Key takeaways

- Nostro, vostro, and loro describe the same cross-border balances from different viewpoints, nostro is “ours abroad,” vostro is “yours here,” loro is “theirs via a third bank.”

- For freelancers, these accounts affect speed, fees, and where payments get stuck. Fewer intermediaries usually means faster, cheaper transfers.

- Share complete beneficiary and intermediary details, ask clients to choose OUR charges, and request the MT103 for any delayed SWIFT payment.

- Prefer local rails like ACH, SEPA, and Faster Payments for frequent invoices, they typically avoid long correspondent chains.

- Automate compliance with e-FIRA, keep invoices and remittance proofs organized, reduce back and forth with clients.

- Platforms like Karbon Business give you local account details, quick INR settlements, and e-FIRA within 24 hours, removing complexity.

Why these banking terms matter for Indian freelancers

Your US client writes, “Please share your nostro details for the wire,” and suddenly your payment waits in limbo. These terms sound like jargon, yet they determine how quickly money lands in your account, how much gets deducted, and where delays occur. Understand them once, and you will prevent confusion, reduce fees, and answer client queries with confidence.

Big idea: Nostro and vostro are the same balance seen from two sides, loro adds a third bank when there is no direct relationship. Fewer hops, fewer surprises.

What is a Nostro Account?

A nostro account is a bank’s account in a foreign currency, held with a bank abroad. Think of SBI India keeping USD at a US bank. From SBI’s perspective, that USD balance is its nostro, meaning “ours.”

Banks use nostro accounts to settle cross-border transactions quickly, without forcing immediate conversions or long chains of intermediaries. For you, the freelancer, incoming USD often first lands in your bank’s USD nostro abroad, then gets converted and credited in INR.

For more on the mechanics, see the ICAI reference on foreign exchange operations.

What is a Vostro Account?

A vostro account is the same balance, viewed by the foreign bank servicing it. Using the earlier example, the US bank records SBI’s USD funds as a vostro, meaning “yours.”

This perspective lets the local bank handle transfers on behalf of the foreign bank, using domestic rails. The result for you is faster processing when local systems like ACH feed into your bank’s overseas balance. See also the Wikipedia overview of nostro and vostro.

What is a Loro Account?

A loro account is “theirs,” used when two banks lack a direct relationship. If your Indian bank cannot directly hold EUR with your client’s European bank, it may route via a third bank that does. From your bank’s view, that third bank’s account is the loro. This adds complexity, sometimes extra fees, and often a little delay. A helpful primer is this comprehensive guide to nostro, mirror-nostro, vostro, and loro.

Nostro vs Vostro vs Loro at a glance

- Perspective: Nostro is “ours abroad,” vostro is “yours here,” loro is “theirs through a third bank.”

- Ownership: Nostro belongs to the domestic bank abroad, vostro is recorded by the foreign bank locally, loro references a third bank’s account used indirectly.

- Use case: Nostro enables direct settlements, vostro supports local servicing for a foreign bank, loro connects banks without direct relationships.

- Payment impact: Direct nostro-vostro links are quicker, loro chains can add time and fees.

Think of it like a conversation, “my phone,” that is nostro, “your phone,” that is vostro, “their phone,” that is loro.

Examples that make it simple

- Nostro example: SBI India keeps USD at a US bank. That USD balance is SBI’s nostro and funds your incoming USD before INR credit.

- Vostro example: The same USD balance appears in the US bank’s records as SBI’s vostro, serviced locally by the US bank.

- Loro example: To receive EUR when there is no direct link, SBI routes via a UK bank that has an account with the European bank. From SBI’s view, the UK bank’s account is the loro.

For a quick refresher, see this Razorpay overview of nostro, vostro, and loro.

