Key takeaways

- Form 15CA has four parts, pick Part D when remittance is not chargeable to tax, Part A when chargeable and your aggregate is ₹5 lakh or less, Part B when you have an AO order under sections 195(2), 195(3), or 197, Part C when chargeable and aggregate exceeds ₹5 lakh with no AO order.

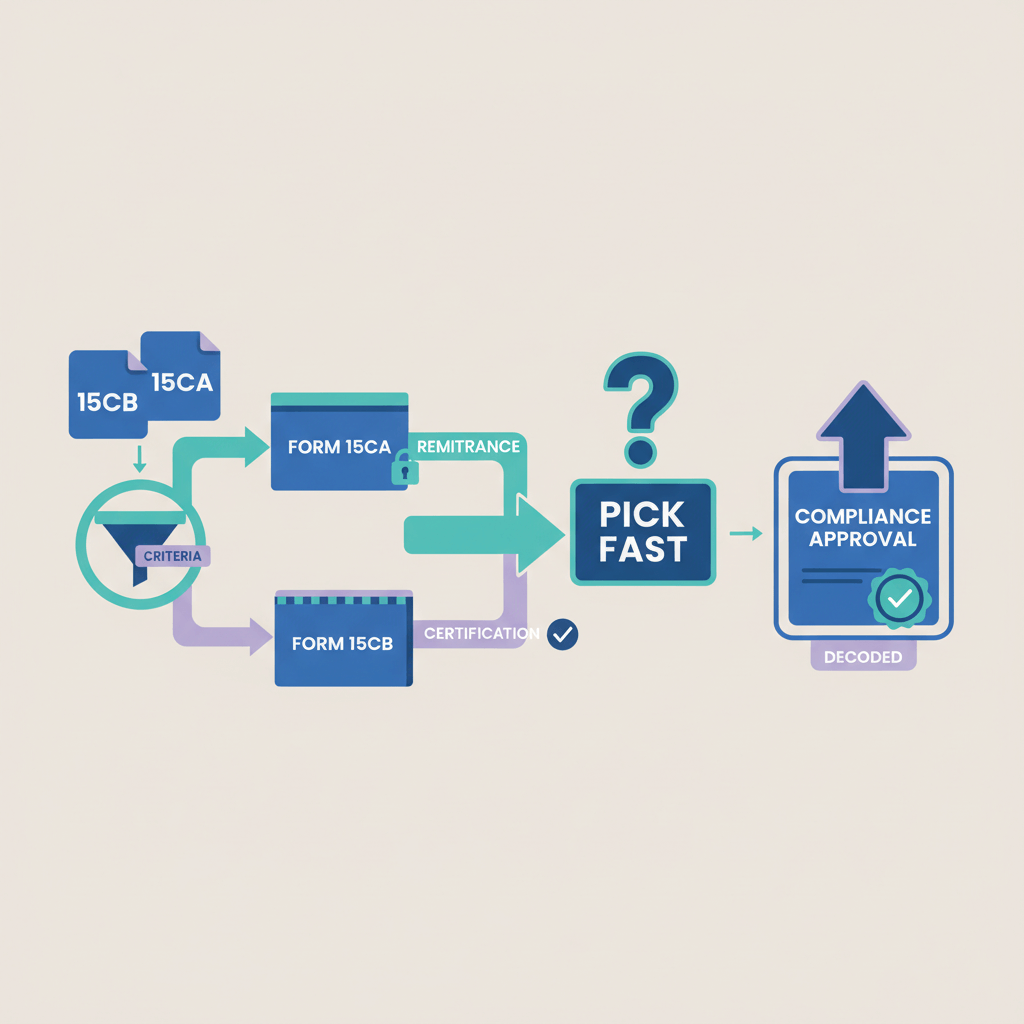

- Part C requires Form 15CB from a Chartered Accountant, your CA files 15CB first, then you file 15CA Part C by linking the 15CB acknowledgement number.

- Always check the Rule 37BB specified exemption list before filing, many categories do not require 15CA or 15CB.

- Track your aggregate of chargeable outward remittances across the financial year, crossing ₹5 lakh pushes you to Part C.

- Match your invoice description, RBI purpose code, taxability reasoning, and the selected 15CA part, mismatches trigger bank compliance holds.

