Key takeaways

- Amazon typically settles every 14 days, but reserves, verification, and holidays can extend timelines, so plan cash flow with buffers.

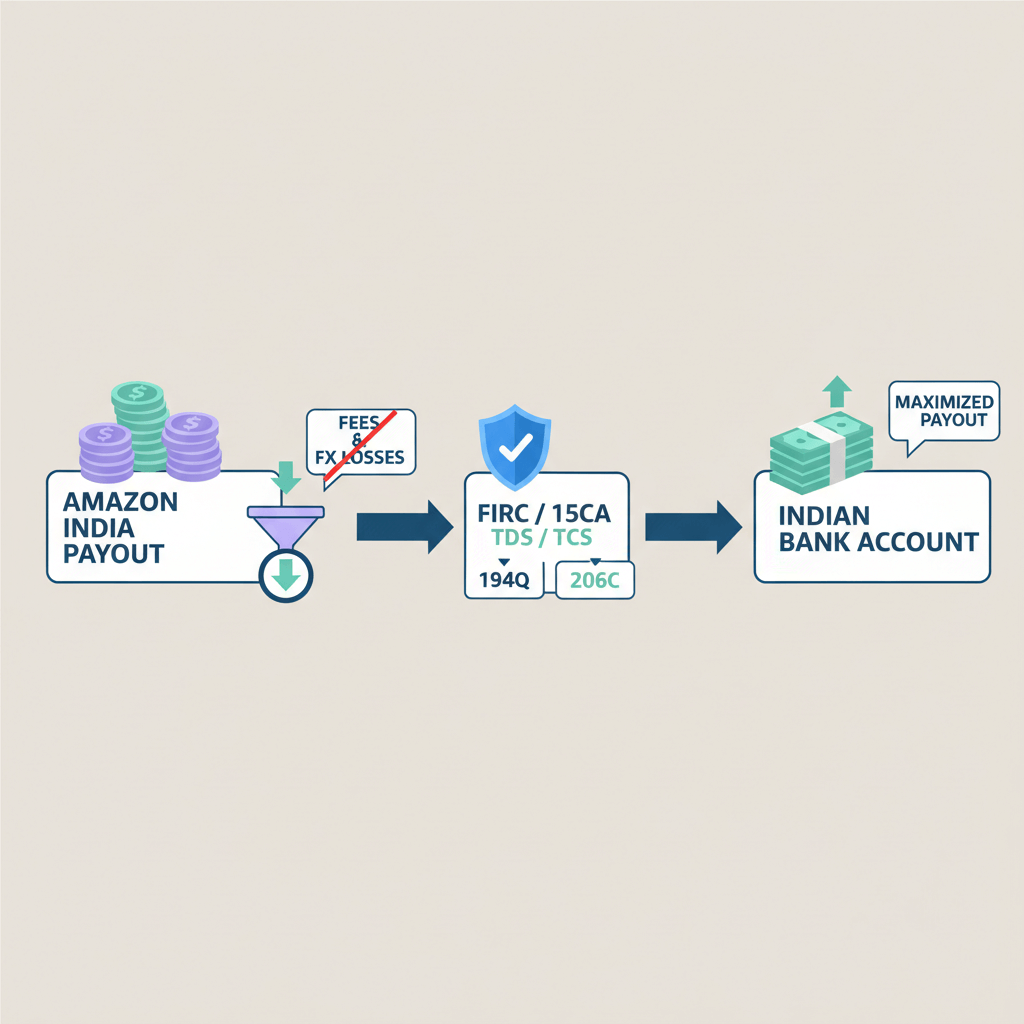

- Your landed INR depends on platform fees, payout route costs, bank charges, and FX markup, not just the USD gross you see in Seller Central.

- ACCS is simple but usually costs ~1.5% fee plus 1 to 2% FX markup, PSPs vary by volume, direct USD wires add fixed fees but can win on FX with batching.

- Always compute your “effective INR per USD” and compare with mid market to catch hidden spread; use an effective rate calculator India to standardize checks.