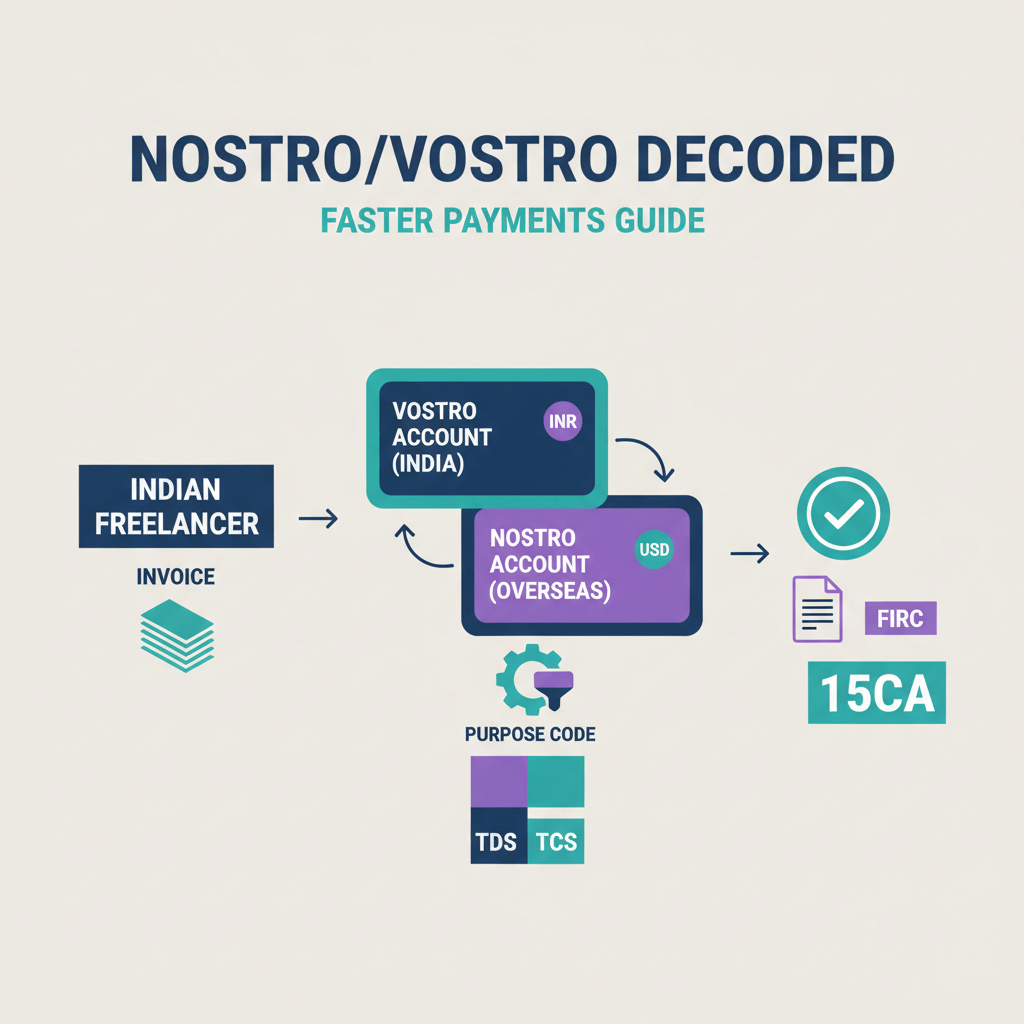

How money actually moves, a freelancer’s payment map

Scenario: Your US client pays you around USD 600 via SWIFT to your Indian bank.

- The client’s bank sends a USD wire through SWIFT to your bank, say HDFC.

- Funds arrive in HDFC’s USD nostro at its US correspondent, for example, JPMorgan.

- JPMorgan updates the vostro balance it maintains for HDFC, from its viewpoint, it is “your” money.

- HDFC is notified, converts USD to INR at its rate, and credits you.

Where delays happen: Compliance checks, time zones, and any loro intermediaries. Where fees hit: Correspondent lifting fees, FX spread, and charge type, OUR versus SHA versus BEN. A deeper background explainer is here, Faisal Khan’s payments wiki.

Tip: If funds do not show up in 3 to 5 business days, ask your client for the MT103, this is the official SWIFT trace that lists every hop.

What this means for freelancers in practice

When a client asks for “nostro details,” they want the complete routing path that ensures their payment reaches your bank quickly, with no ambiguity.

- Share complete beneficiary info: Full name as per bank, account number, PAN.

- Provide full bank details: Bank name, branch address, SWIFT or BIC, IFSC for domestic linkage.

- Include intermediary details: If your bank uses a correspondent, add the intermediary bank’s name and code.

- Match rails to currency: USD via ACH or SWIFT, EUR via SEPA, GBP via Faster Payments or CHAPS.

- Agree fees upfront: Ask for OUR, or else SHA will split, BEN reduces what you receive.

If a payment stalls: Request MT103 from your client, share it with your bank’s remittance desk, and follow up within 24 to 48 hours.

