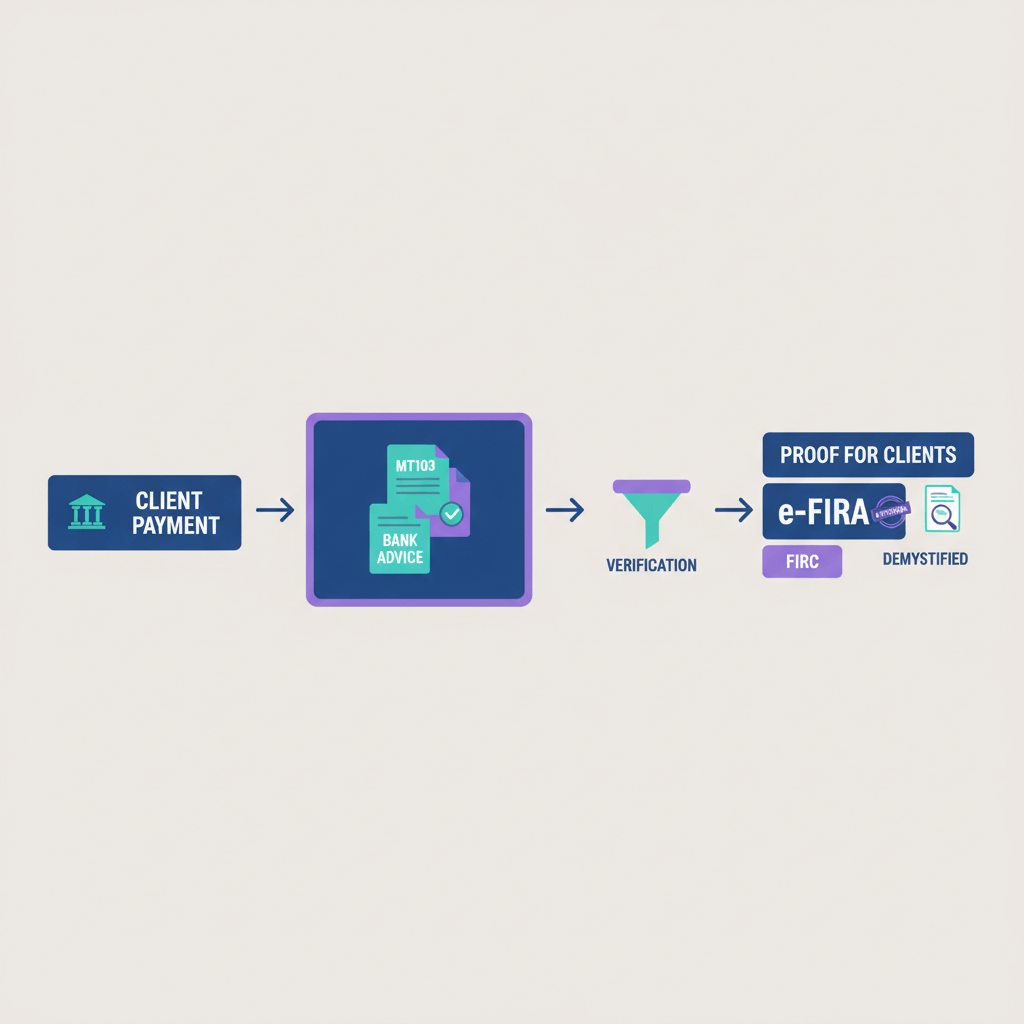

Key takeaways

- For SWIFT wires, send your paid invoice plus bank advice after credit, use the client’s SWIFT MT103 only if tracing is needed before funds arrive.

- For ACH, SEPA, or FPS, share paid invoice plus bank advice, then download e-FIRA within 24 hours for Indian compliance.

- Bank advice is the primary client facing receipt, e-FIRA is an India compliance record you must keep for ITR, GST refunds, and export benefits.

- MT103 is a sender side proof, like shipment tracking for a wire, request it from your client if the payment is delayed or requires traceability.

- Build a standard proof pack for every remittance, paid invoice, bank advice, e-FIRA, and MT103 when relevant.

- Use privacy best practices, redact account numbers, watermark shared PDFs, and ensure names match across invoice, bank advice, and e-FIRA.

- Consider platforms like Karbon Business that auto generate e-FIRA, provide transparent FX, and settle quickly to INR.

