Key takeaways

- TT buying rate is used when your bank converts incoming USD, EUR, GBP, or CAD into INR, TT selling rate is used when your bank converts your INR into foreign currency for outward payments.

- The spread, TT selling minus TT buying, is the hidden markup that reduces your take home amount on inward payments and increases your costs on outward payments.

- For major pairs like USD/INR, typical spreads are 50 paise to 1 rupee, weekends and holidays often widen spreads further.

- Always compute expected INR using the bank’s TT buying or TT selling rate, then subtract or add fees, and compare against mid market to quantify the markup.

- Ask your bank to confirm locked rate versus indicative rate, cutoff times, full fee breakdown, purpose code, and e FIRA timelines before approving any transfer.

- Avoid dynamic currency conversion, insist clients pay in their local currency, time conversions around weekends, and maintain a comparison spreadsheet.

- Mid market plus flat fee platforms can reduce hidden spreads, for example, Karbon Business shows mid market rates and adds a clear platform fee while auto generating e FIRA.

- Keep invoices, SWIFT copies, bank statements, and e FIRA or FIRC organized, mismatched or missing documentation can delay credits and invite compliance queries.

TT Buying Rate vs TT Selling Rate: Quick Definitions

Before we dive into calculations, let us nail down what these terms actually mean.

What Is the TT Buying Rate?

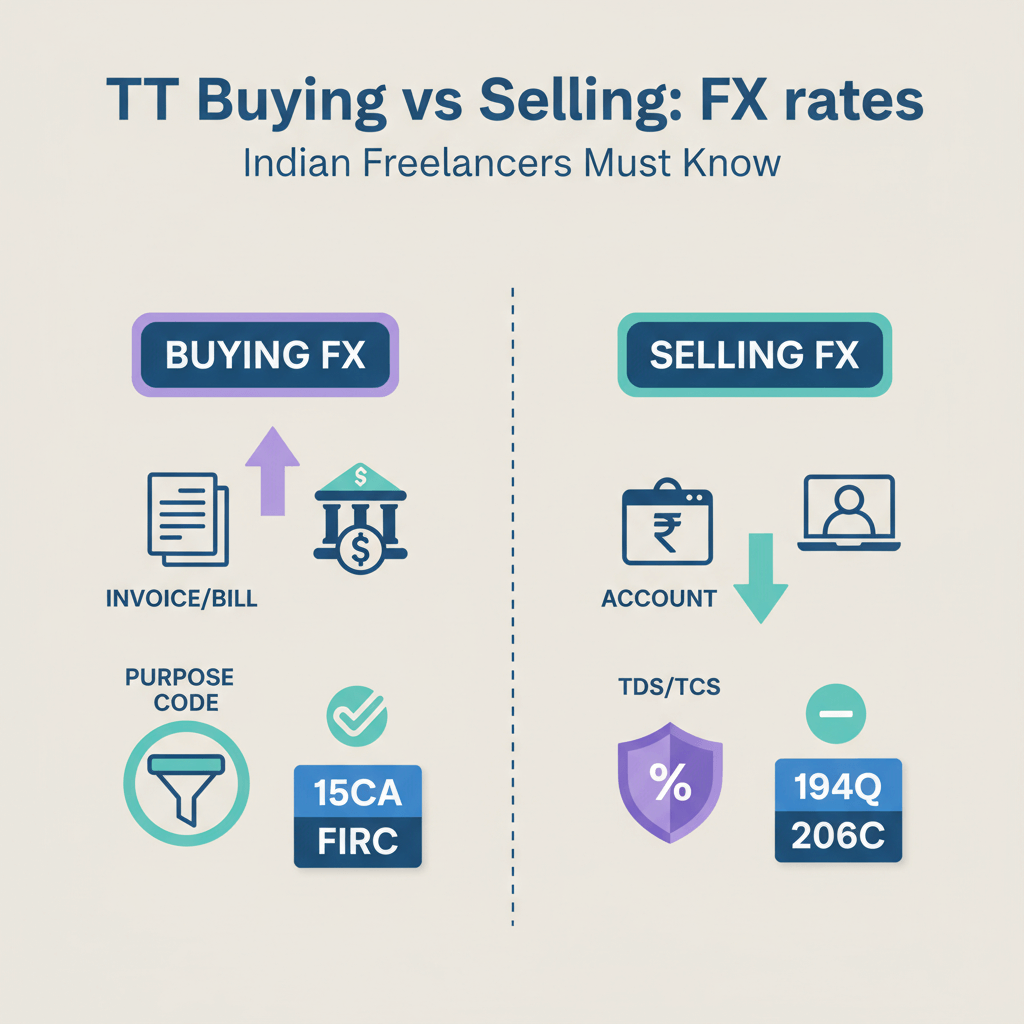

The TT buying rate is the exchange rate your bank uses when it buys foreign currency from you. In plain English, it is the rate applied when your client’s USD, EUR, GBP, or CAD payment arrives and needs to be converted into Indian rupees.