Who this guide is for and why it matters

If you pay overseas SaaS, hire foreign subcontractors, or send refunds to clients abroad, your bank asks for Form 15CA, then the maze starts, Part A, B, C, or D, do you also need Form 15CB, what about the ₹5 lakh threshold. Pick the wrong part, your payment pauses, vendors wait, clients escalate, timelines slip. This guide clarifies the parts, the thresholds, and the 15CB linkage so Indian freelancers avoid delays and compliance holds.

One clean framework, consistent documents, and the right 15CA part, that is the difference between a smooth wire and a week of back and forth.

Basics, what are Form 15CA and Form 15CB?

Form 15CA is an online declaration under Rule 37BB for outward remittance to non residents, filed before the bank processes your payment. For a friendly primer, see the HDFC Life explainer on Form 15CA and Form 15CB. The official steps live in the Income Tax Department Form 15CA user manual.

Form 15CB is a Chartered Accountant certificate that analyzes taxability, DTAA, and TDS rate, context and use cases are explained here, Form 15CB requirement, and the official guidance sits in the Income Tax Department Form 15CB user manual.

You file Form 15CA on the portal, download the acknowledgement, and submit it to your bank with invoices and KYC. When 15CB is required, your CA files it first, you then link its acknowledgement number inside 15CA Part C.

Decision framework, which 15CA part to select

Step 1, check exemptions under Rule 37BB

Many remittances need neither 15CA nor 15CB. Review the Rule 37BB specified list and confirm with your bank.

Step 2, assess taxability

If the payment is not chargeable to tax under the Income tax Act or an applicable DTAA, file Part D, explain the reason, and attach supporting documents. No 15CB is needed.

Step 3, if chargeable, apply thresholds and orders

- Part A, chargeable remittances, aggregate in the financial year is ₹5 lakh or less, no 15CB required.

- Part B, you hold an Assessing Officer order under 195(2), 195(3), or 197 permitting nil or lower TDS, no 15CB required.

- Part C, chargeable remittances, aggregate exceeds ₹5 lakh, no AO order, 15CB is mandatory.

Aggregate means the total of all your chargeable outward remittances in the current financial year. For deeper context, see this ClearTax filing guide.

15CA Part A vs B vs C vs D explained

Part A

Use Part A when the remittance is chargeable to tax and your aggregate remains at ₹5 lakh or less. Provide remittee details, amount, nature of payment, and TDS challan if applicable.

Part B

Use Part B when you possess an AO order under sections 195(2), 195(3), or 197, reference the order number and date, the threshold is not relevant because the order governs TDS.

Part C

Use Part C when the remittance is chargeable, your aggregate exceeds ₹5 lakh, and there is no AO order. Obtain 15CB first, then file Part C by linking the 15CB acknowledgement number, your bank will verify both before processing.

Part D

Use Part D when the remittance is not chargeable to tax, enter the reason and attach supporting documents. No 15CB is required.

Remember, if your payment is in the specified exemption list under Rule 37BB, skip 15CA and 15CB entirely.

15CB linkage, how 15CA and 15CB connect

Your CA files 15CB first, the portal generates an acknowledgement number, you then file 15CA Part C and enter that number to link the two. Banks cross check this linkage and may verify the CA’s UDIN. A practical overview for NRIs and residents is here, Form 15CA 15CB for transferring personal funds.

If any link or detail mismatches, the bank will hold the payment and ask for corrections before release.

Practical how to, filing on the e filing portal

Gather PAN, remittee details, RBI purpose code, AD code, amount and currency, invoice or contract, and, if relevant, the 15CB acknowledgement and TDS challan. Follow the Income Tax Department Form 15CA user manual for portal steps. Many CAs share process checklists, for instance Slohia & Co’s service overview.

- Part A, enter remitter and remittee details, nature of remittance, purpose code, amount, TDS challan if any, confirm aggregate is within ₹5 lakh, submit and download acknowledgement.

- Part B, add AO order number, date, section, permitted rate, submit and download acknowledgement.

- Part C, enter the 15CB acknowledgement number, fill DTAA details and TDS challan if applicable, submit and download acknowledgement.

- Part D, choose not chargeable to tax, state the reason clearly, submit and download acknowledgement.

Freelancer specific examples

- Refund to an overseas client, a cancelled project advance is usually a capital refund, file Part D with a brief reason such as refund of advance, not income, DTAA or domestic law basis.

