Key takeaways

- Remitly is great for personal remittances, but it lacks automated e-FIRA, transparent business FX, and B2B workflows for India facing exports, see this breakdown of Remitly alternatives for business payments to India.

- For recurring freelancer and agency payouts, India first platforms such as Karbon Business and Skydo offer 1 percent fees, zero FX markup, fast INR settlement, and auto e-FIRA, read this comparison of a Remitly alternative for business payments.

- Always judge total cost by landed INR, not headline fees, and prefer local rails like ACH, SEPA, and FPS over SWIFT for small to medium invoices, see this cost guide on low cost India payouts.

- RBI and FEMA compliance needs correct export purpose codes and timely e-FIRA, use a platform aligned to RBI and FEMA export service regulations.

- Karbon Business stands out with 1 percent platform fee, mid market FX, ACH, SEPA, FPS, SWIFT, card links, 24 to 48 hour settlement, and auto e-FIRA, details in this Karbon Business guide.

Why Remitly falls short for business payments to India

Remitly shines for fast personal transfers with a friendly interface, yet business use is where friction shows. The onboarding journey assumes a private sender, not a company paying contractors. Limits rarely match project invoices, and support teams are not optimized for India specific B2B compliance.

Purpose codes, and accurate audit trails, are critical under RBI and FEMA. Without automated e-FIRA, Indian freelancers must chase their bank for certificates, which delays filings and creates paperwork overhead. Hidden FX spreads also inflate real costs, turning a seemingly cheap transfer into an expensive one once you compare against mid market rates.

Use Remitly for ad hoc personal remittances, not for recurring B2B payouts that demand e-FIRA and transparent, low all in fees.

For a structured comparison of what to use instead, see this primer on Remitly alternatives for business payments to India and this India focused review of a Remitly alternative for business payments.

Decision framework, choosing the right Remitly alternative

Make your shortlist with a lens on compliance, total cost, transfer methods, speed, and features.

- Compliance alignment: The platform should generate e-FIRA within 24 to 48 hours, map the right export purpose codes, and stay aligned to RBI and FEMA export service regulations.

- Transparent fees: Track platform fee plus FX markup plus any bank charges. The number that matters is the INR that lands in your account, cross check with this guide to transparent India payouts.

- Transfer methods: Prefer ACH, SEPA, and FPS for under ten thousand dollar invoices, use SWIFT only when necessary. Card links are convenient, but pricier and carry chargeback risk.

- Settlement speed: Target 24 to 48 hours to INR credit after claim, not the old 3 to 5 day SWIFT cycle.

- Business features: Invoicing, WhatsApp or dashboard tracking, statements, and the option to hold currency for up to 60 days to manage FX timing are all helpful, see this India centric overview of a business payments alternative.

Use case fit, quick matches:

- Small recurring retainers around one thousand dollars a month, India first platforms with ACH, SEPA, and FPS support.

- Large one off invoices above ten thousand dollars, SWIFT or enterprise wallets, where volume offsets fixed fees.

- Marketplace payouts, Payoneer for Upwork, Amazon, Fiverr integrations.

Crypto is not suitable for export services into India due to compliance risk, missing purpose codes, and audit trail gaps, read this caution in the Remitly alternatives guide.

Side by side overview of major Remitly alternatives

Karbon Business focuses on Indian freelancers and small agencies. A flat 1 percent platform fee plus GST on the fee only, zero FX markup, ACH, SEPA, FPS, SWIFT, and card links supported. INR lands in 24 to 48 hours after claim, and e-FIRA arrives automatically within 24 hours. You get virtual USD, GBP, EUR, and CAD accounts, along with 60 day currency holding and WhatsApp tracking, see this full Karbon Business overview.

Wise Business offers multi currency accounts and mid market FX. Fees typically land around 1.6 to 1.8 percent, and there may be a charge per FIRA download.

Payoneer integrates with marketplaces and offers broad receiving account coverage. Receiving fees can appear low, but FX spreads and withdrawal fees often raise the all in percentage.

PayPal is universal, but expensive. Expect a higher take rate and chargeback exposure, with monthly consolidated FIRA only.

Airwallex, OFX, and direct SWIFT via banks handle large B2B transfers, but with slower settlement and higher FX spreads.

