Key takeaways

- For most Indian freelancers, local UK transfers to a virtual GBP account, then fast INR settlement, deliver the lowest total cost and quickest timelines.

- Understand SWIFT fees in detail, sender bank fees, intermediary deductions, and receiving bank charges, then choose OUR charges when a client insists on SWIFT.

- Aim for platforms using mid market GBP to INR rates with zero FX markup and a transparent platform fee, predictable cash flow beats speculative FX timing.

- Always collect proof, invoice plus contract, correct RBI purpose code, and an e-FIRA or equivalent inward remittance certificate for RBI, FEMA, and tax.

- Set up clean processes, detailed invoices, accurate beneficiary details, and clear payment references, to avoid delays and compliance holds.

Understanding UK to India Payments: Your Main Options

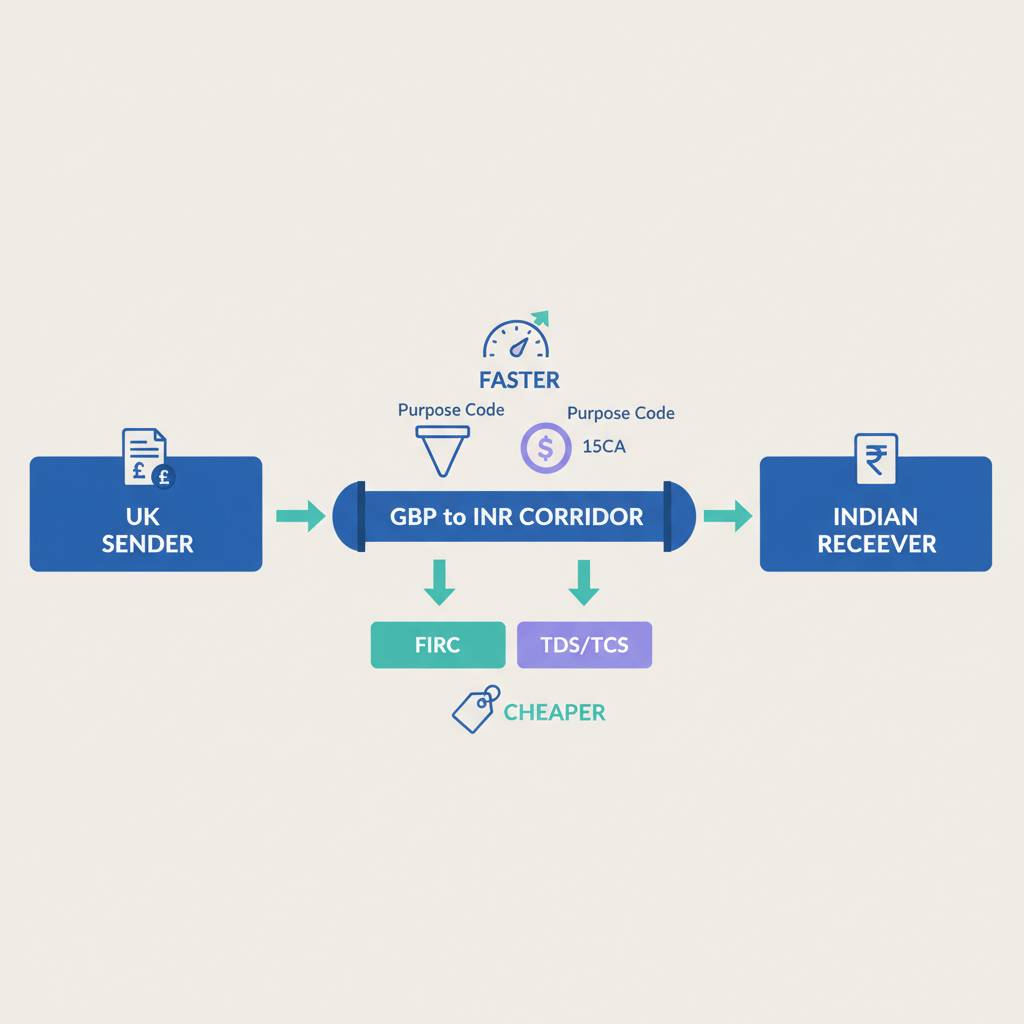

Receiving GBP payments from UK to India shouldn’t be confusing. In practice, freelancers have three primary rails that each trade off cost, speed, and compliance ease.

