Key takeaways

- Know the difference between cancellation, recall, and reversal, cancellation stops a payment before it credits, recall requests funds back after credit, reversal is the accounting entry when the return succeeds.

- Always track the payment via the UETR, and confirm status before asking your bank to act.

- Use MT192 for fast cancellation in the pre credit window, use MT199 for recall after credit, expect lower success rates and longer timelines for recalls.

- Fees and forex shifts are real, plan for $75 to $200 in bank charges, and 1 to 3 percent potential currency movement between send and return.

- For Indian freelancers, document everything, e-FIRA, invoices, reversal entries, and update tax records properly.

- Prevent errors with test payments, clear contracts, and local rails via platforms like Karbon Business.

- Use the ready email templates to contact banks quickly, complete data improves speed and success.

What Is SWIFT and How Do International Transfers Work

SWIFT powers most international bank transfers through a network that connects over 11,000 financial institutions worldwide. When your overseas client sends you money, they are typically using a SWIFT MT103 customer credit transfer.

Here is the journey your payment takes. Your client's bank, the ordering bank, initiates the transfer. The payment then moves through one or more intermediary banks that act as correspondents between countries and currencies. Finally, it reaches the beneficiary bank, your bank in India, which credits your account.

Each institution in this chain adds processing time, fees, and potential points of failure. That is why a single international wire can take three to five business days and cost anywhere from $15 to $50 in bank charges.

Modern SWIFT transfers include a UETR, a tracking code similar to a courier tracking number. Some banks offer SWIFT gpi, a real time tracking service that shows exactly where your money is in the chain, whether it is pending at an intermediary, credited to your account, or fully settled.

Before you attempt any cancellation or recall, always check the payment status first. You cannot cancel what is already been credited, and you waste precious hours asking for recalls on payments still in transit. The status determines your next move, so track the UETR through your bank or ask your client to check with theirs, see can SWIFT transfer be reversed.

International Payment Reversal vs Recall: Core Definitions That Matter

The terms reversal, recall, and cancellation get thrown around interchangeably, but they mean very different things in SWIFT banking. Using the wrong term with your bank wastes time and confuses the process.