Skydo is another India focused option with 1 percent inward fees, instant FIRA, and local rails, see this Skydo comparison.

India first platforms consistently win on lower all in fees, faster e-FIRA, and support teams fluent in RBI rules.

Cost clarity, fees and landed INR examples

Total cost equals platform fee plus FX markup plus bank charges, measured against the INR that hits your account. Always compare your offered rate to mid market.

- $2,000 invoice, mid market ₹83 per USD

Karbon Business, about 1 percent, landed around ₹164,940, see the math in this Karbon fee example.

Wise Business, about 1.6 to 1.8 percent plus any FIRA charge, landed around ₹164,566.

Payoneer, typical 1 percent receive plus FX spread and withdrawal fees, landed around ₹164,000.

PayPal, 4.4 percent plus 3 to 4 percent FX, landed around ₹163,400.

Bank SWIFT, FX markup plus correspondent fees, often lands lower than local rails.

Scale to ten thousand dollars and the gap widens. Local rails via India first platforms often save 50 to 70 percent versus traditional SWIFT on small to mid sized invoices, cross check with this cost comparison.

Transfer methods explained, ACH, SEPA, FPS, SWIFT, and card links

- ACH: U.S. domestic clearing, 1 to 2 business days, very low sender cost, ideal for monthly retainers.

- SEPA: Euro area transfers, typically one business day, low cost and predictable.

- FPS: U.K. instant payments, near instant funding to the platform.

- SWIFT: Global reach, 2 to 5 days, intermediary deductions, use for large invoices only if needed.

- Card payment links: Instant authorization, higher network fees, and chargeback risk, useful for urgent or one off projects, more context in this transfer methods guide.

