Key takeaways

- Prioritize cashflow, not predictions: cover 30 to 45 days of INR expenses first, then decide how much USD to hold.

- Use simple rules, for example 50/50 or 40/30/30 laddering, to average rates and cut anxiety.

- Spreads usually cost more than visible fees, always compare to the mid market before converting.

- Have a target rate band, convert when the market hits it, and keep a buffer for the next cycle.

- Respect RBI’s 60 day limit to hold USD in multi currency accounts, and always collect e-FIRA for compliance.

- Tools like Karbon Business help with mid market execution, auto e-FIRA, and faster INR settlement.

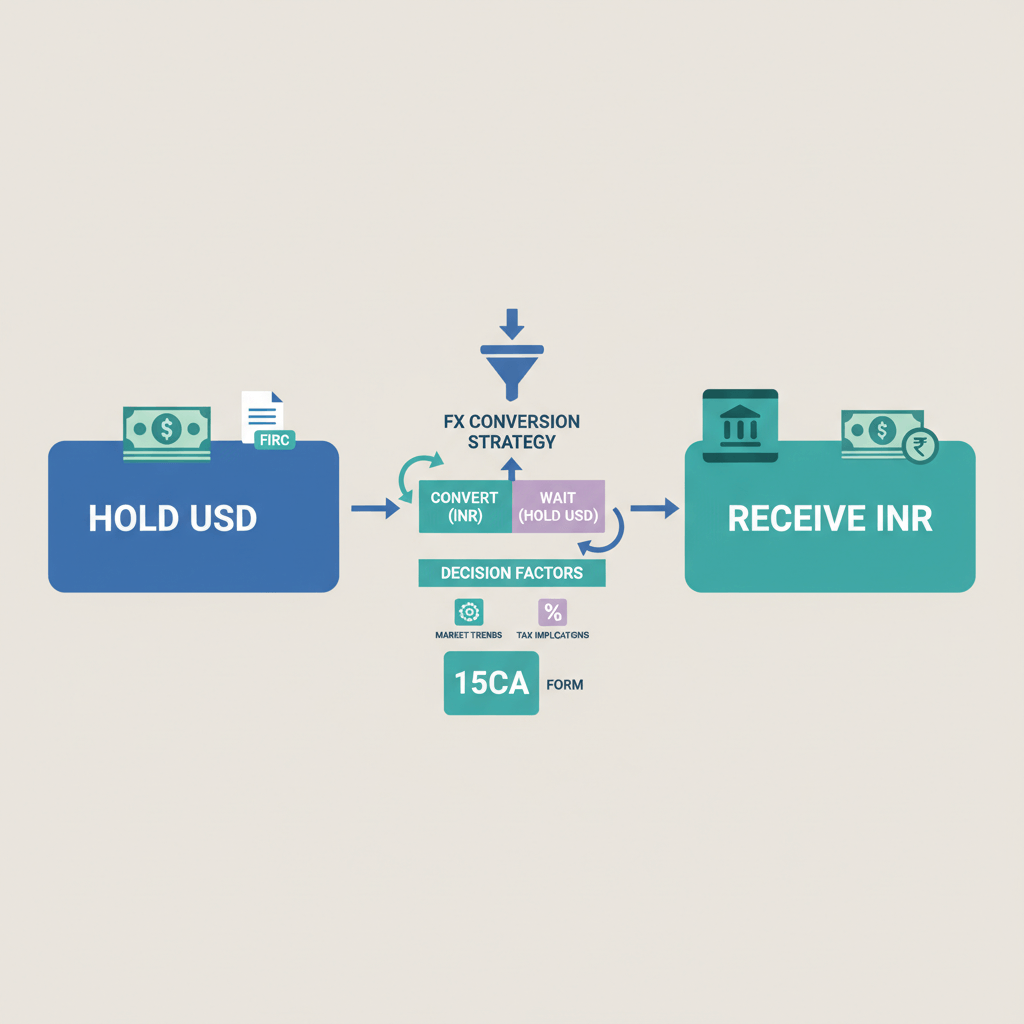

Hold USD vs convert to INR for businesses: what’s at stake

You just received a $5,000 client payment. USDINR swung 1.2% last week, the clock is ticking on payroll, rent, and GST. The real question isn’t “Can I guess the top,” it’s “How do I meet cash needs with minimal fx risk and minimal cost,” while staying compliant, calm, and in control.