Local UK GBP transfers to a virtual GBP account, then converted to INR

Your client sends a domestic UK transfer, Faster Payments, BACS, or CHAPS, to a virtual GBP account in your name. You essentially get UK bank details, a sort code and account number, without opening a physical UK account. The platform converts GBP to INR, then settles to your Indian bank, usually within 24 to 48 hours.

SWIFT international wire directly to India

Your UK client sends a SWIFT transfer in GBP straight to your Indian bank using your SWIFT or BIC, account number, IFSC, and other beneficiary details. This is often preferred for larger B2B amounts, but costs are higher and less predictable because of layered SWIFT fees.

Wallets and payment processors

Your client pays via a wallet or payment gateway, then you withdraw to INR. Convenience is high, but the effective cost is typically much higher once FX markup and withdrawal fees are included. This suits marketplace work or card-first clients, not routine invoices.

For most Indian freelancers, a local UK transfer to a virtual GBP account is the default winner on cost and speed. To compare choices, see best ways to accept GBP payments in India.

Breaking Down Fees and Timelines for Each Method

Local UK GBP transfer to INR via a fintech account

How it works

A fintech gives you local UK bank details as a virtual GBP account. Your client sends an FPS, BACS, or CHAPS domestic transfer in GBP, you claim and convert, then receive INR in your Indian bank.

Fees

Modern platforms often charge around a flat 1% on inward remittance. If they use mid market FX with zero FX markup, your GBP to INR closely matches what you see on rate trackers.

Timelines

FPS usually arrives within minutes to a few hours for the GBP leg. After you claim and convert, INR settlement typically lands within 24 to 48 hours.

Result: predictable, affordable, and fast, ideal for repeat invoices.

SWIFT wire to India and understanding SWIFT fees

How it works

Your client initiates a SWIFT wire in GBP to your Indian bank, the payment may pass through one or more correspondent banks before reaching India.

Typical fee components

- Sender bank fee: roughly £15 to £40.

- Intermediary deductions: often £10 to £25 or more, unpredictable because multiple banks can take their cut.

- Receiving bank fee in India: varies by bank, sometimes fixed, sometimes percentage based.

Charge types

SHA: client pays their bank’s fee, you bear intermediary and receiving deductions.

OUR: client pays all SWIFT fees, you receive the full amount, best for freelancers.

BEN: you pay all fees, strongly not recommended.

Timelines

Usually 1 to 5 business days to land. Delays happen for compliance checks, wrong beneficiary details, missing purpose codes, or bank holidays.

For a broader comparison of methods freelancers use, see freelance payment methods in India.

Wallets and payment processors

Examples

PayPal, Payoneer, Stripe, and similar gateways.

Effective costs

The true total often runs 3 to 6% after you include cross border fees, FX markup, and withdrawal charges. Some platforms add fees for chargebacks or disputes too.

Timelines

Funds show up in your platform balance in 1 to 3 days, withdrawal to INR takes another 1 to 5 days depending on your bank and batching cycles.

For a perspective on wallet based options used by freelancers, see freelancer payment method.

Understanding GBP to INR Exchange Rates

Mid market rate vs bank FX markups

The mid market rate is the real rate, the midpoint between buy and sell prices in the interbank market. Many banks and wallets add a markup of 2 to 4% on top, so you silently lose money in addition to visible fees. Platforms that promise zero FX markup pass on the mid market rate and charge a transparent platform fee, which keeps your effective cost down.

Example GBP to INR calculation

Invoice amount: £1,000. Assume mid market GBP to INR is ₹110. Platform fee: 1%, zero FX markup.

Step 1: Gross INR = £1,000 × ₹110 = ₹110,000.

Step 2: Platform fee = £10 = ₹1,100.

Step 3: Net INR received = ₹110,000 minus ₹1,100 = ₹108,900.

Compared to a wallet with 3.5% effective cost, you’d lose ₹3,850, a difference of ₹2,750 on a single invoice.

Should you hold GBP or convert immediately?

Some platforms let you hold a GBP balance and convert later, which offers light FX flexibility. Convert immediately if GBP to INR looks strong or you need cash flow now. Consider holding for up to around 60 days if your provider allows, and you expect the rate to improve. Don’t try to time the market, predictable cash flow beats speculation. For more context, check how to receive money from UK clients in India.

