Karbon Virtual Accounts for International Payment

Collect in 30+ currencies and settle fast to your main account.

Indian businesses handle hundreds of payments every month, and that number keeps rising as they sell to more customers at home and abroad.

When invoices or references are missing, teams spend hours matching payments to the right customer or order. One slip delays delivery and ties up working capital.

Virtual account numbers solve this by giving each customer or invoice its own unique payment ID. Domestic or global, they help you track every payment clearly, match it instantly, and get paid on time.

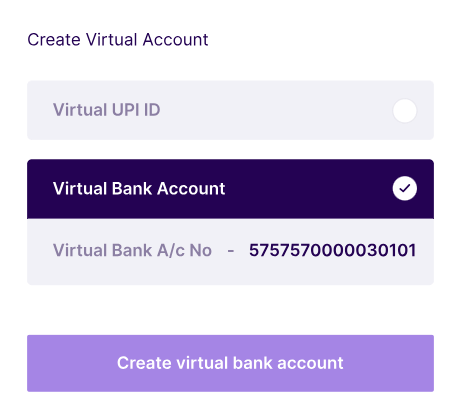

A virtual account number is a unique ID linked to one customer, invoice, or transaction. It’s not a separate bank account. Instead, it’s connected to your main business bank account. The money does not stay in the virtual account. It flows straight to your main account.

Take Mira, who runs a design agency with clients in India, the US, and Europe. She sends over 200 invoices each month. Without virtual accounts, all clients pay to the same bank account.

This creates three problems:

When Mira switches to virtual accounts, each client or invoice gets a unique account number.

All payments still land in Mira’s main account. But each payment carries a clear “tag,” so her team does not match records manually.

When a business works with a bank or payment partner, they get a virtual account system. This system can create thousands of unique account numbers at once.

Companies use an online dashboard or API to generate these numbers. Each one is linked to a customer, invoice, or order.

How it works:

When the money arrives, the bank’s system checks the unique number. It matches the payment to the right customer or invoice.

This removes the need for manual tracking and payment proofs. The finance team sees clear records and updates in real time.

.png)

No. Virtual account numbers work for both domestic and international transactions. Businesses receiving money from other countries can open virtual accounts in different currencies through a bank or payment partner.

This lets them collect payments from clients abroad just like a local business would. For the sender, it feels like a local transfer because the virtual account is in their own currency.

For example:

An IT consulting firm in India works with clients in the UK and Australia. Many clients prefer paying by local bank transfer instead of expensive SWIFT wires.

The firm sets up virtual accounts in GBP and AUD through a payment partner. UK clients pay into the GBP account, and Australian clients pay into the AUD account. These payments settle back to the firm’s INR business account automatically.

When a business works with a payment partner or bank, they can open virtual accounts in different currencies.

How it works:

Once the client pays into the virtual account, the payment partner receives the funds and confirms that the payment is complete.

The partner converts it to the business’s local currency at agreed exchange rates. Karbon handles this conversion.

Traditional SWIFT payments pass through multiple banks, adding intermediary bank fees and delays. These extra charges add up fast for businesses doing frequent cross-border payments.

Virtual accounts work through local clearing routes instead of SWIFT. This reduces cost per transaction, cuts settlement time, and lowers the chance of failed payments.

Domestic businesses that collect payments from multiple payers can benefit the most from virtual accounts. For example:

Domestic virtual accounts reduce payment errors and remove the need for manual tracking when thousands pay the same main account.

Businesses that receive payments from clients can use multicurrency virtual accounts.

International virtual accounts save money on high bank fees, provide better exchange rates, and help businesses get paid on time.

Yes. For domestic payments, they only tag and track payments — the money always goes straight to your main account, so there’s no risk of funds being stuck. For international payments, virtual accounts reduce fraud risk by letting clients pay through trusted local rails instead of costly and error-prone SWIFT wires. Everything stays traceable and easy to reconcile.

