Key takeaways

- A chargeback is a forced reversal initiated by the client’s bank, unlike a refund that you control, it can hit your INR balance weeks later with extra fees, and it affects your processor reputation.

- Know the lifecycle, transaction to arbitration, map each stage to deadlines and evidence requirements; study the chargeback process in detail.

- Reason codes matter, fraud, processing errors, and consumer disputes need different evidence; “services not as described” requires airtight SOW, milestone sign-offs, and delivery logs.

- Respond fast, ideally within 7 to 10 days, even if networks allow 20 to 45 days; set alerts and internal SLAs to avoid auto losses.

- Prevent disputes proactively, enable 3D Secure on payment links, use bank transfers for larger invoices, clarify scope and refund terms, and keep a clean audit trail.

- India-specific realities, e-FIRA supports compliance and tax filings, currency conversion risk can magnify losses, reversals hit upcoming INR payouts or linked accounts.

- Use purpose-built platforms for cross-border work, Karbon Business offers virtual foreign accounts, 3DS links, auto e-FIRA, and fast support, see fraud prevention for Indian freelancers.

- When in doubt, issue a voluntary refund to save fees and avoid ratio penalties, compare approaches using refunds and chargebacks for Indian freelancers.

What is a chargeback and why it matters for freelancers

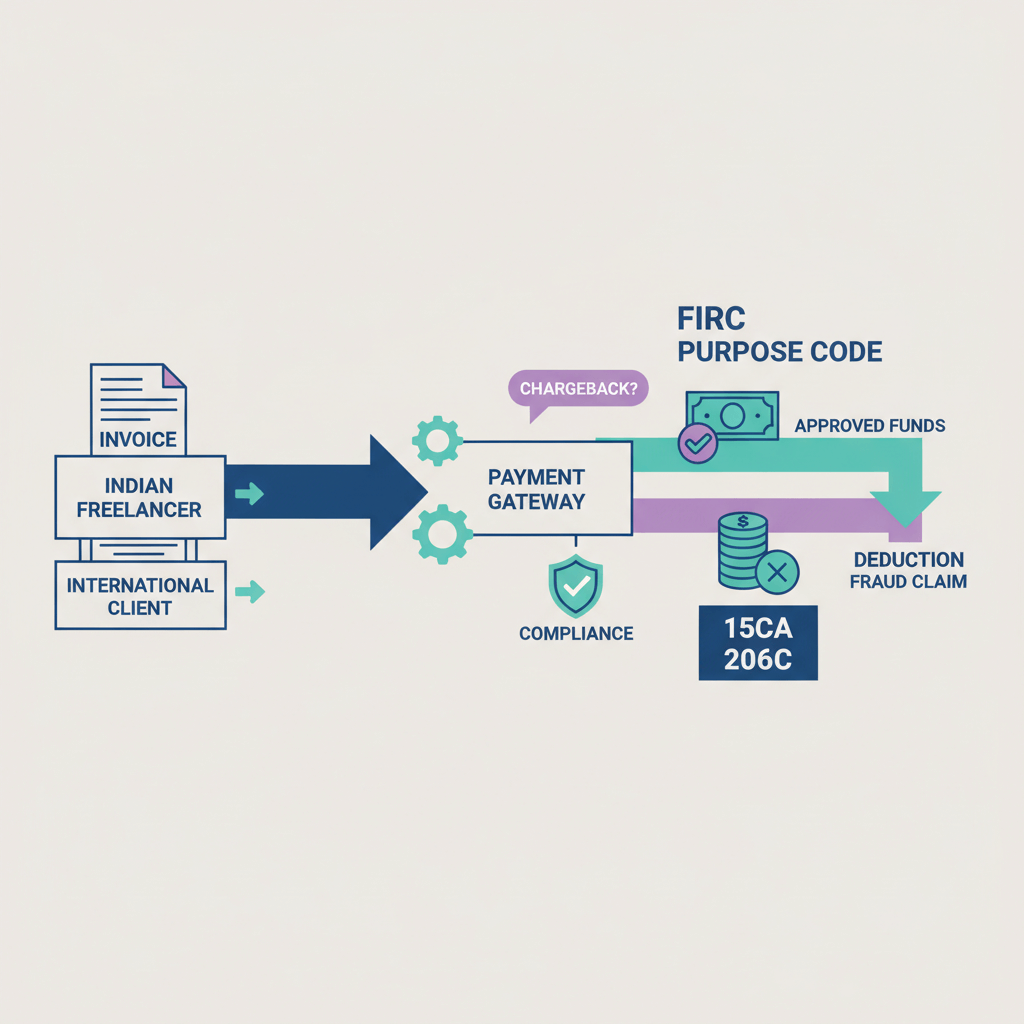

A chargeback is a payment reversal triggered by your client’s issuing bank, not by you. Unlike refunds that you initiate voluntarily, a chargeback can claw back settled funds plus fees after weeks or months, affecting cashflow and your standing with payment processors. For Indian freelancers managing projects, invoices, and compliance, a single dispute can be disruptive and costly. For more context, review refunds and chargebacks for Indian freelancers and the industry-standard chargeback process.

Why it stings more in India: you convert USD or EUR to INR, pay platform fees, maybe file export paperwork, then a reversal lands and the processor debits your next payout, sometimes with currency loss due to exchange movements. High ratios can freeze card rails, cutting off future international income.