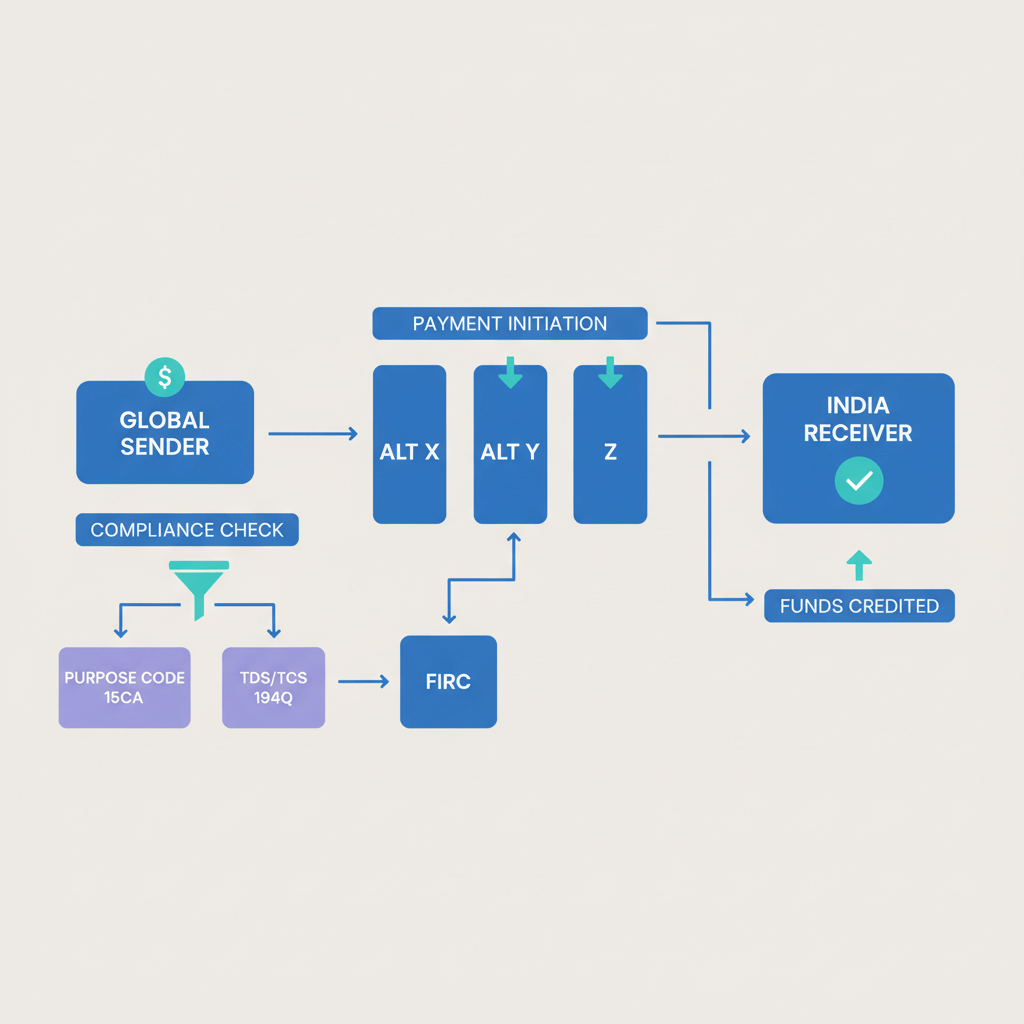

Virtual accounts route the client’s local payment to your balance, then you claim and convert to INR within 24 to 48 hours, see an India focused explainer in this virtual accounts guide.

Deep dive, Karbon Business as the top Remitly alternative

Compliance: Auto e-FIRA within 24 hours, correct purpose codes, RBI and FEMA aligned.

Fees: Flat 1 percent on the platform, GST on the fee only, zero FX markup on mid market rates.

Transfer methods: ACH, SEPA, FPS, SWIFT, and card links for comprehensive coverage.

Settlement: 24 to 48 hours after claim to INR credit.

Operations: Invoicing tools, WhatsApp tracking, statements, and 60 day currency holding. Learn more in this Karbon Business deep dive and this India focused comparison overview.

How to set up and switch from Remitly to a business alternative

For Indian freelancers receiving payments

- Step 1, Sign up and KYC: Keep PAN, masked Aadhaar, three months of bank statements, and a live work profile ready. Typical verification takes 2 to 4 working days.

- Step 2, Activate accounts: Enable USD, GBP, EUR, and CAD receiving accounts, set up card links if desired.

- Step 3, Invoice and share details: Generate or upload your invoice, share local ACH, IBAN, or sort code details, or send a payment link.

- Step 4, Client pays: They pay domestically in their currency via ACH, SEPA, FPS, or card.

- Step 5, Claim and settle: Claim on the dashboard, INR lands in 24 to 48 hours, download e-FIRA for your records, see this step by step in the Karbon setup guide.

Pro tip: If you expect the rupee to strengthen, hold foreign currency for up to 60 days before converting.

For global clients paying Indian freelancers

- Step 1, Pick the rail: Use ACH, SEPA, or FPS for recurring payments under ten thousand dollars, use SWIFT for large, infrequent invoices.

- Step 2, Pay with exact details: Match account name, reference, and invoice ID, and include purpose code if requested.

- Step 3, Confirm receipt: Ask the freelancer to confirm INR credit and e-FIRA availability for your AP records, see the checklist in this business payments guide.

Pilot one invoice end to end, measure time to INR, and compare the landed INR against your old method before fully switching.

India specific compliance, e-FIRA, RBI rules, and tax documentation

e-FIRA is the electronic Foreign Inward Remittance Advice, a must have proof of foreign income for ITR and GST where applicable. Read the practical walkthrough in this e-FIRA and FIRC documents guide.

Under RBI and FEMA, you need the right export purpose codes and complete documentation. Automated e-FIRA in 24 hours removes bank branch runs and long waits, see policy context in this compliance oriented comparison and this India focused remittance alternative guide.

- Use invoice templates that include scope, currency, and due dates.

- Store invoices, e-FIRA, and payment confirmations for each transaction.

- Double check purpose codes to prevent holds or penalties.

Real world scenarios, how businesses save

Scenario 1, U.S. SaaS paying ₹ developer $3,000 monthly: ACH via Karbon Business costs about 1 percent, INR in 24 hours post claim, versus 3 to 5 day SWIFT and higher combined costs.

Scenario 2, U.K. studio paying £1,200 per project: FPS to virtual GBP account is instant to the platform, INR in up to 48 hours, e-FIRA auto generated.

Scenario 3, EU consultancy paying €25,000 milestone: SEPA delivers predictable cost and speed, with less leakage than SWIFT intermediaries, more examples in this India payouts case study.