Think of any inward remittance, a software development invoice paid by a New York startup, a content writing fee from a London agency, or a consulting payment from a Toronto firm. All of these incoming payments get converted at the TT buying rate.

This rate applies when the bank’s Nostro account has already been credited, so they are ready to give you rupees immediately.

What Is the TT Selling Rate?

The TT selling rate is the flip side. It is the rate your bank uses when it sells foreign currency to you, converting your INR into USD, EUR, or another foreign currency for outward payments.

Subscribing to a SaaS tool, paying your HubSpot bill, or sending money to an overseas contractor, your bank debits rupees at the TT selling rate and sends out the foreign currency.

When Applied: Which Rate Do You Get in Real Life?

Inward Remittances for Services: TT Buying Rate

When you invoice a foreign client and they pay you via wire, ACH, SEPA, or Faster Payments, the funds land in your Indian bank account using the TT buying rate. Clean telegraphic transfers, demand draft collections, and export bill realizations all use the bank’s TT buying rate.

Outward Remittances and SaaS Payments: TT Selling Rate

When you pay a $300 subscription, or send €500 to a European freelancer, your bank converts your INR using the TT selling rate, which is always higher than the buying rate. This covers outward telegraphic transfers, foreign currency demand drafts, and refunds of inward payments.

Edge Cases: Chargebacks, DCC, Cash vs TT, Weekend Rates

- Chargebacks or failed export bills: A reversal can hit you at the TT selling rate, you received at buying, you repay at selling.

- Dynamic Currency Conversion: If a processor offers to “pay in INR,” it usually means a poor exchange rate. Ask clients to pay in their local currency.

- Cash rates vs TT rates: Physical cash exchanges carry handling costs, spreads are often wider than TT.

- Weekend and holiday rates: Banks add buffers when markets are shut, Monday credits from Friday evening instructions may reflect wider spreads.

Understanding the Spread and Why It Affects Your Income

Definition and Formula

The spread is the bank’s profit margin: the difference between TT selling and TT buying for the same currency at the same time.

Spread = TT Selling Rate − TT Buying Rate

Spread (%) ≈ (Spread ÷ Mid Market Rate) × 100

Example, mid market USD/INR is 83.50, TT buying is 83.10, TT selling is 83.90, spread is 0.80, which is roughly 0.96% of mid market. On a $5,000 payment that 0.80 costs you roughly ₹4,000.

Mid Market vs Bank Card vs TT Rates

Banks begin from the mid market rate, also called interbank. You see this on Google, XE.com, or Bloomberg. They subtract a margin to arrive at TT buying, and add a margin to arrive at TT selling. For an overview of how currencies are quoted globally, see exchange rate.

The Foreign Exchange Dealers Association of India issues guidelines that influence spreads. Banks publish intraday FX cards with TT buying, TT selling, and sometimes cash rates, and they revise rates as markets move.

Typical Spread Ranges and Timing Impact

- USD/INR often sees 50 paise to 1 rupee spreads, less liquid pairs like CAD/INR can be wider.

- Weekends and holidays usually widen spreads, a 0.80 weekday spread might become 1.20 on Saturday.

Illustrative snapshot, mid 83.50, TT buying 83.10, TT selling 83.90, spread 0.80, that gap is pure margin.

How to Compute Your Expected INR and Compare Providers

Step by Step Calculation Method

- Find today’s TT rate: Check your bank’s FX card, use TT buying for inward or TT selling for outward.

- Compute gross: Inward INR = Foreign Amount × TT Buying, Outward INR = Foreign Amount × TT Selling.

- Apply fees: Subtract fees for inward, add fees for outward, include GST and any correspondent charges.

- Measure markup: Compare against mid market to see the hidden percentage loss.

- Repeat for quotes: Run the same math across providers to identify the true all in cost.

Example inward: $5,000 × 83.10 = ₹415,500, minus ₹590 fees = ₹414,910 net.

Example outward: $300 × 83.90 = ₹25,170, plus ₹590 fees = ₹25,760 debited.

Checklist: What to Confirm With Your Bank

- Locked or indicative rate? Ask when the rate is fixed, quote time or settlement time.

- All in fees upfront? Processing, GST, SWIFT, and correspondent deductions in writing.

- Purpose code: Ensure the code and invoice description match to avoid delays.

- Cutoff times: Know the T+0 or T+1 implications if you miss the day’s cutoff.

- Mid market comparison: Keep a live mid rate alongside the TT rate to quantify spread.