Compliance and Proof Requirements for UK to India Payments

What proof Indian freelancers need

- Invoice and contract with the UK client.

- Correct RBI purpose code when claiming or converting the payment.

- e-FIRA or equivalent foreign inward remittance certificate from the AD Category I bank or fintech.

Why proof matters

RBI and FEMA require foreign inflows to be reported as export proceeds, while income tax and CA audits rely on matching invoices with e-FIRAs to verify foreign income and benefits. Your documentation also supports visas, loans, or registrations later.

How to obtain proof: the e-FIRA

Modern platforms often auto generate e-FIRA within about 24 hours of settlement, accessible from your dashboard to view, download, and share. This saves you from branch visits and follow ups. For a practical overview, see getting paid by international clients.

Step by Step: How to Receive GBP Payments from UK to India

Step 1: Onboarding and KYC

Provide PAN, masked Aadhaar, last three months bank statements, and a basic professional profile such as Upwork, LinkedIn, a portfolio site, or Instagram for creators. KYC usually completes in 2 to 4 working days. Once approved, you receive a virtual GBP account with UK details.

Step 2: Create and send invoice with local GBP details

Issue a GBP invoice that clearly states your name as per KYC, virtual account sort code and account number, invoice number, due date, and service descriptions. Add Indian bank details and GSTIN if relevant, then email it to your UK client.

Step 3: Client pays from the UK

Ask the client to pay via FPS or CHAPS to your virtual GBP account. This is a domestic transfer for them, generally low cost and fast. For larger B2B, some providers also support SWIFT to the collection bank. Payment links can help smaller invoices or card-first clients.

Step 4: Claim payment and convert to INR

When GBP credits your virtual account, claim it in your dashboard, choose the correct purpose code, and select your Indian bank for settlement. The conversion uses mid market GBP to INR with zero FX markup, and charges a transparent fee, often around 1%. INR lands in 24 to 48 hours.

Step 5: Download your e-FIRA for compliance

Within about 24 hours of settlement, download the e-FIRA PDF for that payment and share it with your CA. This serves as primary proof for RBI, FEMA, and tax filings.

Practical Scenarios and Tips

Scenario 1: Small recurring invoices (£300 to £2,000)

Best method: local UK transfer to a virtual GBP account, then convert to INR.

Why: around 1% effective cost, mid market FX, fast timelines, and automatic proof via e-FIRA, perfect for retainers or milestone billing.

Scenario 2: Large B2B invoices (£10,000 and above)

Option: use SWIFT when the client’s finance policy requires it, and request OUR charges so the client bears all fees. Expect 2 to 5 business days and occasional compliance queries.

How to reduce errors and delays

- Ensure the beneficiary name matches exactly across invoice, fintech account, and KYC documents.

- Ask the client to include your invoice number and name in the payment reference.

- Always choose the correct RBI purpose code when claiming funds.

- Avoid conversions near weekends, or UK and Indian bank holidays.

Smart FX strategy for freelancers

Convert immediately if the rate looks strong and cash flow is urgent, hold briefly if your platform allows and the rate is weak, but avoid speculation. A simple rule: if you need the money this month, convert, otherwise hold a short while and monitor daily.

Chargeback and fraud hygiene

Use formal contracts and invoices, keep a clean record of invoices, e-FIRAs, and bank statements in cloud folders, and maintain clear email trails. This helps in client disputes, audits, visa or loan processes, and ensures your compliance is airtight.

Comparing Tools for Receiving GBP Payments in India

Choose platforms designed for Indian compliance, transparent fees, and fast INR settlement.

- Karbon Business: virtual GBP, USD, EUR, and CAD receiving accounts with local transfer capability, flat 1% platform fee, zero FX markup at mid market rates, INR settlement in 24 to 48 hours, automatic e-FIRA within 24 hours, built for Indian freelancers and small service providers.

- Wise Business: multi currency account with localized details, transparent fees, but withdrawals can add up for frequent invoices.

- Payoneer: common for marketplaces, virtual USD and EUR receiving, fees and markups tend to be higher than India focused fintechs.

- PayPal: widely accepted, convenient, but expensive for regular invoice flows once FX and withdrawal fees stack.

- Revolut Business: multi currency account, check current India availability and compliance status.