No. For both domestic and international use, a virtual account can’t exist alone. It acts like a smart reference layer that routes payments to your primary business bank account. Funds never sit in the virtual account itself. To use one, you must have a valid, active bank account where all incoming payments finally land, whether they come through local or global virtual accounts.

Yes. For domestic payments in India, virtual accounts work perfectly with UPI, NEFT, RTGS, and IMPS. Customers pay like they always do — the only change is they use a unique virtual account number. For international payments, the same idea applies but through local clearing systems like SEPA in Europe, ACH in the US, or local rails in the UK and Australia, making it feel like a local transfer for your client.

For domestic payments, businesses can create thousands of virtual account numbers instantly once they’re onboarded with a bank or payment partner. For international payments, setup is also fast and fully online. Partners like Karbon provide ready access to virtual accounts in over 30 currencies, so you can share local account details with global clients without waiting weeks for traditional bank arrangements.

Domestically, virtual accounts use INR only. They help match incoming local payments to the right customer or invoice. Internationally, you can get virtual accounts in major global currencies like USD, GBP, EUR, AUD, CAD, and more, depending on your provider. With Karbon, you can access 30+ currency options, so you get paid like a local vendor, wherever your clients are based.

Domestically, most banks include virtual accounts as part of their payment solutions with minimal or no extra fees. Internationally, Karbon charges a flat 1% fee on settlements, which covers the local collection, currency conversion, and payout to your main bank account. Compared to SWIFT transfers, which often cost 2–5% with hidden charges, virtual accounts can save you a lot on each overseas payment.

No. Domestically, customers just use their usual UPI app or bank to pay the unique virtual account number. Internationally, your client pays by local transfer using their regular bank or local clearing system. They don’t need to fill SWIFT forms or pay high wire fees. For them, it feels like paying any local supplier, which makes you easier to work with.

Not at all. Domestically, even small schools, coaching centers, utilities, or subscription apps use virtual accounts to track large volumes of incoming payments without errors. Internationally, freelancers, consultants, exporters, and small agencies benefit too — they can share local currency account details with overseas clients, get paid faster, and avoid high SWIFT charges. Any business that wants better payment control should consider them.

Indian businesses handle hundreds of payments every month, and that number keeps rising as they sell to more customers at home and abroad.

When invoices or references are missing, teams spend hours matching payments to the right customer or order. One slip delays delivery and ties up working capital.

Virtual account numbers solve this by giving each customer or invoice its own unique payment ID. Domestic or global, they help you track every payment clearly, match it instantly, and get paid on time.

A virtual account number is a unique ID linked to one customer, invoice, or transaction. It’s not a separate bank account. Instead, it’s connected to your main business bank account. The money does not stay in the virtual account. It flows straight to your main account.

Take Mira, who runs a design agency with clients in India, the US, and Europe. She sends over 200 invoices each month. Without virtual accounts, all clients pay to the same bank account.

This creates three problems:

When Mira switches to virtual accounts, each client or invoice gets a unique account number.

All payments still land in Mira’s main account. But each payment carries a clear “tag,” so her team does not match records manually.

When a business works with a bank or payment partner, they get a virtual account system. This system can create thousands of unique account numbers at once.

Companies use an online dashboard or API to generate these numbers. Each one is linked to a customer, invoice, or order.

How it works:

When the money arrives, the bank’s system checks the unique number. It matches the payment to the right customer or invoice.

This removes the need for manual tracking and payment proofs. The finance team sees clear records and updates in real time.

No. Virtual account numbers work for both domestic and international transactions. Businesses receiving money from other countries can open virtual accounts in different currencies through a bank or payment partner.

This lets them collect payments from clients abroad just like a local business would. For the sender, it feels like a local transfer because the virtual account is in their own currency.

For example:

An IT consulting firm in India works with clients in the UK and Australia. Many clients prefer paying by local bank transfer instead of expensive SWIFT wires.

