Key takeaways

- SEPA is euro only and behaves like a local transfer across 36 European countries, while SWIFT is the global network for multi currency wires with higher, less predictable fees. For a quick primer, see SEPA vs SWIFT.

- Indian banks don’t issue IBANs, so you can’t receive SEPA directly into an Indian account. Use a EUR IBAN to collect via SEPA, then remit INR to India with e-FIRA for compliance.

- SEPA is typically faster and cheaper than SWIFT. Standard SEPA settles in one business day, SEPA Instant in seconds. SWIFT often takes 1–5 business days.

- For regular EU clients paying in EUR, open a virtual EUR account with a SEPA eligible IBAN. Platforms like Karbon Business are built for Indian freelancers.

- Always track total cost: transfer fees, intermediary fees, and FX markup. Prefer mid market conversion with zero FX markup plus transparent flat fees.

- Keep compliance airtight: ensure matching names across invoices and accounts, and secure e-FIRA/FIRC for every inward remittance.

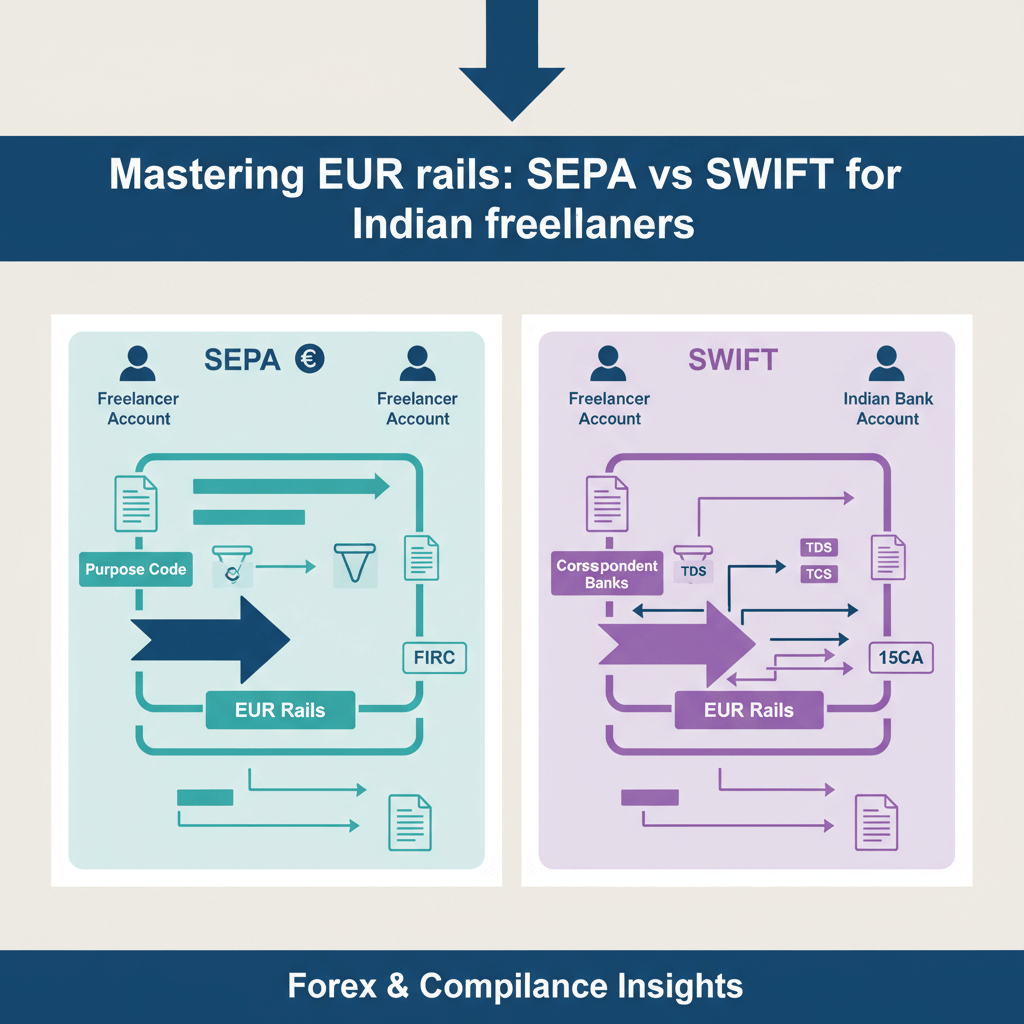

Why understanding SEPA vs SWIFT matters for Indian freelancers receiving euros

When your German client prefers SEPA, and your Indian bank talks SWIFT, you face a payments puzzle that affects speed, fees, and compliance. In Europe, SEPA is normal, cheap, and fast. India, being outside the SEPA zone, pushes most direct receipts into SWIFT. The result, for many freelancers, is slower payments and stacked fees. A practical understanding of SEPA vs SWIFT helps you choose the right rail, save thousands of rupees, and stay fully compliant with RBI through e-FIRA.

Bottom line: SEPA gives you speed and predictability for euro payments, while SWIFT gives you global reach and multi currency support. For Indian freelancers, combining both smartly is the win.

SEPA meaning: what every freelancer should know

SEPA, the Single Euro Payments Area, standardizes euro transfers across 36 countries so they behave like domestic payments. Conceptually, it turned cross border euro transfers into local transactions, cutting costs and errors. For a deep dive into the main differences, and another clear explainer on SEPA vs SWIFT, explore these guides.

- Euro only. If the money isn’t in EUR, SEPA doesn’t apply.

- Uses IBANs. Often you don’t even need a BIC/SWIFT code.

- Three rails: SEPA Credit Transfer (1 business day), SEPA Instant (seconds, 24/7), SEPA Direct Debit (pulls with mandate).