- Batch settlements, negotiate bank charges, and avoid double conversions, these small wins compound into thousands saved yearly.

- Maintain compliance: IEC, AD code, shipping bills, e-BRC for goods, e-FIRC/FIRA for services, and keep settlement reports matched to bank credits.

- Run a $100 test payout before scaling, reconcile reported versus landed, and escalate any name mismatch or intermediary fee surprises quickly.

How Amazon Global Selling settlement works, end-to-end

Your first US sale is live, great, now the key question is how those USD earnings turn into INR, what nibbles away at them, and how long it really takes. Amazon disburses every 14 days, but it can hold reserves for performance metrics, returns, chargebacks, holidays, or pending verification. For new or recently flagged accounts, expect longer than two weeks.

Track everything inside Seller Central, Payments, and Settlement reports. These show gross USD before any payout routing, the real numerator for your effective rate calculation. The flow is straightforward: Amazon disburses USD to your chosen method, then conversion and INR credit happens. Timelines vary by route, as detailed in this practical comparison, see Payoneer vs bank transfer fees for Indian Amazon sellers. Payoneer often lands INR in 2 to 4 days after disbursement, SWIFT bank transfers can take 3 to 7 days depending on intermediary banks and cutoffs.

This variability matters, especially if you are restocking or paying suppliers. A four day delay versus seven can mean missing a reorder window or paying late fees. Build a buffer and monitor reserves closely.

All the fees that affect your final INR

Amazon platform fees, referral, FBA fulfillment, and closing fees, are deducted before payout routing. They reduce the gross but are not the lever for optimizing your INR credit.

Payout specific fees

- ACCS: A volume based fee, for example 1.50% under $1 million in annual proceeds, plus 1 to 2% FX markup over market rate, see the Amazon seller fees guide.

- Third party PSPs: Providers like Payoneer, PingPong typically charge 1 to 2% through FX markup or a transaction fee, details shift by volume and negotiation, see Payoneer fees in India.

- Indian bank charges: $25 to $40 SWIFT fee, $10 to $15 intermediary bank charges, inward remittance charges, plus GST on fees. Multiple small payouts amplify these costs.

Forex conversion costs

The spread is the quiet killer. If the mid market is $1 = ₹86.5, a 1 to 2% markup means you might effectively get ₹85. “Zero transfer fee” marketing often hides this in the rate. The rate is locked when your disbursement is executed, not when INR hits the bank.

If you are not measuring effective INR per USD landed versus mid market, you are likely giving up 1 to 3% without noticing.

Payout routes to India compared

Route A: ACCS to INR bank

Pros: Easiest setup, predictable credit, 1 to 5 business days, no wire handling.

Cons: 1.50% fee plus 1 to 2% FX markup, limited control on timing.

Typical costs: About 1.50% fee plus spread, roughly $3,000 on $200,000 gross.

Route B: Approved PSPs, Payoneer and PingPong

Pros: Marketplace approved, multicurrency balances, competitive FX, e-FIRC automation.

Cons: 1 to 2% all in, withdrawal limits, compliance checks, 2 to 4 day INR credits.

Typical costs: 1 to 2% total, about $2,000 on $200,000 if negotiated well.

Route C: USD, GBP, EUR to your bank, convert later

Pros: Full control on timing and spread, potential near zero markup with the right converter.

Cons: Requires an approved account in your legal name, fixed wire fees, rejection risk if unapproved.

Typical costs: $30 to $55 per wire plus your bank’s FX spread, best when you batch larger amounts.

Amazon requires the payout account or PSP to be in the seller’s name and on the approved list. Avoid unapproved virtual accounts to prevent holds, rejections, or delays, see the operational nuances in Payoneer vs bank transfer fees for Indian Amazon sellers.

Reading your settlement and finding the real cost

Download the Settlement report, then compute your “effective INR per USD”: landed INR divided by gross USD. Compare with mid market to quantify erosion. A handy worksheet is this effective rate calculator India.

Example: $10,000 gross, $9,850 after Amazon fees, and ₹793,425 landed means an effective ₹80.55 per USD. If mid market is ₹82, you lost ₹1.45 per dollar, about 1.8% all in. Over a year, that adds up.