- Paying a foreign subcontractor, if services are performed outside India with no permanent establishment in India, you may claim DTAA non taxability, use Part D with robust documentation, or Part C with 15CB if aggregate exceeds ₹5 lakh or if the bank requests a CA certificate.

- Annual SaaS subscription, if chargeable to tax, use Part A when the aggregate is within ₹5 lakh, deduct and deposit TDS at the applicable rate, if aggregate exceeds ₹5 lakh, move to Part C with 15CB.

- AO certificate for a large consulting payment, when you have an AO order for nil or lower TDS under section 195, file Part B, the threshold does not apply, no 15CB needed.

Common mistakes to avoid

- Filing 15CA for Rule 37BB exemptions, always check the specified list first.

- Continuing with Part A after crossing ₹5 lakh aggregate, switch to Part C once you cross the threshold.

- Claiming DTAA benefit without TRC and documentation, collect TRC, invoice, contract, and consider a 15CB even for Part D when analysis is complex.

- Purpose code, invoice, and 15CA nature mismatch, ensure all three tell the same story.

- Attempting Part C without prior 15CB, the portal requires the 15CB acknowledgement number.

- Deducting TDS but skipping challan details in the form, reference the challan to avoid future notices.

Bank workflow and documents

Banks need your 15CA acknowledgement, 15CB certificate or acknowledgement for Part C, invoice or contract, correct RBI purpose code, standard KYC, and AO certificate for Part B. For a banker’s perspective, see Axis Bank’s note on Form 15CA and 15CB.

Delays usually arise from missing 15CB linkage, expired TRC, or mismatched names, amounts, and dates. Submit a complete set, follow up politely, and you will typically clear compliance in a couple of days.

Updates and caveats

Thresholds, lists, and interpretations evolve, always check the official user manual and consult your CA for unusual scenarios. Portal fields may change, menu locations can shift, and DTAA case law can update treatment of fees and royalties.

Quick checklist before remitting

- Is the payment in the Rule 37BB specified list, if yes, skip 15CA and 15CB.

- Is the payment chargeable to tax, if not, file Part D with reasons and supporting documents.

- What is your aggregate of chargeable remittances this year, switch from Part A to Part C once you cross ₹5 lakh.

- Do you have an AO order under 195(2), 195(3), or 197, if yes, file Part B.

- For Part C, has your CA filed 15CB, do you have the acknowledgement number.

- Do invoice description, RBI purpose code, and 15CA nature align.

- Have you deducted and deposited TDS when required, do you have the challan.

- Did you download the 15CA and 15CB acknowledgements, banks prefer PDFs.

- Are all supporting documents ready, invoice, contract, KYC, AO order, TRC if DTAA benefit claimed.

- Do names, amounts, dates, and account numbers match across all papers, review twice.

How Karbon Business helps with compliance and payments

Karbon Business focuses on receiving international client payments for Indian freelancers, offering virtual USD, GBP, EUR, and CAD accounts, local rails like ACH or SEPA on the client side, INR settlement in 24 to 48 hours, and automated e FIRA for compliance. Clean inward records make outward paperwork simpler, if you later pay a SaaS bill or a subcontractor, your inward e FIRA is a tidy proof of foreign income in your files. Learn more at Karbon Business.

Alternatives for cross border payment management

- Karbon Business, India first inward platform with automated e FIRA and fast INR settlement.

- Wise Business, popular for transparent fees and mid market FX, some India compliance steps may be manual.

- Payoneer, broad marketplace integrations, fees vary by route and currency.

- PayPal, easy setup, higher fees, and FX markups, better for small amounts than large invoices.

- RazorpayX International, growing cross border capabilities within a domestic payment suite.

Final thoughts

Master the flow, exemption list first, assess taxability next, apply the ₹5 lakh aggregate, then pick A, B, C, or D. Engage your CA early for 15CB when Part C applies, align invoice, purpose code, and narrative, and share a complete pack with your bank. A deliberate five minute review saves days of refiling and compliance holds.

FAQ

Bank bol raha hai 15CA Part A ya Part C, mera aggregate kaise count karu aur kya 15CB zaroori hai?

Aggregate means your total chargeable outward remittances in the same financial year. If the payment is chargeable and your aggregate is ₹5 lakh or less, use Part A, no 15CB needed. If the aggregate crosses ₹5 lakh and there is no AO order, use Part C and get Form 15CB from your CA first. Track all chargeable payments from April onwards so you switch at the right time.

