Key takeaways

- Outward remittance is the RBI regulated process to send money from India to overseas vendors, you must submit Form A2, select the correct purpose code, and attach proper documentation.

- Card payments are fine for small subscriptions, bank SWIFT is ideal for invoices and larger amounts, specialist fintech platforms can speed things up and reduce costs.

- Choose OUR charge option so your vendor receives the full amount, SHA or BEN often results in short crediting and reconciliation headaches.

- Refer to this primer for concepts and flow in outward remittance explained, and understand personal limits via foreign remittance limits.

- Match your transaction to the RBI’s categories using the purpose code list for outward remittance, and file taxes correctly with the 15CA and 15CB filing guide.

- Plan for total cost including bank fees, correspondent charges, GST on forex services, and exchange rate spread, see a full breakdown in this complete outward remittance guide.

- For bigger context on compliance and record keeping, explore this outward remittance guide.

Understanding outward remittance from India

Outward remittance means converting Indian Rupees to foreign currency and sending it to an overseas beneficiary through an authorized dealer bank under FEMA. Businesses pay vendors through current account transactions, individuals use the Liberalised Remittance Scheme for permitted purposes up to a yearly cap. Typical use cases include one time project invoices, recurring SaaS, milestone based contractor fees, and digital service purchases. The compliance framework ensures legitimate flows, accurate balance of payments data, and sanctions adherence, which is why banks ask for precise documents and classifications. For a friendly overview, skim outward remittance explained.

Choosing the right payment method for your vendor

Cards suit small recurring subscriptions, they are quick and simple, but FX spreads are usually higher and chargebacks worry some vendors.

Bank outward remittance via SWIFT is the gold standard for invoices and larger amounts, you get a clean audit trail, proper compliance, and predictable delivery.

Specialist fintech platforms can reduce processing time to one or two days and often improve exchange rates compared to traditional banks. Always compare total landed INR cost before you commit.

Pro tip: Whenever possible, pay in the vendor’s home currency to avoid double conversions and uncertain spreads.

For context and timelines, see outward remittance explained.

Documents you need before starting

- Vendor invoice or contract with legal name, full address, currency, amount, and detailed scope of work, avoid vague descriptions.

- Beneficiary banking details, account or IBAN, SWIFT or BIC, bank name and address, intermediary bank details if applicable.

- Purpose code that correctly classifies your transaction, we decode this below.

- Form A2, the mandatory forex application and declaration.

- Tax forms 15CA and 15CB when thresholds or taxability conditions are met.

- KYC, PAN for all, plus company incorporation documents for businesses.

Understand personal remittance caps and related nuances via foreign remittance limits.

How to pay international vendors from India, step by step

Step one: Verify vendor and invoice details

Match legal names exactly, confirm currency and amount, ensure the invoice date is current, and clarify scope to pre empt bank queries.

Step two: Select the appropriate purpose code

Map your transaction to RBI categories using the official purpose code list. If unsure, ask your relationship manager before filing.