Quick answer, what should you share when?

If your client paid via SWIFT, share your paid invoice plus bank advice once funds credit. If they need confirmation before credit, ask them for their SWIFT MT103. For your compliance, download e-FIRA when available.

If your client paid via ACH, SEPA, FPS, or another local rail, share your paid invoice plus bank advice, then add e-FIRA once it generates, usually within 24 hours.

If the client asks for proof before funds arrive, request their bank’s MT103 for SWIFT or a local payment confirmation with a reference ID. You can share your receipt documents only after credit.

Think of MT103 as the sender’s tracking slip, bank advice as your received delivery note, and e-FIRA as your Indian government compliance receipt.

Understanding the documents, definitions and when to use what

Proof of payment for clients, what you share

Client facing proof includes your paid invoice or receipt, bank advice or credit advice, a statement line with the inbound remittance, and transaction references like UETR, UTR, or local payment IDs. These confirm the invoice is settled and funds reached your account.

SWIFT MT103, the official wire message

SWIFT MT103 is issued by the sender’s bank, it includes UETR, sender and receiver BICs, beneficiary details, amount and currency, value date, charges code field 71A with OUR, SHA, or BEN, and reference narrative. It is the strongest sender side proof if money has not landed yet, ask your client for it to trace delays.

Bank advice, your receipt after credit

Bank advice is the official confirmation from your Indian AD bank or fintech partner. It shows your name and account, credit timestamp, foreign currency and INR amounts, exchange rate, unique transaction reference, and sender details where available. Clients accept this as definitive proof that funds were received.

FIRC vs e-FIRA, India compliance documents

The RBI moved from physical FIRC to digital e-FIRA. It is generated by AD banks or authorized fintech partners, contains RBI purpose code, remitter details, amount, exchange rate, and reference numbers, and it is essential for ITR, GST refunds, and export benefits. Clients may ask for it, but it primarily serves your Indian compliance.

What each document should contain, quick checklists

Paid invoice or receipt

- Invoice number and date, client and your business name

- Scope of services or goods, currency and total amount

- Paid status with payment date and method, for example wire, ACH, SWIFT

- Your bank details if relevant for tracing

SWIFT MT103, requested from client if tracing is needed

- UETR, sender and receiver bank BICs

- Beneficiary name and account

- Amount, currency, and value date

- Field 71A charges code, OUR, SHA, or BEN

- Intermediary bank details if any, and payment narrative

Bank advice, your receipt after credit

- Bank header, your name and masked account number

- Credit date and timestamp

- Foreign currency amount, INR equivalent, and FX rate

- Unique reference, UTR, UETR, or internal bank ref

- Sender details when available, and transaction narration

e-FIRA, previously called FIRC

- AD bank or fintech partner name

- Beneficiary details, RBI purpose code, for example P0802, P0803

- Remitter name and country

- Foreign currency amount, INR amount, and exchange rate

- Date of remittance and credit, UTR or reference number

Scenario based guidance, real world use cases

Scenario 1, client’s finance team needs immediate proof

Send your paid invoice plus bank advice as soon as the credit appears. If they want pre credit traceability for SWIFT, ask them for their SWIFT MT103. Follow up with e-FIRA within 24 hours if they require it for compliance.

Scenario 2, client claims payment sent but funds have not arrived

Request MT103 or local confirmation with reference ID from the client, share it with your bank to trace. Review field 71A for charges code to understand fee deductions. Once funds credit, send bank advice and e-FIRA to close the loop.

Scenario 3, payment from marketplace platforms

Share the platform receipt showing settlement, then share bank advice once INR lands, keep e-FIRA for your ITR and GST records. Most platforms generate e-FIRA or equivalents within a day.

Scenario 4, large B2B retainer or multi month project

Maintain a monthly proof pack, paid invoice, bank advice, e-FIRA, and MT103 if traced. Store consistently to simplify reconciliation and audits.

How to request the right document from your client

Email template, before payment arrives

Hi [Client],

Could you please confirm the payment details for invoice #XXX? If you have initiated a SWIFT wire, please share the SWIFT MT103 from your bank once it is sent. If you are using ACH, SEPA, or a local transfer, a payment confirmation with the reference ID would help.

Once funds arrive, I will share the bank credit advice and final confirmation.

Thanks!

Email template, after payment arrives

Hi [Client],

Invoice #XXX is settled. Attached, Paid invoice, Bank credit advice.

