coder in Bengaluru buying US index funds, a designer in Mumbai adding gilts, or a consultant in Pune allocating to European equities, LRS is your legal framework. Follow the steps, stay compliant, and let your portfolio grow as steadily as your skills.

FAQ

How can I, as an Indian freelancer, legally send money to my foreign broker for stocks under LRS?

Use your personal savings account with an authorised dealer bank to initiate an outward remittance under the Liberalised Remittance Scheme, select the correct purpose code for investments, attach A2, broker confirmation, and a purpose declaration, then authorise the transfer. If you receive client payments via platforms like Karbon Business, first realise funds in India, transfer to your personal savings account, and then remit under LRS.

What documents will my bank typically ask for when I wire funds to a US broker?

Expect PAN, address proof, A2 cum LRS, outward remittance request form if required, broker account confirmation with funding details, a purpose declaration referencing OPI in listed securities, and source of funds evidence. Some banks may ask for 15CA or 15CB depending on their policy, even though capital remittances usually do not need them.

Will TCS of 20% always apply when I remit for investments under LRS?

No, TCS applies only when your cumulative investment remittances under LRS in a financial year cross INR 10 lakh. The bank deducts 20% on the excess. You can claim it as credit in your income tax return via Form 26AS. Plan cashflow so the TCS deduction does not surprise you mid year.

Can I fund my foreign broker directly from my current account where I receive freelance income?

No. LRS is only for resident individuals, and remittances must go from your personal savings account. If you receive international payments in a current account or via Karbon Business, transfer the realised INR to your savings account, keep the trail clean with statements and e FIRA, then remit under LRS.

Is crypto or margin trading allowed if I send funds under LRS for investments?

Crypto assets and unregulated margin products are prohibited under LRS. Stick to permitted OPI instruments like listed equities, ETFs, foreign mutual funds, and bonds via regulated brokers. If in doubt, confirm the product’s eligibility with your bank and the broker.

How do I choose a compliant international broker that accepts Indian residents?

Check for top tier regulation, segregated client funds, reputable custody, clear funding instructions, and investor protection schemes. Verify that the beneficiary details allow wires from India based clients, and avoid platforms without transparent fees. Do a small test transfer before scaling.

What is the practical timeline from initiating a wire to seeing dollars in my brokerage account?

Same day to two working days for bank approval if documents are clean, and typically one to three business days for credit at the broker, depending on routing and time zones. Avoid initiating late on Fridays, and submit before your bank’s forex desk cut off for faster processing.

Do I need to bring back dividends or sale proceeds from my US stocks to India?

No, LRS permits retaining and reinvesting such income overseas. You must, however, report dividends and capital gains in your Indian tax return, and you can claim foreign tax credit by filing Form 67 with the broker’s tax statement as evidence.

I get paid in USD by clients through Karbon, can I keep the dollars abroad and invest directly?

Under FEMA, export proceeds must be realised in India within prescribed timelines. Receive the funds, get documentation like e FIRA from Karbon Business or your bank, move INR to your personal savings account, and then remit under LRS to your foreign broker. This preserves compliance and auditability.

What purpose code should I select inside netbanking for LRS stock investments?

Banks map purposes to internal codes, commonly a variant of “Investment under LRS” or a securities code like S0001. If the dropdown is unclear, contact your bank’s forex desk and confirm the exact code for Overseas Portfolio Investment to avoid rejection.

Do I have to file 15CA and 15CB when sending money for OPI under LRS?

Generally, no, because you are transferring capital to your own account abroad, not paying a foreign vendor for taxable services. Some banks may still request these forms as policy, so check in advance and have your CA issue 15CB if the bank insists.

How should I budget total costs, including hidden charges, for an outward remittance?

Add the bank’s FX spread, remittance fee plus GST, likely SWIFT or intermediary deductions, any broker incoming wire fee, and potential TCS above the INR 10 lakh threshold. Keep a simple spreadsheet to compare landed cost per dollar, and consider a small pilot transfer to validate the route before larger remittances.