For you, the magic is simple: if you can provide a SEPA eligible IBAN and your client sends euros from within SEPA, the payment is fast, inexpensive, and highly reliable.

SWIFT basics: the global alternative

SWIFT, the Society for Worldwide Interbank Financial Telecommunication, is a secure messaging network that orchestrates international transfers between 11,000+ institutions in 200+ countries. It supports all major currencies, including EUR, USD, GBP, and INR. Transfers use BIC/SWIFT codes, account numbers, and sometimes extra routing info. The complexity often comes from correspondent banks. To understand how fees and delays creep in, see payment routing explained.

Expect 1–5 business days for SWIFT, variable fees at multiple points, and less predictable data and tracking. Still, SWIFT is the default path to Indian bank accounts—India isn’t part of any regional euro scheme.

Core comparison: SEPA vs SWIFT side by side

Here’s how they differ at a glance, with references like the main differences, SEPA vs SWIFT, and key differences explained.

| Feature | SEPA | SWIFT |

|---|---|---|

| Currency | EUR only | Multi currency, global |

| Geography | 36 SEPA countries | 200+ countries |

| Speed | 1 business day; seconds for Instant | 1–5 business days |

| Fees | Low or zero, domestic like | Higher, intermediaries add costs |

| Identifiers | IBAN, BIC often optional | BIC/SWIFT + account details |

| Best for | Euro transfers within SEPA | Global, non EUR, outside SEPA |

If you want SEPA style benefits but live in India, you’ll likely use a EUR IBAN as a bridge. See how Indian freelancers get paid from EU via SEPA without friction.

Decision framework: when to choose SEPA vs SWIFT for euro transfers

- Choose SEPA when the client is in the SEPA zone, payment is in EUR, and you can provide a SEPA eligible IBAN. It’s almost always faster and cheaper. Reference: SEPA vs SWIFT.

- Choose SWIFT when you’re receiving directly to an Indian account, the client is outside SEPA, or the currency isn’t EUR. See the main differences.

Also weigh amount, urgency, client bank capabilities, and total cost including FX. A helpful explainer on what’s the difference between SEPA and SWIFT can guide expectations.

Practical how to for Indian freelancers handling euro transfers

Because Indian banks don’t issue IBANs, you can’t receive SEPA directly into an Indian account. See the main differences for the structural reasons, then pick one of two paths below.