If you need e-FIRA for your records, I can provide it within 24 hours.

Best regards,

[Your Name]

Privacy and redaction best practices

- Redact account numbers, show only last four digits

- Hide unrelated balances or pages

- Watermark sensitive PDFs, for example, For [Client] Invoice #XXX Confidential

- Verify name alignment across invoice, bank advice, and e-FIRA

- Check currency amounts match, foreign currency and INR conversion

Step by step, assembling a remittance proof pack efficiently

- Issue a correct invoice with entity details, dates, deliverables, and currency.

- Client initiates payment via SWIFT, ACH, SEPA, FPS, or card.

- Funds credit to your account, the AD bank or fintech posts the entry.

- Mark the invoice paid, download bank advice, share both with the client.

- Download e-FIRA within 24 hours and file it for compliance.

- For pre credit tracing on SWIFT, request MT103 from the client and share with your bank.

- Store the proof pack, invoice, bank advice, e-FIRA, and any MT103 in one folder.

Troubleshooting and timelines, India specific realities

Typical settlement windows

Local rails like FPS and NEFT generally settle same day or next business day, SWIFT wires settle within one to three business days, ACH and SEPA take one to five business days, and fintech settlements to INR usually complete within 24 to 48 hours after claim.

If payment is delayed

- Verify UETR status for SWIFT, many banks provide gpi tracking.

- Check field 71A for charges code, OUR, SHA, or BEN, align expectations on fees.

- Confirm beneficiary details with your bank, account number, IFSC, and name must match.

- Ensure the RBI purpose code is correct, mismatches can cause holds.

- Ask about intermediary banks, they can add one to two days to settlement.

Chargebacks or card disputes

Keep a clear invoice and scope, communication trail, bank advice showing credit, and proof of delivery or work completion. With solid documentation, disputes are resolved faster.

Compliance corner, clearing up FIRC and e-FIRA confusion

Why e-FIRA matters in India

e-FIRA is required for ITR, GST refunds, and many export benefits. It proves the source and legitimacy of foreign income, and maps to RBI and DGFT systems where applicable.

Key misconception, do I still need FIRC

Yes, but in digital form. Physical FIRC ended in 2016. Today, e-FIRA is auto generated by your AD bank or authorized fintech partner when an inward remittance is reported to EDPMS.

What to do with your e-FIRA

File it per remittance, attach in your tax working papers, share with your CA, use it for GST refund claims, and provide to clients only on request.

What to share in different payment rails, copy paste checklist

SWIFT wire

- ☐ Paid invoice

- ☐ Bank advice

- ☐ e-FIRA within 24 hours

- ☐ Client’s MT103 if tracing is required

ACH, SEPA, or FPS transfer

- ☐ Paid invoice

- ☐ Bank advice or statement line

- ☐ e-FIRA within 24 hours

- ☐ Client’s local payment confirmation if tracing is needed

Card payments or payment links

- ☐ Paid invoice

- ☐ Platform receipt

- ☐ Bank advice after settlement

- ☐ e-FIRA within 24 hours of settlement

Small templates for common scenarios

Template 1, request SWIFT MT103 from client if tracing needed

Hi [Client],

I notice the SWIFT for invoice #XXX has not appeared in my account yet. Could you please share the SWIFT MT103 from your bank, this will help my bank trace the wire. Thanks!

Template 2, send proof of payment bundle to client

Invoice #XXX is settled. Attached, Paid Invoice, Bank Credit Advice. If you need e-FIRA for your records, I can share it within 24 hours.

Template 3, escalate delayed SWIFT with both banks involved

To bank, The UETR for SWIFT [UETR number] sent to account [xxx5678] on [date] has not credited, please trace with intermediary and receiving banks and share an update.

To client, My bank is tracing SWIFT with UETR [number]. Please confirm the gross amount sent and the charges code, OUR, SHA, or BEN, from your bank’s confirmation.

Recommended tools for receiving international payments into India

Shortlist platforms that auto generate e-FIRA, settle quickly, and offer transparent FX. Karbon Business provides multi currency receiving accounts with local rails, quick INR settlement within 24 to 48 hours, e-FIRA within 24 hours, and a flat fee model. Wise Business, Payoneer, PayPal, RazorpayX International, Tazapay, OFX, WorldFirst, and Revolut Business are alternatives with varying fees, speeds, and compliance workflows.