Bottom line: Build INR runway first, then hold and ladder USD with rules you can stick to. Certainty today often beats chasing one more rupee tomorrow.

The 2 minute decision cheat sheet

- INR bills due within 7 to 14 days: Convert now. Zero runway means certainty > upside.

- 30 to 45 days INR buffer: Hold part of your USD for up to 60 days, stagger conversions to average rates.

- Rate hits your target band: Convert what you need plus 25 to 50% extra to create cushion for the next cycle.

Example: Payroll in 10 days? Convert 50% now, ladder the rest only if you have runway. You’ll sleep better and still have upside potential.

Essentials you must know: rates, fees, and spreads

Mid market rate is the real interbank rate. Banks and some platforms add a spread, often 1 to 2%, plus fees. Your net INR depends on the executable rate, not the headline claim.

Rule of thumb: Effective INR ≈ USD amount × mid market rate × (1 − total fee) − fixed charges.

Example on $5,000 at USDINR 83.50: Bank A with 1.8% spread and 0.5% fee nets you roughly ₹414,000. A mid market platform with 1% fee can be closer to ₹413,000 to ₹415,000 depending on final charges.

Spreads can quietly cost ₹6,000 or more on $5,000. Open a mid market source in one tab, your platform in another, and compare. If the gap is bigger than the stated fee, you’re paying hidden markups.

Understanding FX risk and how much to care

Fx risk is the chance your USD buys fewer rupees while you wait. Monthly swings of 0.5 to 2.5% are common around RBI and US data events. On $5,000, a 1% move is roughly ₹4,175 at 83.50—real money for payroll or software bills.

- If you can’t tolerate a ₹3,000 to ₹8,000 swing this month, convert more, sooner.

- If you have buffer and can tolerate volatility, hold some USD and ladder.

Convert before big events if missing payroll would hurt more than missing potential upside.

Cashflow planning first, rate view second

Map a simple 60 day INR cashflow: salaries, rent, GST, vendors. Build a minimum INR runway of 30 to 45 days so you never convert under pressure.

- Policy: Always cover the next 30 days in INR, non negotiable. Hold the rest in USD up to 60 days and review weekly.

- Worksheet example: Feb 1 payroll ₹2 lakh, convert $2,400 today. Feb 8 rent ₹1 lakh, ladder 30% of what’s left. Align to RBI weeks to derisk event volatility.

This converts a guessing game into a repeatable process designed around your expenses.

When to convert USD: practical triggers and tactics

- Triggers: INR due ≤14 days, rate hits your band, or looming RBI/US data weeks.

- Laddering: For example 40% now, 30% next week, 30% by day 30, to average volatility.

- 50/50 rule: Half now, half later—simple and effective.

- Hard stop: Convert all by day 55 to 58 to respect the 60 day limit.

- Best execution window: 10:30am to 3:30pm IST for tighter spreads.

Example: Receive $3,000 on Monday, payroll two Fridays away. Convert $1,200 Tuesday midday, another $900 if rates improve the following week, and the final $900 the Friday before payroll. You hit obligations and average rates calmly.

Spreads and execution quality: where money is won or lost

- Live rate: Is it mid market or marked up?

- All in cost: Fee + spread + wire charges. A “zero fee” offer with 2% spread is worse than a 1% fee at mid market.

- Speed: 24 to 48 hour INR settlement preserves runway and reduces risk.

Checklist before you convert:

- Verify the mid market reference.

- Target total cost under 1.5%.

- Execute during liquid hours.

Real scenario: $5,000 at 83.50 is ₹417,500 gross. A wider spread bank might land ~₹414,000, a mid market platform with a transparent fee can deliver ~₹413,000 to ₹415,000 net. That ₹3,000 to ₹6,000 difference can fund tools you actually use.

Compliance and operational guardrails for India

RBI and FEMA allow you to hold USD up to 60 days for hedging fx risk, after which you must convert via channels that generate e-FIRA for your records. Use correct purpose codes like P0801 for export of software services, attach invoices, and keep everything ready for your CA.

Tip: Platforms that auto generate e-FIRA within 24 hours save time and headaches. For a broader overview, see this guide to accept international payments in India.

Compliance isn’t a blocker, it’s a checklist: document the service, convert within 60 days, collect e-FIRA, file with ITR.

Three real world scenarios with numbers

Scenario A: Tight cashflow

You have payroll in 10 days. Convert now at mid market with a transparent fee and you lock certainty. Waiting two weeks only to see a 1% drop costs ~₹4,000 on $5,000 and raises stress.