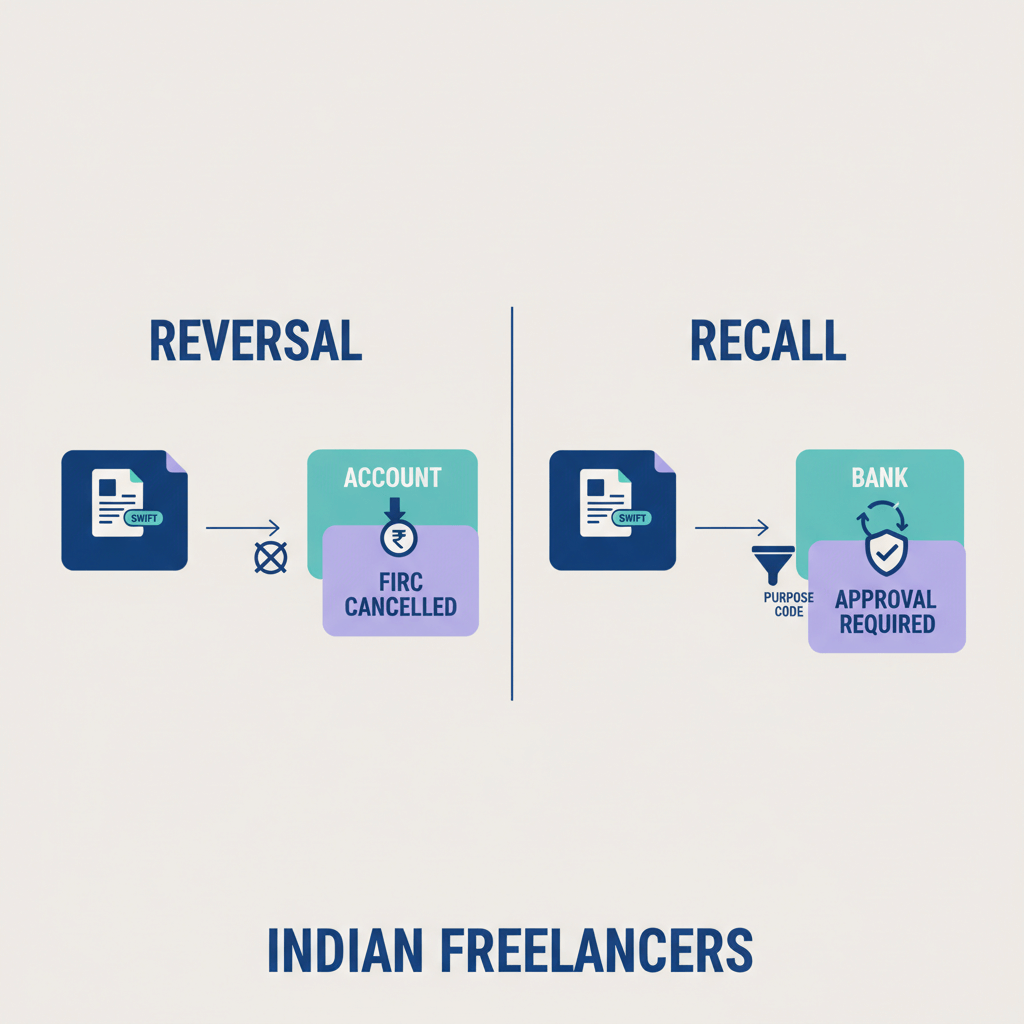

Cancellation means stopping a payment before the beneficiary bank credits the recipient's account. Your client's bank sends an MT192 Request for Cancellation message down the SWIFT chain. If the payment is still in processing, somewhere between banks and not yet posted to your account, the beneficiary bank can halt it and return the funds.

Cancellation works only in that narrow pre credit window. Speed is everything. The MT192 needs to reach the beneficiary bank before they post the credit, which could be minutes or hours depending on the institution. Success rates are decent, around 70 to 90 percent, if you act immediately.

Recall refers to requesting the return of funds after the beneficiary bank has already credited the recipient's account. This uses an MT199 free format SWIFT message, essentially a formal request asking the recipient to voluntarily send the money back. Notice that word, voluntary. Once money sits in your account, the bank cannot simply yank it back without your consent. The recall process is a negotiation, not a reversal button.

Recall timelines stretch into weeks. Success depends entirely on whether the recipient cooperates, whether the funds are still in the account, and whether all parties can agree on fees and exchange rates for the return transfer. There is no guarantee whatsoever.

Reversal is what banks call the ledger outcome when a recall or cancellation succeeds. You will see a reversal entry on your statement, a debit line referencing the original payment. It is not a separate SWIFT message type but the accounting result after funds move back.

So when someone asks about international payment reversal vs recall, the distinction is this, cancellation, MT192, attempts to stop uncredited payments quickly, recall, MT199, negotiates the return of already credited funds, and reversal is the bank statement entry that appears after a successful return.

When to Use Cancellation, Recall, or Accept the Reversal

Choosing the right action depends entirely on timing and payment status. Here is your decision tree.

Step one: Check the payment status using the UETR or SWIFT gpi tracker. If the payment is still pending, sitting at an intermediary bank, not yet credited to the final account, go straight to cancellation. Contact the ordering bank immediately and request an MT192 cancellation. Provide the original MT103 reference number, the UETR, the exact amount and currency, full beneficiary details, and a clear reason such as duplicate payment, wrong account number, or suspected fraud. Emphasize urgency.

Your bank sends the MT192 message down the SWIFT chain. Intermediary banks and the beneficiary bank respond, ideally with an MT196 acknowledgment or confirmation that the payment has been stopped. If successful, the funds return to the sender minus bank fees.

Step two: If the payment is already credited, cancellation is off the table. Now you need a recall. Email your bank with MT103 and UETR references, reason for the recall, and supporting evidence, then request MT199 recall. The beneficiary bank contacts the account holder, checks availability of funds, and asks for consent. If everyone cooperates, the beneficiary bank processes a new outbound credit, the return appears as a reversal on statements, for background see can a wire transfer be reversed.

Step three: If funds have already been debited or offset on your statement, the reversal is complete. Reconcile your records and move on.

Step four: If both cancellation and recall fail, SWIFT offers no guaranteed remedy. You are left to negotiate directly, possibly involve legal contracts or disputes. The international payment system does not come with an undo button beyond these narrow windows.

How to Initiate a SWIFT Cancellation Using MT192

Use MT192 when you discover an error quickly, ideally within hours, and the payment has not yet been credited to the recipient's account.