Quick comparison checklist, what to look for

- Auto e-FIRA within 24 to 48 hours, confirmed by downloads.

- All in fees at or near 1 percent, zero FX markup on mid market.

- Local rails for your client’s country, ACH, SEPA, FPS, plus SWIFT when necessary.

- INR settlement in 24 to 48 hours after claim.

- Ability to hold currency up to 60 days for FX timing.

- Support that understands India specific RBI and FEMA rules, more pointers in this platform checklist.

Next steps, test your Remitly alternative

Start with a small invoice, five hundred to one thousand dollars, and measure end to end time, landed INR, and e-FIRA accuracy. Compare against your old method. If results are better, migrate recurring clients and update invoices with your new local account details or payment links. For onboarding help and deep compliance resources, visit Karbon Business.

Switching to a business focused, India ready platform reduces cost, speeds up cash flow, and removes compliance headaches, so you can focus on delivery instead of chasing banks.

FAQ

Which platform is best for Indian freelancers to receive international client payments with low fees and proper e-FIRA?

For most freelancers, Karbon Business is a strong pick because it charges a flat 1 percent platform fee, uses mid market FX with zero markup, and auto generates e-FIRA within 24 hours. Skydo is similar. Both are built for Indian export services, so compliance is baked in.

How do I get e-FIRA automatically for my USD payments without visiting my bank branch?

Use an India focused platform that integrates e-FIRA generation into the payout flow. With Karbon Business, every payment produces a downloadable e-FIRA in about 24 hours, which you can hand over to your CA for ITR or GST.

ACH vs SWIFT, which is cheaper and faster for paying Indian freelancers between $1,000 and $10,000?

ACH is usually cheaper and faster for U.S. clients because it is a domestic rail for them, and on platforms like Karbon Business the INR settles in 24 to 48 hours after you claim. SWIFT adds intermediary bank fees and can take 3 to 5 days.

Can I accept card payments from clients abroad without losing a lot in fees?

Yes, but plan for card network charges. Karbon Business lets you share a payment link at the same 1 percent platform fee, while card networks add their own processing cost. Use card links for urgent jobs, and include pricing that covers the extra cost.

What documents should I keep for taxes when I receive international payments in India?

Keep the e-FIRA for each transfer, the invoice you issued, and a payment confirmation or statement. Platforms like Karbon Business centralize these so you can download a clean audit trail for your CA or during an assessment.

How do I explain to my foreign client that paying me via ACH or SEPA is easier than SWIFT?

Tell them it is a local transfer for them, so it feels like paying a domestic vendor, it is cheaper, and it clears faster. With Karbon Business, they get local account details in USD, GBP, or EUR, and you receive INR in 24 to 48 hours with e-FIRA.

Is Remitly good enough for B2B payments to India or should I switch?

Remitly is optimized for personal remittances, not recurring business payouts. If you need clear FX, higher limits, and automated e-FIRA, switch to a business focused option like Karbon Business or Skydo.

What is the typical total cost I should target for international freelancer payments to India?

Target about 1 to 1.8 percent all in for small to medium invoices using local rails. With Karbon Business, many freelancers land near 1 percent plus GST on the fee only, since FX markup is zero.

Can I hold USD or EUR for some time and convert later if INR improves?

Yes, platforms like Karbon Business let you hold foreign currency for up to 60 days. This gives you flexibility to convert when the rupee is stronger, increasing landed INR.

Will I get support for RBI purpose codes and export service compliance if a payment gets flagged?

With India first platforms, support teams are trained on purpose codes and RBI workflows. Karbon Business provides guidance and auto populates purpose code details, reducing the chance of holds and rework.

How fast can I start after signup, what KYC is needed for Indian freelancers?

KYC typically completes in 2 to 4 working days. You will need PAN, masked Aadhaar, three months of bank statements, and a public work profile like LinkedIn or Upwork. After activation, you can share local account details immediately.

Can my client pay from the UK or EU without extra bank charges on their side?

Yes, with FPS in the UK and SEPA in the EU, your client pays domestically. On Karbon Business, that local transfer lands to your virtual account and you convert to INR, avoiding unpredictable SWIFT deductions.