Option A: receive via EUR IBAN, then settle to India

This route unlocks SEPA speed and cost benefits, then remits INR to your Indian bank with full compliance.

- Open a virtual/local EUR account that gives you a SEPA eligible IBAN. For instance, Karbon Business offers EUR IBANs for Indian freelancers, alongside USD, GBP, and CAD.

- Invoice with your IBAN and ask for “SEPA Credit Transfer” or “SEPA Instant Credit Transfer.”

- Funds arrive fast thanks to SEPA. Timelines explained here: SEPA vs SWIFT.

- Convert to INR at mid market rates with zero FX markup, pay a transparent platform fee, and get auto generated e-FIRA within 24 hours. See SEPA vs SWIFT for context on costs and speed.

Result: lower total cost, faster cash flow, automated compliance.

Option B: receive directly to Indian bank via SWIFT

- Share your bank’s BIC/SWIFT, account number, and exact account name.

- Request a EUR SWIFT transfer, include invoice references.

- Expect 1–5 business days. Variability comes from intermediaries—see key differences explained.

- Collect FIRA/FIRC or e-FIRA from your bank; fees will apply. More in SEPA vs SWIFT.

Good for occasional EUR payments; less efficient for regular EU work.

Why SEPA doesn’t apply directly to India and the workaround

SEPA requires IBAN based accounts within the SEPA zone, while Indian banks use domestic formats under RBI rules. Hence, direct SEPA to India isn’t possible. See the main differences and this overview of what’s the difference between SEPA and SWIFT.

The workaround: receive into a SEPA zone EUR IBAN first, then remit INR to India through a compliant channel that issues e-FIRA. You keep SEPA’s low cost, fast euro leg, and satisfy India’s regulatory leg.

Common pitfalls and how to fix them

- IBAN errors. Copy paste your IBAN and ensure your beneficiary name matches exactly. More tips in SEPA vs SWIFT.

- Client sends SWIFT instead of SEPA. State “Payment method: SEPA Credit Transfer to IBAN …” on the invoice. See the difference between a SEPA and a SWIFT payment.

- SWIFT hidden fees. Request fee option “OUR” or at least “SHA,” and ask for estimates upfront. Reference: SEPA vs SWIFT.

- Compliance holds. Ensure consistent names and clear invoice narratives. Overview here: what’s the difference between SEPA and SWIFT.

- Timing surprises. Not all banks support SEPA Instant; check availability and cut off times. See SEPA vs SWIFT.

- Currency confusion. SEPA is euro only; specify EUR on the invoice if you want SEPA.

Fees, FX rates, and compliance essentials for euro transfers

SEPA fees. Typically minimal, often zero or just a few euros. See a quick explainer on what’s the difference between SEPA and SWIFT.

SWIFT fees. Sender, intermediaries, receiver—costs accumulate and are hard to predict; see key differences explained.

FX markups. Prefer mid market rates with zero markup; avoid hidden spreads. Many platforms show the live mid market rate you’d see on Xe.com.

Platform fees. Seek transparent, flat pricing over blended FX + fee structures.

RBI/FEMA compliance and e-FIRA. Always secure e-FIRA for inward remittances. Background: SEPA vs SWIFT and this e-FIRA/FIRC documents guide.

Taxes. Report INR equivalents accurately; if you hold EUR before converting, track dates and rates. Consult a CA if needed.

Step by step checklist for choosing and using SEPA or SWIFT

- Confirm client location and currency. If SEPA zone + EUR, SEPA is likely best; otherwise SWIFT.

- Pick your path. EUR IBAN + SEPA for efficiency, or direct SWIFT to India for simplicity.

- Share accurate details. IBAN for SEPA, SWIFT/BIC and account details for India.

- Invoice clearly. State “SEPA Credit Transfer” or “SWIFT,” include terms and references.

- Track the payment. SEPA: 1 business day or seconds with Instant; SWIFT: expect a few days.

- Settle to INR and get e-FIRA. Convert at fair rates, download your e-FIRA, and reconcile.

- Review and optimize. Compare total cost and speed, then standardize your best flow.