Contact your ordering bank immediately. Provide MT103, UETR, exact amount and currency, full beneficiary details, a clear reason for cancellation, and a timestamp showing urgency. Your bank's SWIFT department sends MT192 through the chain, the beneficiary bank can stop the payment and confirm via MT196 if it has not posted.

Expect fees at each bank, and a one to three business day timeline if you act fast. Real example, a Mumbai developer's client sent $5,000 with a wrong digit, caught within six hours, MT192 stopped the payment, funds returned minus $40 in fees within three days, see can SWIFT transfer be reversed.

How to Initiate a SWIFT Recall Using MT199

Use MT199 when the payment has been credited, or when MT192 fails. The process requires beneficiary cooperation.

Provide MT103 and UETR, detailed reason and proof, and request your bank to send an MT199 recall message. The beneficiary bank reviews, contacts the account holder, and seeks consent. If the recipient agrees, the bank debits the account and returns funds, which appears as a reversal. Fees and forex changes may reduce what the sender ultimately receives. Recalls often take two to four weeks, sometimes longer. The lesson, MT199 recall is a request, not a command, see can SWIFT transfer be reversed.

What a Payment Reversal Looks Like on Your Bank Statement

When a recall or cancellation succeeds, your bank processes the funds return as a reversal on your ledger, not a separate SWIFT instruction.

On your statement, you will see a debit entry referencing the original credit, for example, Reversal of SWIFT credit ref MT103 [number]. Amounts match the original credit, fees may be deducted separately. If intermediaries were involved, the return can take additional days. Track via UETR or ask for status updates on the outbound return payment.

Mind currency implications. If dollars were converted to rupees, a later reversal means you need INR to cover the debit. Exchange rate moves can create loss. Reconcile in your accounting, and update e-FIRA entries and export records properly, more on this in can SWIFT transfer be reversed.

Indian Freelancer Scenarios: What to Do When You are the Beneficiary

Scenario one, a client requests a recall due to mistake. Verify the sender, confirm details, and remember, you are not obligated to return credited funds unless there is fraud or legal cause. If valid, cooperate and adjust records.

Scenario two, client sent funds to the wrong account number, not yours. Advise immediate MT192 or MT199 via their bank. Do not issue a new invoice until the mistaken payment is resolved, avoid double payments and fresh recalls.

Scenario three, you suspect a scam. Watch for red flags, third party refund accounts, vague reasons, urgent tone. Do not comply, contact your bank's fraud team, and report. If the original payment was fraudulent, the bank may reverse under AML rules, keeping a clear paper trail protects you, see can SWIFT transfer be reversed.

Professional courtesy matters, but consent is king. A recall is a request, your agreement drives the outcome.

E-FIRA, RBI, and Tax Implications of Payment Reversals

When you receive an international payment, your bank issues an e-FIRA within 24 hours. If the payment later reverses, the e-FIRA does not disappear. Track both events in your records, adjust income with your chartered accountant, and maintain documentation, invoice, e-FIRA, reversal entry, and correspondence. If the payment is re sent correctly, a new e-FIRA is issued. For more, see can SWIFT transfer be reversed.

Data and Documentation Checklist for Banks

Complete information speeds up bank action. Gather, UETR, MT103 reference, exact amount and currency, value date, full beneficiary details, intermediaries if known, clear reason, supporting evidence, and your contact info with urgency. Use descriptive subject lines, for example, URGENT, MT192 Cancellation for UETR [code], or MT199 Recall Request for MT103 [reference]. Banks process hundreds of requests daily, clarity wins, see can SWIFT transfer be reversed.

Timeframes, Fees, and Success Rates for Reversal and Recall

Cancellation, MT192, act within hours, resolution in one to three business days, success rate 70 to 90 percent pre credit.

Recall, MT199, two to four weeks typical, success often below 50 percent, depends on beneficiary consent and fund availability.

Fees, cancellation costs about $75 to $120 across banks, recall can total $100 to $200 because the return is a new payment.

Forex risk, 1 to 3 percent movement is common over days or weeks, adding exposure on larger transfers. No part of the process is guaranteed post credit. Plan for failure scenarios, and protect with contracts and milestones, reference, can you reverse international bank transfers.

How to Prevent the Need for SWIFT Reversals in the First Place

Validate beneficiary details obsessively, double and triple check every digit, verify SWIFT codes.

Send a test payment, confirm arrival before the full amount.