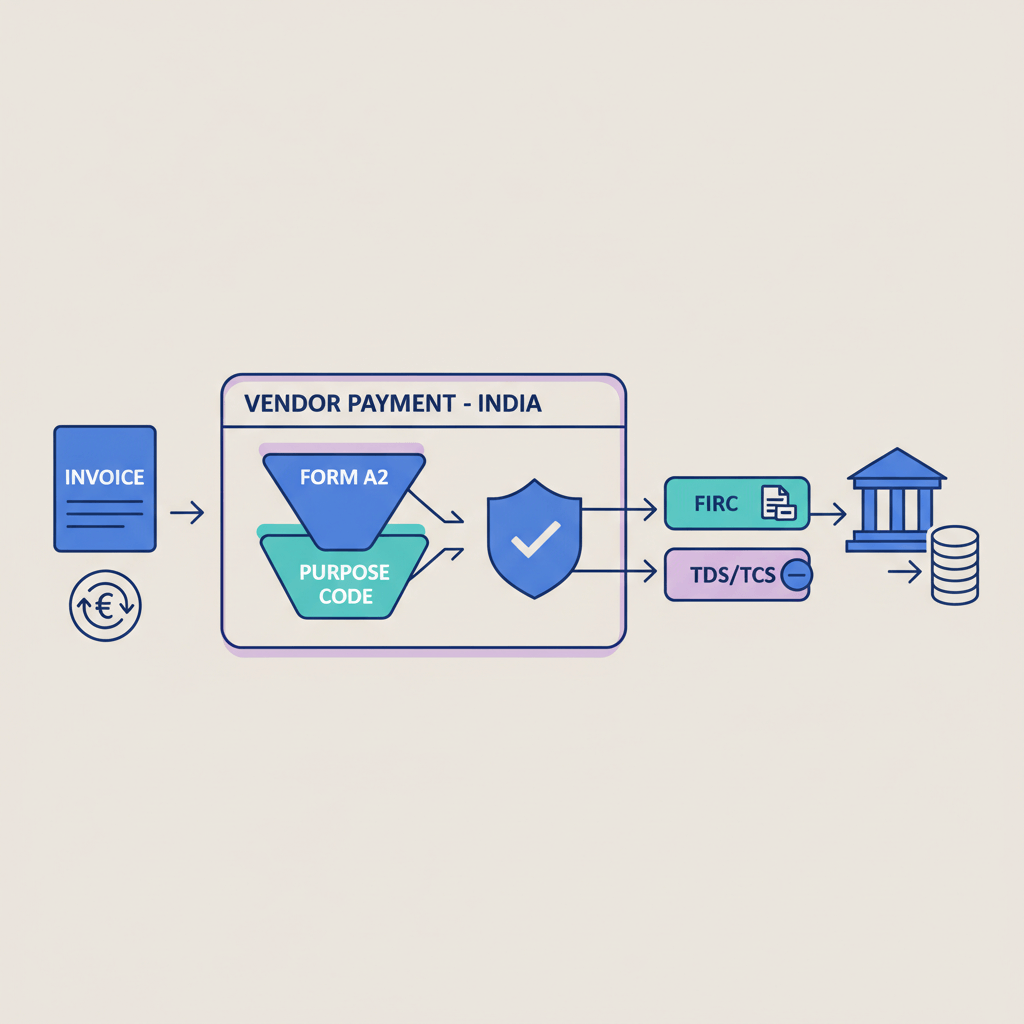

Step three: Complete Form A2 accurately

Enter remitter PAN and address per bank records, beneficiary data exactly as on the invoice and bank details, amount and currency, correct purpose code, and a clear transaction description. Many banks now accept digital Form A2.

Step four: Determine if 15CA and 15CB are required

Professional and technical services often need tax forms; goods usually do not. File Form 15CA first, then obtain CA certified 15CB as explained in this 15CA and 15CB filing guide.

Step five: Initiate the remittance with your authorized dealer bank

Submit invoice, Form A2, beneficiary details, and tax forms if applicable. Choose OUR charges so the vendor receives the full amount.

Step six: Review the FX rate and fees

Scrutinize the quoted rate and total INR debit, including bank fee and correspondent charges. If timing allows, compare alternatives to improve your rate.

Step seven: Track the SWIFT transfer

Ask for the MT103 confirmation, share it with your vendor, and use it to trace any delays through the network.

Step eight: Reconcile and maintain records

Archive the invoice, signed Form A2, bank debit advice, MT103, and tax certificates for accounting and audits. For a practical overview of costs and rules, see this complete outward remittance guide.

Everything you need to know about Form A2

Form A2 is your RBI mandated application and declaration. It captures remitter identity, beneficiary information, transaction details including purpose code, and your legal confirmation of FEMA compliance. Common errors include name mismatches, vague descriptions, missing invoices, and incorrect SWIFT or IBAN. Many banks offer digital submission with validations, though some still require wet signatures. Learn related LRS context here: foreign remittance limits.

Decoding purpose codes for outward remittance

- SaaS and cloud subscriptions are services, not goods.

- Foreign contractors and freelancers generally fall under professional or business services.

- Software licenses can be intangible goods or intellectual property rights, separate from services.

- Physical product imports use goods or import specific codes.

- Royalties and license fees have dedicated codes.

Using the wrong code can delay or reject a payment. When in doubt, validate with your bank and cross check the purpose code list for outward remittance. For a narrative explanation, see outward remittance explained.

Costs, processing times, and money saving strategies

- Bank service fees typically ₹500 to ₹2,000.

- Correspondent bank charges often $15 to $50, frequently deducted unless you choose OUR.

- FX spread is the biggest cost driver, banks may add 1 to 3 percent, fintechs can be tighter.