Bringing it all together: make euro transfers work for your freelance business

SEPA is a fast, low cost rail for euros within Europe; SWIFT is the global, multi currency backbone. Indian freelancers can’t take SEPA straight into Indian accounts, but can use a EUR IBAN to collect via SEPA, then remit INR with full RBI compliance and e-FIRA. For repeating EU invoices, this simple change often boosts effective earnings and reduces stress.

Consider setting up a virtual EUR IBAN today. Compare fees, FX, settlement times, and e-FIRA automation. If you frequently work with European clients, platforms built for Indians—like Karbon Business—can turn slow, expensive euro payments into quick, predictable cash flow.

FAQ

SEPA vs SWIFT which is better for Indian freelancers getting paid in euros?

For euro payments from European clients, SEPA is usually better because it’s faster and cheaper. But India isn’t in SEPA, so use a EUR IBAN to collect via SEPA, then remit INR to your Indian bank. Platforms like Karbon Business provide a EUR IBAN and automate e-FIRA, making the workflow smooth.

Can I give my Indian bank details and ask my EU client to do a SEPA transfer?

No, SEPA needs an IBAN within the SEPA zone. Indian accounts don’t have IBANs, so the bank will reject the transfer or switch to SWIFT. Instead, receive into a EUR IBAN first, then convert and settle to India with e-FIRA for compliance.

How fast do SEPA payments come compared to SWIFT wires to India?

SEPA Credit Transfer lands in about one business day, SEPA Instant in seconds. SWIFT to India can take 1–5 business days because of correspondent banks and compliance checks. If speed matters, collect via SEPA into a EUR IBAN, then settle INR quickly.

What is the cheapest way to receive small euro invoices from EU clients?

Use SEPA to a EUR IBAN to avoid multi bank SWIFT fees. Convert at mid market rates with zero FX markup and a flat platform fee. Karbon Business, for example, charges a transparent percentage and provides e-FIRA automatically.

How do I make sure I get the full amount when the client pays via SWIFT?

Ask the client to choose the OUR fee option so the sender bears all bank charges. Also include invoice references and confirm intermediary bank fees. Still, SWIFT costs may vary, so using SEPA to a EUR IBAN can be more predictable.

What documents do I need in India after receiving foreign payments?

You need e-FIRA/FIRC for each inward remittance. If you use a platform that supports SEPA collection and INR settlement, it can auto generate e-FIRA within 24 hours. Karbon Business provides this by default, which simplifies tax filing and RBI compliance.

Is there any limit on SEPA Instant for freelancers?

Limits depend on the sending and receiving banks, often around 100,000 EUR per transaction. For standard SEPA Credit Transfer, limits are higher and sufficient for most freelance invoices. For very large transfers, confirm limits with your provider.

Will my client’s bank support SEPA Instant, or will it default to normal SEPA?

Not all EU banks support SEPA Instant yet. Ask your client to check their bank app or branch. If Instant isn’t available, standard SEPA still settles in about one business day, which is much faster than typical SWIFT timelines to India.

How do I reduce FX loss when converting EUR to INR?

Use a service that converts at the live mid market rate with zero FX markup, and charges only a transparent platform fee. With Karbon Business, you can hold euros briefly, convert at mid market rates, and settle INR, which helps maximize your rupee receipts.

What should I write on the invoice so the client definitely uses SEPA?

Include “Payment method: SEPA Credit Transfer” and your full IBAN. Add a note: “SEPA transfers are faster and lower cost for EUR payments within Europe.” This nudges the payer and their bank to route via SEPA, not SWIFT.

If I already use SWIFT to my Indian bank, is switching to a EUR IBAN worth it?

If you regularly work with EU clients in euros, yes. You’ll likely save on total fees, gain speed, and get better FX. Many freelancers report savings of thousands of rupees per month. Platforms like Karbon Business make onboarding quick and handle e-FIRA automatically.

Will I face any RBI or tax issues if I receive via EUR IBAN and then settle to India?

No, provided you use a compliant provider that remits INR through authorized channels and issues e-FIRA for every transaction. Keep your KYC updated, ensure invoice names match account names, and maintain records for your CA at tax time.