Prefer local payment rails, ACH, SEPA, GBP Faster Payments, to avoid multi bank complexity. Platforms like Karbon Business provide virtual USD, GBP, EUR, and CAD accounts so US clients can pay via domestic ACH, funds settle in one to two business days, convert to INR at mid market rates, and e-FIRA is generated automatically.

Track with UETR or gpi, use real time visibility, avoid premature recall requests.

Avoid rush payments, build buffer time in contracts.

Establish clear payment terms, specify currency, account details, method, timeline, and fee responsibilities. For more prevention tips, see can SWIFT transfer be reversed.

Why Karbon Business Makes Cross Border Payment Issues Easier to Handle

Local rails cut out correspondent chains. A US client paying via ACH to your Karbon Business USD account settles in one to two business days with minimal fees, disputes are resolved within a single system. If something goes wrong, ACH has defined return windows and faster resolution than MT199 recalls. You control when to convert to INR, hold up to 60 days, settle in 24 to 48 hours, and get e-FIRA automatically. Support via WhatsApp, email, or phone coordinates status tracking and re sends, with transparent one percent platform fee, no hidden forex markup, no surprise correspondent fees. Learn more in can SWIFT transfer be reversed.

Copy and Paste Email Templates for MT192 and MT199 Requests

MT192 Cancellation Request Email Template

Subject, URGENT MT192 Cancellation Request – MT103 [Reference Number] UETR [UETR Code]

Dear [Bank Name] SWIFT Operations Team,

I request an immediate MT192 cancellation for the following payment,

Amount, [Amount] [Currency]

Beneficiary Name, [Full Name as Registered]

Beneficiary Account, [Account Number or IBAN]

Beneficiary Bank, [Bank Name, SWIFT/BIC Code]

MT103 Reference, [Reference Number]

UETR, [Unique End to End Transaction Reference]

Value Date, [Date]

Reason for Cancellation, [Duplicate payment, Incorrect account number, Wrong amount, Suspected fraud, AML concern]

Evidence, [Attached, email confirmation of error, duplicate payment receipt, contract showing correct details]

This payment has not yet been credited to the beneficiary account. Please send MT192 immediately to halt processing and return funds.

Contact me at [Your Phone] or [Your Email]. This is time sensitive, please act within the hour if possible.

Thank you,

[Your Name]

[Your Account Number]

MT199 Recall Request Email Template

Subject, MT199 Recall Request – MT103 [Reference Number] UETR [UETR Code]

Dear [Bank Name] International Payments Team,

I request an MT199 recall for the following credited payment,

Amount, [Amount] [Currency]

Beneficiary Name, [Full Name]

Beneficiary Account, [Account Number or IBAN]

Beneficiary Bank, [Bank Name, SWIFT/BIC Code]

MT103 Reference, [Reference Number]

UETR, [UETR Code]

Original Payment Date, [Date]

Reason for Recall, [Duplicate payment, Payment sent in error, Fraudulent transaction, Contract dispute]

Supporting Evidence, [Attached, duplicate payment confirmations, email correspondence, fraud report, contract]

The payment has been credited to the beneficiary account. Please send an MT199 free format message to the beneficiary bank seeking voluntary return of these funds.

Please confirm receipt and provide an estimated timeline. I can be reached at [Your Phone] or [Your Email].

Thank you,

[Your Name]

[Your Account Number]

Beneficiary Consent to Return Funds Template

Subject, Consent to Return Payment – UETR [UETR Code]

Dear [Your Bank Name],

I consent to the return of the following payment received in my account,

Amount, [Amount] [Currency]

Original Payment Date, [Date]

MT103 Reference, [Reference Number]

UETR, [UETR Code]

Sender, [Sender Name, Bank]

Reason, [Duplicate payment received, Payment sent in error, As requested by sender]

Please process the return to the original sender via [SWIFT, ACH, Local method]. Deduct applicable fees, and share confirmation and fee breakdown.

Preferred return date, [Date, or As soon as possible]

Contact me at [Your Phone] or [Your Email] for any further authorization.

Thank you,

[Your Name]

[Your Account Number]

FAQ

SWIFT recall ka success guarantee hota hai kya?

Nahi, MT199 recall beneficiary ki consent par depend karta hai, agar paise account me available nahi hai, ya recipient refuse karta hai, to recall fail ho jata hai. Pre credit MT192 cancellation ke chance zyada hote hain, lekin wo sirf tab possible hota hai jab credit abhi hua nahi hota, reference, can a wire transfer be reversed.