- GST on forex services applies to the service component.

Smart savings: batch invoices to cut fixed fees, pay in the vendor’s local currency, submit perfect documents to avoid queries, select the precise purpose code, compare exchange rates before booking, and set standing instructions for recurring payments. For a full breakdown of charges and timing, read this complete outward remittance guide.

Tax compliance and regulatory considerations

Individuals remit under LRS up to $250,000 per financial year for allowed purposes, businesses use current account transactions without a fixed annual cap. Payments that may be taxable to the non resident often require Forms 15CA and 15CB. Exemptions exist, but professional and technical services frequently need filings regardless of amount. Keep airtight records, sanctions screening is standard, and high risk corridors can require extra documentation. For a concise overview, see this outward remittance guide.

Troubleshooting common outward remittance problems

Short credited payments: use OUR charges to prevent deductions by intermediaries.

Compliance queries: respond quickly with clear explanations and documents to avoid cancellations.

Name or detail mismatches: correct immediately and create a verified vendor master for future transactions.

Lost or delayed transfers: trace using the MT103 and value date, most holds resolve once additional information is provided. For background, revisit outward remittance explained.

Real world examples

US designer, $1,200 logo: professional services code, Form A2, likely 15CA and 15CB, OUR charges, two days to credit, total about ₹1.03 lakh including a modest FX markup. Keep invoice, MT103, tax certificates on file.

European SaaS, €99 monthly: services code, standing instruction after first approval, typically no 15CA or 15CB under thresholds, fintech route saves about one percent on FX.

UK consultant, $5,000 milestone: professional services code, 15CA and 15CB required, OUR charges, better FX negotiated due to amount, roughly three business days door to door.

US software license, $3,000: intellectual property or license code, attach license agreement, verify 15CA and 15CB treatment for royalty like nature, maintain full documentation.

For charge structures and fees across cases, refer to this complete outward remittance guide.

Practical checklists and quick references

- Verify invoice details, legal name, address, currency, amount, and specific scope.

- Collect complete beneficiary bank details, account or IBAN, SWIFT or BIC, bank address, intermediaries if any.

- Pick the correct RBI purpose code using the purpose code list for outward remittance.

- Complete Form A2, ensure every field matches the supporting documents.

- Confirm if 15CA and 15CB are required, use this 15CA and 15CB filing guide.

- Choose OUR charges for business payments, avoid short credits.

- Review FX rate and total INR debit before approving.

- Save and share MT103 with the vendor, then archive the full dossier.

Form A2 structure in one glance: remitter details with PAN and address, beneficiary details with country and bank account, transaction details with currency, amount in figures and words, purpose code and description, plus the declaration block with date and signature.

Where Karbon Business fits in your international payment strategy

While this guide focuses on paying vendors, many Indian freelancers and agencies also receive client payments. Karbon Business helps with inward remittance by offering virtual accounts in USD, GBP, EUR, and CAD, settling to your Indian account in 24 to 48 hours. You get mid market Xe.com rates at zero percent markup and a flat one percent platform fee, with automatic e FIRA documentation generated within 24 hours. Managing both outward and inward flows with discipline gives you complete control over global cash management.

Moving forward with confident international payments

Build a standard checklist, maintain a verified vendor master, cultivate a responsive banker or fintech account manager, and work with a CA who understands cross border tax. With repetition, purpose code selection, tax form decisions, and documentation become routine, helping your payments clear smoothly, on time, and fully compliant.

FAQ

Form A2 har payment pe lagta hai kya, chhote amounts ke liye bhi?

Haan, India se kisi bhi outward remittance ke liye Form A2 mandatory hai, chahe $50 ho ya $50,000, yeh hi aapka forex purchase application aur FEMA declaration hota hai, isliye hamesha submit karein.

Purpose code kaise choose karu, SaaS aur freelancer payments ke liye kaunsa theek rahega?

SaaS and cloud subscriptions service category me aate hain, freelancers, designers, developers, consultants professional or business services me aate hain, license or royalty ke liye IP related codes use hote hain, quick mapping ke liye aap purpose code list for outward remittance check kar sakte hain.

Mujhe 15CA aur 15CB kab file karna hota hai, freelancer invoices pe zaroori hai?