DTAA benefit claim karna hai, kya Part D enough hoga ya CA ka 15CB bhi chahiye?

If your remittance is genuinely not chargeable to tax due to DTAA, Part D is correct, but banks usually ask for strong documentation, for example Tax Residency Certificate, contract scope, and invoice. When the analysis is complex, a CA issued 15CB strengthens your case even for Part D, it prevents delays and clarifies the tax position.

AO certificate mil gaya under section 195, ab kaunsa 15CA part file karu?

When you have an Assessing Officer order under section 195(2), 195(3), or 197 allowing nil or lower TDS, file Part B. The ₹5 lakh threshold does not apply in this scenario and 15CB is not required because the AO order itself provides tax authority approval.

Vendor Philippines mein hai, services India mein perform nahi hui, bank ko kaise samjhau ki tax chargeable nahi hai?

Prepare a clear Part D filing, explain that the services were performed outside India, no permanent establishment in India, and cite the relevant DTAA article. Attach TRC and contract, and keep an invoice that matches the RBI purpose code. If the bank still wants a CA opinion, ask your CA for 15CB to document non taxability.

SaaS subscription UK se pay kar raha hoon, TDS ka kya scene hai aur kaunsa part choose karu?

Many SaaS payments can be treated as royalty or fees for technical services depending on the DTAA. If chargeable and your aggregate is within ₹5 lakh, file Part A, deduct TDS at the applicable DTAA or domestic rate and deposit via the correct challan. If your aggregate exceeds ₹5 lakh, move to Part C and obtain 15CB from your CA.

Part C file karne se pehle 15CB acknowledgement number kahan se aayega?

Your Chartered Accountant must file 15CB on the Income Tax portal first, once submitted it generates a 15CB acknowledgement number. You then enter that number inside your 15CA Part C form, the portal links both filings automatically. Without this number, you cannot complete Part C and the bank will not process the remittance.

Rule 37BB exemption list mein agar mera payment aata hai, fir bhi 15CA file karna padega?

No, if your remittance falls under the specified exemption list in Rule 37BB, you do not file 15CA or 15CB. Provide the invoice and KYC to your bank and proceed. Always verify the latest list and confirm with your branch to avoid unnecessary filings.

Invoice description aur RBI purpose code mismatch ho gaya, bank ne payment hold kar diya, ab kya karu?

Request a correction, align the invoice description to the correct RBI purpose code, and ensure your 15CA part and nature of remittance fields match that story. Provide a cover note explaining the correction, attach the updated invoice or clarification, and ask the bank to lift the compliance hold.

Freelancer ke liye ₹5 lakh threshold practical kaise track karu, koi simple system batao?

Maintain a running spreadsheet of all outward remittances that are chargeable to tax, capture date, amount, currency, INR equivalent, purpose code, and whether a 15CA part was filed. Sum the INR equivalent for the year, once the total touches ₹5 lakh, switch to Part C and engage your CA for 15CB before the next payment.

Karbon Business use karte hue inward payments smooth hain, outward remittance ke liye koi shortcut milega?

Karbon Business streamlines inward collections and generates e FIRA automatically, which keeps your books clean for tax time. Outward remittance must still go through your bank and the Income Tax portal with 15CA, and 15CB where required. The practical shortcut is preparation, have invoices, TRC, purpose code, and your aggregate tracker ready, and involve your CA early for Part C remittances.

Bank ne UDIN verify karne ko bola for 15CB, ye kya hota hai aur kyun important hai?

UDIN is the Unique Document Identification Number issued by the ICAI for CA certificates. Banks sometimes verify UDIN to ensure the 15CB certificate is genuine and current. Ask your CA to share the UDIN on the 15CB, provide it to your bank, and keep the acknowledgement PDFs in your records.

Refund of advance client ko dena hai, kya Part D sahi hai, koi example do?

Yes, refunds of advances for cancelled projects are typically capital in nature, not income, so they are not chargeable to tax. File Part D, state refund of advance, not income, and attach the original invoice or agreement showing the advance. Ensure your reason field references domestic law or DTAA context if helpful.

TDS deduct kiya but 15CA form mein challan details miss ho gaye, kya penalty aayegi?

If TDS was applicable and deducted, you should enter the challan details in the 15CA form. Missing details can trigger queries later. Reconcile immediately, keep the challan copy, and respond to any notice with the challan reference. For future filings, add challan to your checklist so the form and your TDS record match.