How to choose the right payment method, step by step

- Frequent payments from US, EU, UK, Canada: Prefer local rails like ACH, SEPA, Faster Payments, fewer correspondent hops, predictable costs.

- Local currency account details: Virtual USD or EUR accounts accept domestic transfers, avoiding international wire charges entirely.

- Large B2B wires: Confirm OUR charges, share the full correspondent chain, request the MT103 immediately after sending, be mindful of cutoff times.

- Speed versus cost: SWIFT in 2 to 5 days with fees, ACH in 3 to 5 days, often low cost, SEPA in 1 to 2 days, often minimal cost.

- Currency holding: When allowed, hold USD or EUR briefly if rates are volatile, then convert when favorable.

Payment platforms that simplify everything

Karbon Business gives you virtual USD, GBP, EUR, and CAD accounts with local routing. Clients pay via ACH, SEPA, or Faster Payments as domestic transfers. INR settles in 24 to 48 hours at mid market rates, zero markup, with a flat 1 percent platform fee. e-FIRA is generated automatically within 24 hours, you can hold currencies up to 60 days, and you get payment links with WhatsApp tracking.

Wise Business offers multi currency accounts with transparent pricing, useful for frequent smaller invoices.

Payoneer provides receiving accounts in major currencies, popular for marketplace payouts, fees usually around 1 to 2 percent.

PayPal is quick and convenient, fees are higher, better for small, urgent settlements.

RazorpayX International supports foreign receipts with automated compliance and Indian integrations.

All of these manage nostro and vostro relationships behind the scenes, you just share simple local details.

Invoice and payment instruction templates

Invoice payment details section

Beneficiary Name: [Your Full Name or Firm Name]

PAN: [Your PAN Number]

Account Number / IBAN: [Complete Account Number]

Bank Name: [Full Bank Name and Branch]

SWIFT / BIC Code: [8 or 11 Character Code]

Routing Code: [ABA for US, Sort Code for UK, or IFSC for India]

Intermediary Bank: [If required, for example, JPMorgan Chase, ABA 021000021]

Payment Reference: Invoice #123

Fee Arrangement: OUR, sender covers all fees

Client email for payment instructions

Subject: Payment Instructions for Invoice #123

Hi [Client Name],

Thank you for approving the invoice. Please use these details for USD wire transfer:

Beneficiary: [Your Name]

Bank: [Your Indian Bank Name], SWIFT: [BIC Code]

Nostro / Intermediary: [US Correspondent Bank Details]

Amount: USD 600.00

Reference: Invoice #123

Charges: OUR, please ensure you cover all fees so I receive the full amount

Please confirm payment with the MT103 SWIFT trace for my records. Typical settlement takes 3 to 5 business days.

Thank you!

Pre payment checklist

Confirm your bank’s latest correspondent details, verify cutoff times, and agree OUR or SHA in writing.

If payment is delayed

Ask for the MT103, check bank notifications, contact your bank’s remittance team with the reference, verify intermediary references.

FAQ

Do I, as a freelancer, need to open a nostro account to receive USD or EUR?

No, nostro accounts are bank to bank. You do not open one yourself. Your Indian bank, or a platform like Karbon Business, maintains the required correspondent relationships and gives you simple details to share with clients.

Client is asking for “nostro details,” what exactly should I send?

Send your beneficiary name as per bank records, account number, bank name and address, SWIFT or BIC, IFSC if needed, plus the intermediary or correspondent bank details your bank recommends for that currency. If you use Karbon Business, share the local account details they provide for ACH, SEPA, or Faster Payments.

What is the difference between vostro and a normal multi currency account I can open?

Vostro is a bank’s internal record of another bank’s funds, it is not a customer product. A multi currency account is customer facing, you can open it to receive and hold multiple currencies. Karbon Business offers virtual accounts with local details, which function like domestic receiving accounts for your clients.

Why did my SWIFT payment arrive short, who deducted the fees?

Intermediary banks often deduct lifting fees during processing. If your client chose BEN or SHA, you bear some, or all, deductions. Ask the client to use OUR so you receive the full invoice amount. Platforms that use local rails, for example Karbon Business for ACH or SEPA, avoid many of these deductions.

How do I trace a missing SWIFT wire from my US client?

Request the MT103 from your client. It lists sender, receiver, intermediaries, value date, and references. Share it with your bank’s remittance desk to locate the funds, expect a response in 2 to 5 business days. For background on third bank routing, see this note on loro accounts in foreign transactions.