Generally professional or technical services pe 15CA and 15CB required hote hain, goods purchases par aam taur par nahi, thresholds aur exemptions change hote rehte hain, safest approach hai apne CA se har significant payment pe confirm karna, filing steps ke liye yeh 15CA and 15CB filing guide dekhein.

OUR, SHA, BEN charges me difference kya hota hai, freelancer ko full amount kaise milega?

OUR me saare bank and intermediary fees aap pay karte ho, vendor ko full amount milta hai, SHA me fees shared hoti hai, BEN me beneficiary pay karta hai, business payments me disputes avoid karne ke liye OUR best hota hai.

SWIFT transfer ko kitna time lagta hai, aur MT103 kya hota hai?

Normally one to three business days lagte hain, fintech rails se kabhi kabhi one to two days me bhi ho jata hai, MT103 international wire ka confirmation message hota hai, isme reference number hota hai jisse aap trace kar sakte ho.

Kya main international vendor ko INR me pay kar sakta hoon, bina forex convert kiye?

Agar vendor ka Indian account hai to wo domestic payment hoga, outward remittance ke liye INR ko foreign currency me convert karna hi padega, isliye aapko bank ya fintech ke through FX conversion karna hota hai.

Payment short credit ho gaya, vendor ko kam paise mile, ab kya karu?

Check karein ki SHA ya BEN select to nahi kiya tha, intermediaries ne charges deduct kiye honge, MT103 se track karke gap identify karein, phir shortfall cover karne ke liye supplementary payment bhej dein, future me hamesha OUR choose karein.

Kya fintech services banks se better rate dete hain, aur kya documents same rehte hain?

Often fintech platforms tighter FX spreads aur faster processing dete hain, documents largely same rehte hain, invoice, Form A2, purpose code, aur zarurat padne par 15CA and 15CB, total landed INR cost compare karke decide karein.

Freelancer hoon, mujhe clients se USD, EUR me payments lena hota hai, best option kya hai?

Receiving ke liye aap Karbon Business jaise platform use kar sakte hain, yeh USD, GBP, EUR, CAD me virtual accounts deta hai, funds 24 se 48 ghanton me Indian account me settle ho jate hain, mid market Xe.com rate pe zero percent markup aur flat one percent fee hoti hai, saath me e FIRA bhi auto generate hota hai.

Purpose code galat select ho gaya to consequences kya honge, kaise fix karu?

Galat code se payment hold, rejection, ya enhanced scrutiny ho sakti hai, turant bank ko inform karke correction request raise karein, next time submit karne se pehle purpose code list for outward remittance cross check karein ya RM se confirm karein.

15CA 15CB ke bina payment bhej diya, ab compliance kaise handle karu?

Agar category me filings required thi to bank payment hold kar sakta hai ya info demand karega, apne CA ke through retro filings and clarifications karein, future payments ke liye pehle 15CA portal pe submit karein, phir CA se 15CB lein, process yahan samjhein, 15CA and 15CB filing guide.

SaaS subscription ke liye har month Form A2 bharna padega kya, koi faster workflow hai?

Haan, Form A2 required rahega, lekin aap standing instruction set kar sakte hain jahan pehli baar documentation approve hone ke baad subsequent debits faster process hote hain, purpose code clearly services choose karein aur invoice trail maintain karein.

Kya bank se better FX rate negotiate kar sakta hoon, practical tips batao?

Bigger ticket sizes par negotiate karna asaan hota hai, rate quotes compare karein, intraday volatility ka fayda uthayein, non urgent payments ko favorable windows me book karein, fintech quotes bhi lein aur total landed INR cost pe decision lein.

International consultant ko milestone payment dena hai, tax withholding kaise handle karu?

Contract and scope ke basis par withholding obligations trigger ho sakte hain, apne CA se review karwa ke 15CA and 15CB banwayein, Form A2 me professional services purpose code use karein, OUR charges select karein, documentation me invoice, contract, tax certificates attach karein.

Karbon Business mere outward remittance me kaise help karega aur kya inbound alag hota hai?

Outward remittance banks or specialist platforms se process hota hai, Karbon Business primarily inbound me help karta hai jahan aapko USD, GBP, EUR, CAD virtual accounts milte hain, zero percent FX markup at mid market, flat one percent fee, fast settlement, aur e FIRA automation, isse aap client receipts optimize kar sakte hain jabki vendor payments bank or fintech outward rails se karte hain.