Quick Fee and Timeline Comparison Snapshot

- Local UK GBP to INR via fintech: around 1% fee with zero FX markup if mid market rates are used, settlement in 24 to 48 hours after claiming.

- SWIFT bank transfer: total fees often £25 to £60 or more across sender, intermediaries, and receiver, timeline 1 to 5 business days, amounts may arrive short under SHA or BEN.

- Wallets and processors: 3 to 6% effective cost after markups and withdrawals, timeline 2 to 7 days end to end.

Choosing the Right Path for Your UK Payments

The reliable default for freelancers is simple, set up a virtual GBP account, ask UK clients to pay via local FPS transfers, convert to INR at mid market rates with a transparent platform fee, and save the auto generated e-FIRA for compliance. Use SWIFT only when required for large B2B, and wallets when convenience outweighs the higher effective cost. With this setup, receiving GBP payments from UK to India becomes predictable, affordable, and audit ready, so you can focus on work.

FAQ

How can I receive GBP from a UK client to my Indian bank with minimum fees?

Use a virtual GBP account and ask your client to send an FPS or BACS domestic transfer, then convert GBP to INR at mid market rates with a transparent platform fee, for example Karbon Business charges around 1% and settles INR in 24 to 48 hours.

FPS to virtual account versus SWIFT wire, which is better for my GBP invoice?

For invoices under about £5,000, local UK transfers to a virtual GBP account are cheaper and faster, SWIFT is best reserved for larger B2B or when the client’s finance team mandates it, if using SWIFT, request OUR charges so you receive the full amount.

What is e-FIRA and how do I download it for my CA?

e-FIRA is the electronic Foreign Inward Remittance Advice issued by the AD bank, compliant platforms like Karbon Business auto generate an e-FIRA within about 24 hours of settlement, you can download the PDF from your dashboard and share it with your CA for audits and tax filings.

How to add purpose code while claiming foreign remittance from UK?

During the claim or conversion step, select the RBI purpose code that matches your service, for example software services, IT consulting, professional fees, or design, platforms like Karbon Business provide clear purpose code options in the flow to reduce errors and settlement delays.

If my client pays via PayPal or card, what will be the total cost for me?

Expect an effective cost of around 3 to 6% after FX markup, cross border fee, and withdrawal charges, wallets are convenient for card-first clients or marketplaces, but for routine invoices you will usually save more with local UK transfers to a virtual GBP account.

What are OUR, SHA, and BEN in SWIFT fees, which should I choose?

SHA means shared fees, you bear intermediary and receiving deductions, BEN means you pay all fees, avoid it, OUR means the sender pays all fees so you receive the full amount, when a client insists on SWIFT, request OUR to protect your invoice value.

How do I get UK sort code and account number as an Indian freelancer?

Open a virtual GBP account with an India compliant fintech, for example Karbon Business, after KYC you receive UK bank details, sort code and account number, which your client can pay via FPS or CHAPS like a domestic UK transfer.

How is GBP to INR calculated, do platforms add FX markup?

Transparent platforms pass the mid market rate without FX markup and charge a clear platform fee, for instance about 1%, this keeps the effective cost low compared to banks or wallets that add 2 to 4% FX markup on top of visible fees.

FPS credit time and INR settlement, how long should I plan for?

UK FPS credits typically in minutes to a few hours, once you claim and convert, INR settlement generally arrives in 24 to 48 hours, set expectations with clients accordingly and avoid conversions near UK or Indian bank holidays to reduce delays.

Can I hold GBP balance for some time under RBI rules?

Many fintechs let you hold a GBP balance for a limited period to manage FX risk, for example up to several weeks, check your provider’s exact limits, if cash flow is tight, convert immediately, otherwise hold briefly and monitor rates daily.

Is GST applicable on export of services when my client is in the UK?

Exports of services are typically zero rated subject to conditions, you still need proper documentation, invoice, contract, purpose code, and inward remittance proof like e-FIRA, consult your CA for specifics based on your registration and service category.

What should I include in a GBP invoice to avoid payment or compliance issues?

Include your legal name as per KYC, virtual GBP sort code and account number, invoice number and due date, clear service descriptions, optional Indian bank details and GSTIN, and ask the client to put your invoice number and name in the payment reference so matching is instant on the platform.