Scenario B: 45 day runway

You ladder 40/30/30 over three weeks as rates oscillate between 83.50 and 84.00. You average around 83.75, cover bills, and pick up a modest gain versus a one shot conversion, while reducing downside risk.

Scenario C: Rate target hit

Target 84.00, market hits 83.95. Convert 70% now, hold 30% for two weeks. If it nudges up, you capture extra upside without risking obligations. If it dips, your core needs are already funded.

A simple playbook you can save

- Weekly 10 minute routine: Check INR runway, compare USDINR to targets, execute per your rules. No second guessing.

- Decision tree: Do you have 30 to 45 days INR runway? If no, convert all now. If yes, hold partially, ladder, review weekly.

- Template: Set a rate band (current ±0.5% to 1%), define tranches (50/50 or 40/30/30), hard stop by day 58.

This balances fx risk, cashflow planning, and cost without turning you into a trader.

Tools and templates

- Free spreadsheet: Columns for date, INR need, USD on hand, target band, action. Update every Monday.

- Calculator: Enter amount, rate, and fees, compare net INR across platforms before each conversion.

- Calendar reminders: Tranche dates and day 58 hard stop.

- Karbon Business dashboard: Hold USD, time conversions at mid market, and grab auto e-FIRA with WhatsApp updates.

FAQ

When should I convert USD if my rent or payroll is due next week?

Convert now. For obligations within 7 to 14 days, certainty beats potential upside. If you still have some INR runway left after that, ladder the remaining USD in small tranches.

Is it risky to hold USD for 30 to 45 days as a freelancer in India?

Expect 0.5 to 2.5% monthly swings. On $5,000 that’s roughly ₹2,000 to ₹10,000. If that range is acceptable and you have INR buffer for 30 to 45 days, you can hold part in USD and ladder conversions to manage volatility.

How do spreads impact my payout compared to fees?

Spreads are the hidden markup in your rate, and they often cost more than the visible fee. Always compare the platform’s executable rate to a trusted mid market reference. A platform like Karbon Business that prices at mid market with a transparent fee helps you keep more of your money.

What’s a simple rule to avoid overthinking the USD to INR timing?

Use the 50/50 rule: convert half now to cover near term INR needs, hold half and review weekly. If you prefer more structure, go 40/30/30 across three dates.

What is the best time of day to convert USD to INR for tighter pricing?

Typically 10:30am to 3:30pm IST sees better liquidity and tighter spreads. Avoid illiquid hours unless urgent.

Can I legally hold USD in India before converting, and for how long?

Yes, under RBI and FEMA you can hold export proceeds in approved multi currency accounts, commonly up to 60 days for hedging risk. Convert within that window and ensure you get e-FIRA for compliance.

What documents do I need when converting USD earnings as a freelancer?

Invoice matching the inward remittance, correct purpose code (for example P0801 for software exports), and e-FIRA after conversion. Platforms such as Karbon Business auto generate e-FIRA, which makes CA work and GST filings easier.

How do I set a target rate band without being a trader?

Pick a band around the current rate, for example ±0.5% to 1% based on recent volatility. Convert when the market hits the band, and always convert enough to cover the next 30 days of INR expenses.

Should I convert everything at once or in parts when I get paid from abroad?

If INR runway is short, convert most or all immediately. If you have 30 to 45 days buffer, convert in parts to average rates. Many Indian freelancers use a 70/30 or 50/50 split to balance certainty and upside.

How does Karbon Business compare to typical bank conversions for freelancers?

Banks commonly add 1 to 2% spread plus fees. Karbon Business prices at the mid market with a clear platform fee and provides auto e-FIRA, faster settlement, and WhatsApp updates. On typical $5,000 conversions, tighter execution can save you several thousand rupees versus marked up rates.

What if I am waiting for a round number like 84.00 on USDINR, is that smart?

It’s fine to have a target, but avoid all or nothing bets. Convert enough when you’re near the band to cover obligations, then hold a smaller tranche for potential upside. This way your bills are safe even if the market reverses.

How do I reduce anxiety about USD to INR timing as a solo freelancer?

Write a simple policy: always fund 30 days INR, define a target band, execute in tranches, and set a hard stop by day 58. Use a platform like Karbon Business for mid market execution and e-FIRA so you focus on work, not the ticker.