Worked examples, simple math

- ACCS: $10,000 minus 1.5% fee = $9,850, assume 1.5% FX markup, you net about ₹793,425, roughly a 2% total loss from mid market.

- Payoneer: $10,000 minus 2% = $9,800, if markup is minimal and you clear near mid market, you land about ₹803,600.

- Direct USD wire, convert later: $10,000 minus $45 total wire costs = $9,955, convert near mid market to land about ₹816,410, strongest if you batch and time conversions.

Takeaway: PSPs often beat ACCS by a meaningful margin, while direct USD routes can win at scale when you batch wires and negotiate bank spreads.

How to set up and test your payout method

- In Seller Central, open Settings, Account Info, Deposit method, add your bank or PSP from the approved list.

- Complete verification, KYC and micro deposit confirmation within three days.

- Set frequency, monitor reserves, new accounts often see 7 to 14 day holds on a portion of payouts.

- Request a small test payout, for example $100, then reconcile report versus bank credit to identify intermediary fees or rate surprises, a flow also covered in Payoneer vs bank transfer fees for Indian Amazon sellers.

Do not discover a $50 per wire surprise on your first $10,000 settlement, test and negotiate first.

Managing forex conversion risk

- Hold multicurrency and batch convert: Many PSPs allow this, convert when the rate is in your favor.

- Rate alerts: Set target levels and execute conversions as the rupee moves.

- Forward cover: At scale, ask your bank for forwards to lock rates for a fee.

- Price buffer: Pad listings by 2 to 3% to absorb INR moves during the 14+ day settlement cycle.

Holding foreign currency has time limits and compliance implications, typically up to 60 days. Factor FEMA and bank policy into your playbook.

Compliance and documentation for Indian exporters

For goods: IEC, AD code, shipping bills, and e-BRC from your bank that matches realized forex. For services: FIRA or e-FIRC, PSPs like Payoneer often auto generate e-FIRC. Maintain a full trail, settlement reports plus bank advice plus e-BRC or FIRA. Mismatches, even 5%, can trigger GST or customs queries.

Cost optimization checklist, quick wins

- Compare ACCS versus PSP at your volume, start with the Amazon seller fees guide benchmarks.

- Negotiate inward remittance charges and SWIFT fees, many banks waive for consistent volume.

- Avoid double conversions, each hop adds spread.

- Batch payouts, one $10,000 wire is cheaper than five $2,000 wires.

- Track effective rate monthly, switch if spread exceeds 2%.

- Keep account health green to reduce reserves and speed cash flow.

Troubleshooting common payout issues

- Delays: Usually reserves or verification. Check the Payments dashboard, resolve KYC prompts.

- Partial credits: Intermediary bank fees, reconcile line by line and raise a ticket with exact figures.

- Name mismatches: Ensure the legal name on bank or PSP exactly matches Seller Central, even “Pvt” versus “Private” can cause rejections and retries.

- Poor FX rates: Compare your effective INR per USD to mid market from a reputable source and escalate with evidence.

When stuck, pull the Settlement report, check payout history, compare with the bank statement, then escalate with specifics. Many issues resolve in a single support thread when you provide precise numbers and timestamps, a pattern highlighted in Payoneer vs bank transfer fees for Indian Amazon sellers.

A note for service exporters and freelancers

If you bill clients directly, you are not bound by Amazon’s approved payout list. Platforms built for Indian freelancers offer simpler accounts, multicurrency holding, and fast INR credits. For example, Karbon Business provides virtual USD, GBP, EUR, and CAD accounts with local transfers, 0% forex markup at mid market, a flat 1% platform fee, INR settlement in 24 to 48 hours after you claim, auto e-FIRA in 24 hours, and up to 60 days of currency holding. Other options include Wise Business, Payoneer, PayPal, RazorpayX International, and Tazapay. Pick based on your invoice sizes and how often you convert.