Examples: Exact Math You Can Copy

$5,000 Inward at TT Buying Rate

Mid: 83.50, TT buying: 83.10, gross ₹415,500, fees ₹590, net ₹414,910. Versus mid market ₹417,500, your loss ₹2,590.

$300 Outward at TT Selling Rate

Mid: 83.50, TT selling: 83.90, gross ₹25,170, fees ₹590, total ₹25,760. Versus mid market ₹25,050, extra cost ₹710.

£2,000 Inward and Weekend Effects

Weekday: Mid 106.80, TT buying 106.20, net ≈ ₹211,810 after fees. Weekend buffer: TT buying 105.90, net ≈ ₹211,210, a ₹600 penalty due to wider spreads.

Quick formulas

Spread = TT Selling − TT Buying

Net INR, Inward = (Foreign × TT Buying) − Fees

Net INR, Outward = (Foreign × TT Selling) + Fees

Hidden Markup (%) = [(Mid − TT Buying) ÷ Mid] × 100

Compliance Must Knows for India

e FIRA, FIRC, and Purpose Codes

Every inward remittance triggers an e FIRA or FIRC, this is essential for GST and ITR. Your bank should issue it within 24 hours of credit, but delays happen if documentation is incomplete. Align your invoice description with the correct purpose code, common ones include P0803 for software exports, P0802 for consultancy, and P1007 for technical services. For background on terminology that banks use in public rate cards, see telegraphic transfer buying rates.

Record Keeping Tips

- Invoice copy with date, amount, and service details.

- SWIFT copy or client payment confirmation.

- Bank statement showing credit and final INR.

- e FIRA or FIRC as soon as issued.

- Email trail with scope, milestones, and payment terms.

Maintain a spreadsheet tracking Date, Client, Currency, Amount, Purpose Code, TT rate, Fees, Net INR, and e FIRA status. This saves time and supports RBI or tax queries.

Reducing Hidden Costs: Practical Tips

Timing, Hedging, and Holding Balances

- Time large conversions away from weekends and holidays.

- Consider partial conversion, hold the rest in permissible foreign currency balances.

- For recurring outflows, ask about forwards to lock rates for three or six months.

Avoiding DCC and Ensuring Rate Transparency

- Ask clients to pay in USD, EUR, or GBP, not INR via DCC.

- Confirm whether your rate is locked now or at settlement, SWIFT can be T+1 or T+2.

- Keep a comparison sheet with mid market, TT buying, TT selling, spread, and fees.

Mini Checklist Before Every Payment

- Rate quote versus mid market, TT buying or TT selling verified.

- Fees breakdown, processing, GST, SWIFT, correspondent charges.

- Documentation and purpose code match your invoice.

- Settlement timeline and cutoff times confirmed.

- e FIRA issuance timeline and requirements clarified.

Alternatives to Bank Spreads: How Mid Market Plus Flat Fee Models Work

Modern platforms show you the mid market exchange rate, then add a transparent flat fee, you see the exact math upfront, foreign amount × mid rate minus fee equals your net INR. Settlement is often faster, compliance is automated, and some allow holding balances to time conversions.

If you want a provider built for India’s regulations, Karbon Business offers multi currency accounts with local collection in USD, GBP, EUR, and CAD, INR settlement in 24 to 48 hours at mid market rates with a flat platform fee and zero forex markup, auto generated e FIRA within 24 hours, and an option to hold currency for up to 60 days to hedge forex risk.

What to Evaluate Beyond Price: Speed, Compliance, Support, Holding Periods

- Speed: One to two day settlement keeps cash flow smooth.

- Compliance automation: e FIRA issuance without branch visits is invaluable.

- Support: Quick responses matter when funds are stuck.

- Holding periods: Ability to hold USD or GBP can add 1% to 2% to your realized rate during rupee dips.

Common Pitfalls Even With Better Providers

- Rate timing: Confirm the exact locked rate at the instant of conversion.

- GST clarity: Check if the advertised fee includes GST.

- e FIRA delays: Keep invoices and purpose codes consistent to avoid hiccups.

- Limits: New accounts can have per transfer or monthly caps, plan large invoices accordingly.

FAQ

TT buying rate kya hota hai, mere USD inward payment par kaise apply hota hai?

TT buying rate woh exchange rate hai jisse bank aapke paas aane wali foreign currency ko INR me convert karta hai, yani jab client ka USD, EUR, GBP ya CAD payment aata hai to credit TT buying rate par hota hai, isliye net INR samajhne ke liye aapko bank ka TT buying rate dekhna chahiye.

TT selling rate kab lagta hai, aur outward remittance me cost zyada kyun ho jati hai?