FAQ

Is SWIFT MT103 mandatory as proof for my foreign client or is bank advice enough?

MT103 is not mandatory in most cases, it is primarily a sender side trace document. Once funds have credited, your bank advice plus a paid invoice is sufficient proof for clients. Ask for the client’s MT103 only when the payment is delayed or requires tracing.

Bank advice mila hai, kya yeh international client ke liye sufficient proof hai ya e-FIRA bhi bhejna zaroori hai?

Bank advice is usually sufficient for clients because it confirms the credit with date, amount, and references. e-FIRA is primarily for Indian compliance, ITR and GST, share it with the client only if they specifically request it for their internal records.

FIRC aur e-FIRA mein actual difference kya hai, aur mujhe ITR ke liye kaunsa chahiye?

FIRC was the old physical certificate, e-FIRA is the current digital document issued by AD banks or authorized fintech partners. For ITR, GST refunds, and export benefits, you need e-FIRA for every foreign inward remittance.

Payment SWIFT se bheja gaya tha, paise nahi aaye, main client se exactly kya mangoon?

Ask for their SWIFT MT103 that includes the UETR, amount, value date, and charges code. Share the MT103 with your bank and request a trace. This is the fastest way to locate where the wire is held up, especially if an intermediary bank is involved.

ACH ya SEPA se aaya payment, kya MT103 relevant hai, ya koi aur reference dena chahiye?

For ACH or SEPA, MT103 is not relevant. Provide your bank advice, the local transaction reference or UTR, and the invoice number. That is enough for the client to reconcile and for their bank to confirm the transfer if needed.

e-FIRA kab generate hota hai, aur main usse kaise download karoon without running behind the bank?

e-FIRA is typically generated within 24 hours of credit when the remittance is reported to EDPMS. If you receive via a platform like Karbon Business, you can usually download the e-FIRA directly from the dashboard without manual follow up.

Client ne BEN charges code select kiya tha, amount kam credit hua, main kya share karoon to close reconciliation?

Share your bank advice showing the net credit and reference numbers, and ask the client to confirm the gross amount sent as per their bank’s confirmation. If they provide MT103, field 71A will show BEN, which explains the deductions by intermediary banks.

Upwork, Payoneer, ya Wise se settlement aaya, client ko proof kaise du jo instantly accept ho?

Send a paid invoice plus your bank advice after INR settlement, optionally attach the platform’s payout receipt. Keep your e-FIRA for compliance. Most clients accept this bundle immediately because it clearly shows the final credit.

Karbon Business par account se USD receive karke INR mein settle kiya, kya mujhe alag se bank se FIRC mangwana padega?

No, with Karbon Business e-FIRA is auto generated within about 24 hours for each inward remittance. You can download it from the portal and share with your CA for ITR and GST.

ITR file karte time kaunse documents attach karne chahiye for foreign freelance income?

Maintain and attach your paid invoices, e-FIRA for each remittance, and if required by your CA, the corresponding bank advice PDFs. Keep MT103 only for cases where tracing was required, it is not usually needed for ITR submission itself.

Client before credit proof maang raha hai, main kya bhej sakta hoon jo genuine ho aur unko satisfy kare?

Before credit, you cannot issue your own receipt. Politely request the client’s SWIFT MT103 for wires, or a local payment confirmation with the reference ID for ACH or SEPA. Once funds credit, immediately send bank advice plus your paid invoice.

Monthly retainer chal raha hai, audit friendly proof pack banane ka best process kya hai?

Create a standard folder per month, store four items, paid invoice, bank advice, e-FIRA, and any MT103 if tracing occurred. A platform like Karbon Business helps by auto generating e-FIRA and consolidating references, which simplifies audits and reconciliations.

Closing thoughts and quick action steps

- Issue invoices with clean entity details and correct currency, ensure names match across all documents.

- Right after credit, send bank advice and your paid invoice to the client, keep communication crisp and fast.

- Download e-FIRA within 24 hours and file it for ITR, GST, and export claims.

- Standardize a proof pack per remittance, paid invoice, bank advice, e-FIRA, and MT103 where applicable.

- Maintain email threads with attachments as an audit trail, it saves days during disputes or reviews.

The next time a client asks for remittance proof at an odd hour, you will open your proof pack, share two files, and get back to your weekend.