MT192 cancellation kab tak kar sakte hain, aur kya details deni hoti hai?

Jitni jaldi ho sake, ideally kuch ghanton ke andar, jab payment abhi beneficiary account me credit nahi hua ho. Aapko MT103 reference, UETR, exact amount and currency, beneficiary bank details, aur clear reason dena hota hai, see can SWIFT transfer be reversed.

MT199 recall ke time me meri bank mujhe kaise contact karegi, aur mujhe kya reply dena chahiye?

Beneficiary bank aapko call ya email karegi, details verify karegi, aur consent maangegi. Agar duplicate payment hai, to professional courtesy se return approve kar sakte hain, warna agar services deliver ho chuki hain, aap refuse kar sakte hain, documentation zaroor maintain karein, invoices, emails, and reversal records.

Karbon Business use karne se SWIFT se related recall issues kaise kam hote hain?

Karbon Business aapko USD, GBP, EUR accounts deta hai, jisse US client ACH se domestic transfer karta hai, settlement fast hota hai, fees kam hoti hai, aur error hone par local rails me dispute resolution jaldi hota hai. INR conversion aap control karte hain, e-FIRA auto generate hota hai.

UETR number kaise track karu, client ke bank se mujhe kya mangna chahiye?

Client se UETR code mangiye, ya SWIFT gpi tracker ka status screenshot. UETR se aap dekh sakte hain payment intermediary bank me atka hua hai, beneficiary bank me pending hai, ya credit ho chuka hai, aur isi basis par aap MT192 ya MT199 decide karein.

Agar funds INR me convert ho chuke hain, aur recall aata hai, to mujhe forex loss kaise handle karna hoga?

Reversal aane par aapke account se INR debit hoga, conversion rate change ho chuka ho sakta hai, 1 se 3 percent tak movement common hai. Is loss ko aap contracts me address kar sakte hain, aur client ko explain karein ki return me currency difference aa sakta hai.

Bank charges kitne lagte hain, aur kya sender ya receiver bear karte hain?

Cancellation ke liye $75 se $120 total, recall ke liye $100 se $200 tak, kyunki return ek nayi payment hoti hai. Usually sender and receiver apne apne bank charges bear karte hain, lekin aap contract clause me responsibility clear kar sakte hain, reference, can you reverse international bank transfers.

India me e-FIRA aur tax filing par reversal ka kya impact hota hai?

e-FIRA initial credit par issue hota hai, reversal ke baad bhi woh record rehata hai. Aapko accounting me original receipt aur reversal dono track karne hain, agar payment dubara aata hai to naya e-FIRA generate hoga. CA ko inform karke income figures adjust karna zaroori hai, see can SWIFT transfer be reversed.

Agar client ne galat account me payment bhej diya, mujhe kya karna chahiye, kaam kab start karu?

Client ko turant MT192 cancellation request karne ko boliye, agar credit ho gaya hai to MT199 recall initiate karein. Jab tak original mistake resolve nahi hoti, new invoice issue na karein, kaam start ya deliver na karein, double payment risk se bachiye.

Recall scam kaise identify karu, meri taraf se kya safety steps lene chahiye?

Red flags, new email domains, third party refund accounts, vague reasons, aggressive tone. Kabhi bhi direct third party account me refund na bhejein, bank ke fraud team ko report karein, outbound transfers temporarily freeze karne ko kahe, paper trail maintain karein.

Karbon Business ke through agar duplicate ACH aa gaya, to return process kitna fast hota hai?

ACH ecosystem me returns, reversals aur NACHA rules ke under 5 business days ke andar process ho jate hain, SWIFT MT199 se kaafi faster. Karbon Business support team status track karne me help karti hai, re send coordinate karti hai, aur INR settlement with e-FIRA timely ensure kar deti hai.

Bank ko email karte waqt subject line aur content me kya likhu, taaki jaldi action ho?

Clear subject lines use karein, URGENT, MT192 Cancellation, UETR [code], ya MT199 Recall Request, MT103 [reference]. Body me UETR, MT103, exact amount, currency, value date, beneficiary details, reason, and evidence attach karein. Concise, complete requests fastest process hoti hain.

Disclaimer, The success of cancellations, recalls, and reversals depends on timing, banks, jurisdictions, and recipient consent. This is general information, not legal or tax advice. Consult your bank, a chartered accountant, or legal counsel for specific cases.