Payment is routed via a third bank, is that normal and does it add delay?

Yes, when banks lack direct relationships, payments use a third correspondent, the loro path. It is normal, but each extra hop can add checks, fees, and a day of delay. Where possible, accept payments via local rails through providers like Karbon Business to reduce intermediaries.

Which is cheaper for me in practice, SWIFT wire or local rails like ACH or SEPA?

Local rails are usually cheaper and more predictable. ACH and SEPA fees are low, settlement times are short. SWIFT can be fast, but fees vary, and intermediaries may deduct charges. With Karbon Business, your clients pay locally, then INR lands to you quickly with transparent pricing.

My client’s bank wants intermediary bank info for USD, where do I find it?

Your bank’s forex or remittance page lists recommended correspondents per currency. Ask your branch or support team for the latest details. If you are on Karbon Business, the app shows you the exact local details, removing the need for complex intermediary instructions.

How can I ensure I get the full invoice amount in INR?

Ask the client to select OUR charges, include your invoice number as reference, and share the precise beneficiary and intermediary details. If your platform provides local accounts, prefer them. Karbon Business converts at mid market rates with a flat fee, helping you predict the final INR credit.

Can I hold USD or EUR for a while, then convert when the rate improves?

Yes, within regulatory limits. Some platforms allow short holding periods for hedging. Karbon Business lets you hold supported currencies up to 60 days, then convert to INR when you prefer, keeping documentation compliant with e-FIRA.

What documents do I need for taxes and compliance on foreign receipts?

Keep e-FIRA or FIRA for each inward remittance, the bank statement credit, and your invoice. These support income tax filings, GST, and export documentation. Karbon Business auto generates e-FIRA within 24 hours, saving you follow ups.

Is PayPal or Payoneer better for India based freelancers who get small, frequent payments?

PayPal is fast and convenient for small amounts, but fees are higher. Payoneer is popular for marketplace payouts with moderate fees. For consistent client work, local rails via virtual accounts often cost less, for example through Karbon Business, Wise Business, or RazorpayX International.

India specific compliance and documentation

Every foreign receipt needs proper records for tax, GST, and export tracking. e-FIRA, or FIRA, is your proof of inward remittance, showing sender details, purpose code, and the applied exchange rate. Most banks now issue e-FIRA, replacing manual FIRC in many cases.

You will use e-FIRA for income tax proofs, GST claims when applicable, export obligation closure, and transfer pricing support for entities. Keep PDFs organized by financial year, along with invoices and bank credits. With Karbon Business, e-FIRA is generated automatically within 24 hours of settlement, which reduces manual follow ups and errors.

Quick reference guide

Nostro: Ours abroad, used for direct foreign settlements.

Vostro: Yours here, local servicing of a foreign bank’s funds.

Loro: Theirs via a third bank, used when there is no direct relationship.

Decision flow

Small, frequent invoices, prefer local rails via virtual accounts. Large, occasional invoices, use SWIFT with OUR charges and full correspondent details. Need compliance automation, pick providers that issue e-FIRA quickly. Watching exchange rates, use short term currency holding when permitted.

Always share with clients

Accurate beneficiary details, full bank and SWIFT or BIC, intermediary information when required, invoice reference, fee arrangement, and expected settlement times.

Where Karbon Business simplifies the entire process

Traditional banking introduces correspondent chains, variable fees, and confusing terminology. Karbon Business removes most of this. Clients pay you locally, ACH in the US, SEPA in the EU, Faster Payments in the UK. Funds settle quickly to INR, at mid market rates, with a flat platform fee.

Compliance is automatic, e-FIRA arrives within 24 hours. Your dashboard and WhatsApp updates keep you informed, you get payment links for faster collections, and you avoid multi portal juggling. This is ideal for freelancers and small agencies that want reliable, predictable international receipts.

Final thoughts

Nostro, vostro, and loro are the invisible rails under every cross-border payment. Learn the basics once, and you will reduce delays, predict fees, and handle client requests like a pro. Your bank’s nostro is their money abroad, the foreign bank’s vostro is the same balance from the other side, and a loro path appears when a third bank bridges a gap.

Whenever possible, pick local rails that bypass long chains, share complete instructions, and request OUR charges. Use MT103 to trace anything missing, and keep e-FIRA alongside your invoices. Platforms that abstract the complexity, like Karbon Business, help you get paid faster, keep more of what you earn, and stay fully compliant.