Final thoughts

Compute your true Amazon international seller payout to India by starting with gross USD, then subtract platform fees, payout route fees, bank charges, and FX markup to the landed INR. Review routes quarterly and switch when the math justifies it. At $500,000 annual volume, squeezing out even 1% is ₹4 to ₹5 lakhs saved, which funds inventory, ads, or simply fatter margins. The process is simple, download reports, measure, test a small payout, negotiate, then scale what works, a mindset echoed in the Amazon seller fees guide.

FAQ

How do I receive Amazon USD payouts in India with the least fees if I am doing low monthly volume like $5,000 to $10,000?

For low volume, ACCS is the simplest, but a negotiated PSP often beats it on FX. Run a $100 test through both, compute effective INR per USD, and include any PSP withdrawal charges. If the spread difference exceeds 0.5%, switch.

Is Payoneer better than direct bank wire for Indian Amazon sellers when my settlements are small and frequent?

Usually yes, because fixed SWIFT fees hurt small wires. If you receive many sub $2,000 payouts, PSPs tend to be cheaper. If you can batch into fewer larger settlements, direct USD wire plus a low markup conversion can win.

How can I check if my bank or PSP is taking hidden FX markup without telling me?

Divide landed INR by the gross USD from the settlement report to get your effective rate, then compare with mid market for that day and time. If you see 1 to 2% gap consistently, that is the markup. Keep a simple sheet and track monthly.

Can I hold USD and convert when the rupee weakens, is that allowed?

Yes, via multicurrency PSP balances or foreign currency accounts, but there are holding period limits, often up to 60 days, and documentation requirements. Use holding strategically, batch conversions, and maintain e-FIRC or e-BRC trails.

For freelancers, which platform gives the best USD to INR rate and fast settlement, is Karbon Business worth it?

Freelancers often prioritize mid market or near zero markup and fast INR credit. Karbon Business offers mid market rates with a flat 1% fee and 24 to 48 hour settlement after claim, plus auto e-FIRA. Compare your typical invoice amount and see if the flat platform fee beats percentage based providers.

My Amazon payout shows “partial credit” in my Indian bank, how do I find where the money went?

Cross check the settlement report amount with your bank credit. The difference is usually intermediary bank fees or inward charges. Ask your bank for the SWIFT MT103 copy, it lists intermediaries and deductions. Then raise a support ticket with specifics.

What is a good benchmark for total payout cost, how much is too much for Indian sellers?

As a rule of thumb, aim for 1.5% to 2% all in on route fees and FX spread for moderate volumes. If your measured effective rate implies 2.5% or higher erosion, renegotiate, switch PSPs, or batch wires to push costs down.

Which is safer for compliance, PSP payout or direct bank wire to India?

Both are compliant if the account is in your legal name and on Amazon’s approved list for marketplace payouts. For goods exports, ensure e-BRC from your bank matches realized forex, for services, secure FIRA or e-FIRC. PSPs that auto generate e-FIRC simplify audits.

How do Indian freelancers avoid double conversion when clients pay in EUR or GBP?

Collect in the client’s currency into a multicurrency account, then convert once to INR at the best available rate. Avoid routing EUR to USD to INR, each hop costs spread. Platforms like Karbon Business or Wise Business help here.

What should I negotiate with my Indian bank if I am switching to direct USD wires?

Ask for reduced or waived inward remittance charges, lower SWIFT fees, and a tighter FX spread if you convert with them. Provide expected volumes and agree on thresholds for better pricing. Batch wires to maximize leverage.

Why does my effective INR per USD differ from what Google shows for USDINR?

Google shows the mid market, not the retail rate you get. Providers add a markup inside the rate and may charge transfer fees. Your effective INR per USD accounts for both, which is why it is the only number that matters.

As a freelancer, can I invoice US clients in USD and receive INR in 24 to 48 hours reliably?

Yes, with platforms designed for Indian service exporters. For instance, Karbon Business lets you invoice in USD, receive to a local USD account, then claim and settle to INR in 24 to 48 hours with auto e-FIRA for compliance. Always test with a small invoice and confirm the landed rate and timing before scaling.