The firm sets up virtual accounts in GBP and AUD through a payment partner. UK clients pay into the GBP account, and Australian clients pay into the AUD account. These payments settle back to the firm’s INR business account automatically.

When a business works with a payment partner or bank, they can open virtual accounts in different currencies.

How it works:

Once the client pays into the virtual account, the payment partner receives the funds and confirms that the payment is complete.

The partner converts it to the business’s local currency at agreed exchange rates. Karbon handles this conversion.

Traditional SWIFT payments pass through multiple banks, adding intermediary bank fees and delays. These extra charges add up fast for businesses doing frequent cross-border payments.

Virtual accounts work through local clearing routes instead of SWIFT. This reduces cost per transaction, cuts settlement time, and lowers the chance of failed payments.

Domestic businesses that collect payments from multiple payers can benefit the most from virtual accounts. For example:

Domestic virtual accounts reduce payment errors and remove the need for manual tracking when thousands pay the same main account.

Businesses that receive payments from clients can use multicurrency virtual accounts.

International virtual accounts save money on high bank fees, provide better exchange rates, and help businesses get paid on time.

Yes. For domestic payments, they only tag and track payments — the money always goes straight to your main account, so there’s no risk of funds being stuck. For international payments, virtual accounts reduce fraud risk by letting clients pay through trusted local rails instead of costly and error-prone SWIFT wires. Everything stays traceable and easy to reconcile.

No. For both domestic and international use, a virtual account can’t exist alone. It acts like a smart reference layer that routes payments to your primary business bank account. Funds never sit in the virtual account itself. To use one, you must have a valid, active bank account where all incoming payments finally land, whether they come through local or global virtual accounts.

Yes. For domestic payments in India, virtual accounts work perfectly with UPI, NEFT, RTGS, and IMPS. Customers pay like they always do — the only change is they use a unique virtual account number. For international payments, the same idea applies but through local clearing systems like SEPA in Europe, ACH in the US, or local rails in the UK and Australia, making it feel like a local transfer for your client.

For domestic payments, businesses can create thousands of virtual account numbers instantly once they’re onboarded with a bank or payment partner. For international payments, setup is also fast and fully online. Partners like Karbon provide ready access to virtual accounts in over 30 currencies, so you can share local account details with global clients without waiting weeks for traditional bank arrangements.

Domestically, virtual accounts use INR only. They help match incoming local payments to the right customer or invoice. Internationally, you can get virtual accounts in major global currencies like USD, GBP, EUR, AUD, CAD, and more, depending on your provider. With Karbon, you can access 30+ currency options, so you get paid like a local vendor, wherever your clients are based.

Domestically, most banks include virtual accounts as part of their payment solutions with minimal or no extra fees. Internationally, Karbon charges a flat 1% fee on settlements, which covers the local collection, currency conversion, and payout to your main bank account. Compared to SWIFT transfers, which often cost 2–5% with hidden charges, virtual accounts can save you a lot on each overseas payment.

No. Domestically, customers just use their usual UPI app or bank to pay the unique virtual account number. Internationally, your client pays by local transfer using their regular bank or local clearing system. They don’t need to fill SWIFT forms or pay high wire fees. For them, it feels like paying any local supplier, which makes you easier to work with.

Not at all. Domestically, even small schools, coaching centers, utilities, or subscription apps use virtual accounts to track large volumes of incoming payments without errors. Internationally, freelancers, consultants, exporters, and small agencies benefit too — they can share local currency account details with overseas clients, get paid faster, and avoid high SWIFT charges. Any business that wants better payment control should consider them.

W-8BEN for Indian Freelancers: Upwork Guide to 0% Withholding

Swati Saraf

February 17, 2026

W-8BEN for Indian Freelancers: Upwork Guide to 0% Withholding

Swati Saraf

Join 2,000+ freelancers and SMEs already saving on international payments with Karbon.

Save 50% - Start Now