TT selling rate tab lagta hai jab aap INR ko foreign currency me convert karke bahar pay karte ho, jaise SaaS subscription ya overseas vendor ko payment, selling rate buying rate se upar hota hai, isliye outward me spread plus fixed fees dono aapki cost badha dete hain.

Google pe dikh raha rate aur bank ke TT rate me itna difference kyun hota hai?

Google ya XE mid market rate dikhate hain, banks us mid rate par apna margin subtract karke TT buying nikaalte hain, aur margin add karke TT selling, ye margin hi spread hota hai jo aapke payment me hidden cost ban jata hai.

Spread kaise calculate karun, aur mujhe kitna loss ho raha hai kaise pata chalega?

Spread = TT selling minus TT buying, phir spread ko mid market se divide karke percentage nikaal lo, inward ke liye foreign amount × TT buying karke gross INR nikalo, fees minus karo, aur mid market ke against compare karke exact markup dekh lo.

Weekend ya holiday par payment aata hai to rate worse kyu hota hai?

Weekends me interbank market illiquid hota hai, isliye banks apna buffer badha dete hain, spreads wider ho jate hain, Monday credit par bhi Friday evening ka buffer reflect ho sakta hai jo aapka net INR ghata deta hai.

e FIRA ya FIRC kya hota hai, freelancer ke liye kyun important hai?

e FIRA electronic proof hai ki foreign exchange legally receive hua, GST filing, ITR, aur RBI compliance ke liye ye document mandatory hota hai, bank credit ke 24 ghante andar issue karna chahiye, isliye har inward ke baad e FIRA track karna zaroori hai.

Purpose code kaise choose karun, galat code se kya issue ho sakta hai?

Invoice description ke hisaab se code choose karo, jaise P0803 software exports, P0802 consultancy, P1007 technical services, galat code se credit hold, compliance query, ya e FIRA delay ho sakta hai, isliye invoice aur purpose code match rakho.

Karbon Business jaise platforms par mid market plus flat fee model me actual benefit kya milta hai?

Mid market transparent hota hai, aapko exact Google level rate milta hai aur upar se flat platform fee add hoti hai, hidden spread nahi hota, Karbon Business jaise providers 24 to 48 hours me INR settle kar dete hain, e FIRA auto generate hota hai, aur 60 din tak currency hold karne ka option mil sakta hai, jo timing advantage deta hai.

Bank se rate lock kaise karun, indicative aur settlement rate me confusion avoid kaise karun?

Forex desk se clearly poochho ki rate kab lock hota hai, quote ke time ya settlement ke time, SWIFT T+1 ya T+2 lag sakta hai, isliye email confirmation lo, aur cutoff time miss na ho iski planning karo.

Dynamic Currency Conversion avoid kaise karun, client ko kya bolun?

DCC me usually bekar rate milta hai, client ko simply bolo ki apni local currency me pay kare, USD, EUR, ya GBP me pay karne par bank ya provider standard TT ya mid rates use karta hai, isse aapka net INR better hota hai.

Freelancer ke liye outward SaaS payments me cost kam kaise karun?

Outward me TT selling spread plus fees lagta hai, isliye larger annual billing prefer karo jahan possible ho, weekends avoid karo, agar monthly recurring fix amount hai to forward rate lock explore karo, ya mid market plus flat fee provider consider karo, for example Karbon Business outward requirements me bhi transparent cost de sakta hai.

USD/INR me 0.80 paise spread practical impact kitna hota hai, koi simple thumb rule?

Roughly har $10,000 par 0.80 paise spread ka matlab ₹8,000 difference hota hai before fees, agar aap saal me $50,000 receive karte ho to sirf spread se ₹40,000 tak slip ho sakta hai, better timing aur transparent providers se ye figure kaafi kam ho sakta hai.

Kya me foreign currency hold karke better rate ka wait kar sakta hoon, practical approach kya hai?

Agar aapke paas EEFC ya provider balance hold facility hai to partial conversion karo, jitna immediate INR chahiye utna hi convert karo, baaki USD ya GBP me 30 to 60 din hold karke favorable dip par convert karo, platforms like Karbon Business ye flexibility provide karte hain jo 1% to 2% extra effective rate de sakti hai.

Wrapping Up

Understanding TT buying rate vs TT selling rate turns you from passive to proactive, spot the spread, compute the markup, factor fees, compare to mid market, and repeat for every transaction. Over a year, small differences snowball into real money. Check your bank’s FX card, build that comparison sheet, ask for locked rates, avoid DCC, time conversions smartly, and consider transparent providers that publish mid market plus a flat fee.

Disclaimer: This post is for informational purposes only, exchange rates fluctuate constantly, always verify live rates with your bank or provider, and follow RBI and FEMA regulations for all cross border payments.