Bottom line: chargebacks cause lost revenue, dispute fees, and admin burden, at the exact time you should be focused on delivery and growth.

Chargeback vs refund, knowing the difference saves you money

Refund: voluntary, initiated by you from your dashboard. Clean records, no dispute fees, client receives money in 7 to 30 days. You retain processor goodwill.

Chargeback: involuntary, initiated by the cardholder via their bank. Provisional credit to the client, funds debited from you plus fees, and you must submit evidence to recover money. Too many disputes can jeopardize access to card networks.

Rule of thumb: if a complaint is valid, issue a refund yourself. It reduces fees, keeps ratios healthy, and avoids formal disputes that processors track.

Who is involved in an international chargeback and cross-border nuances

- Cardholder, your client, files the claim, usually in the US, UK, or EU.

- Issuing bank, reviews the claim, assigns a reason code, sends the chargeback through the network.

- Card network, Visa or Mastercard, sets rules and arbitrates if escalated.

- Acquiring bank or processor, receives notice, debits your account, and relays deadlines.

- You, the freelancer, compile evidence for representment.

Cross-border complications include currency conversion risk, stricter network timelines, and Indian compliance. You still must keep export invoices and e-FIRA, but issuers focus on delivery proof, not local compliance. Study definitions in this chargeback processing glossary.

The chargeback lifecycle, step-by-step

Step 1: Transaction

The client pays via your card link, funds settle to INR within one to two days, and you file your e-FIRA and move on.

Step 2: Dispute opened

Up to 120 days later, sometimes longer for services, the client contacts their bank alleging fraud, non-delivery, or dissatisfaction.

Step 3: Provisional credit

The issuer grants provisional credit to the client, the network forwards the chargeback, your processor debits the transaction amount plus a fee.

Step 4: Notification

You receive the reason code, case details, and response deadline via email or dashboard, sometimes days after filing, reducing your window.

Step 5: Representment

Submit evidence mapped to the reason code within 20 to 45 days depending on network and region. Your processor forwards it to the issuer.

Step 6: Pre-arbitration

If rejected, you can escalate, provide clarifications, or accept the loss. Windows often run 10 to 20 days.

Step 7: Arbitration

The card network issues a binding decision, fees can exceed small dispute amounts, so escalation is rare for freelancers.

Step 8: Resolution

- Win: funds return to your account, usually minus the dispute fee.

- Lose: permanent loss of funds and fee, frequent losses increase risk with gateways.

Track official limits using guides like check the credit card chargeback process and the canonical chargeback process.

Dispute reason codes, what they mean and how to respond

Reason codes indicate the issuer’s rationale and dictate evidence strategy. Common buckets include fraud or unauthorized use, processing errors, and consumer disputes.

- Visa 10.x, Fraud: client claims unauthorized use. Submit 3D Secure results, IP and device data, AVS and CVV match, and email confirmation of the order.

- Visa 13.x or Mastercard 4853, Consumer dispute: “not as described” or “services not provided.” Provide signed SOW, milestone sign-offs, delivery proof such as repo links or design files, and communication logs.

- Mastercard 4837, Fraudulent transaction: duplicate or unrecognized billing. Show detailed invoices, distinct transaction IDs, and evidence of separate deliverables.

Strategic tip: always align evidence with the reason code. For “services not provided,” emphasize timestamped delivery records, commits, and view logs. For “not as described,” lean on SOW clauses and written approvals. For deeper reference, see the chargeback process guide.

Time limits to track and internal deadlines to set

- Cardholder filing: up to 120 days for most transactions, sometimes longer for services.

- Your representment: typically 20 to 45 days from notice, set an internal target of 7 to 10 days to build a buffer.

- Pre-arbitration: another 10 to 20 days depending on network.

- Full cycle: often 30 to 120 days, plan cashflow accordingly.

Automate alerts in email or WhatsApp, many freelancers miss deadlines because they do not see the notice in time. Compare approaches in check the credit card chargeback process and this chargeback processing glossary.

Evidence list, what to collect and how to package it

Winning depends on clear, organized proof. Store documents for at least 13 months post payment.

- Contractual proof: signed SOW, detailed invoice, and milestone approvals.

- Delivery proof: GitHub commits, design file links, cloud access logs, time tracking reports, deployment records, or live URLs with timestamps.

- Communication logs: email, Slack, WhatsApp messages that confirm consent, changes, and approvals.

- Authentication data: 3D Secure outcome, AVS, CVV match, and a recognizable billing descriptor.

- India compliance: auto generated e-FIRA, export invoice, FEMA documentation for records and taxes.

Rebuttal memo snapshot

Re: Chargeback [ID] – Reason Code 13.5

The transaction is valid. Evidence attached:

1. Signed SOW, scope defined and met.

2. Client approval emails, dated milestones show acceptance.

3. Delivery proof, links and logs with timestamps.

Request reversal of chargeback.

For templates, see refunds and chargebacks for Indian freelancers.

How to respond efficiently, practical checklist

Step 1: Read the notification carefully

Note reason code, response deadline, transaction date and amount, client name.

Step 2: Decide whether to fight or accept

- Fight if the amount is material, evidence is strong, and the relationship is not toxic.

- Accept if the fee exceeds the amount, documentation is weak, or you should have refunded.

Step 3: Compile your evidence

Use a one page narrative that maps each item to the reason code, be factual and concise.

Step 4: Submit via your processor dashboard

Upload, confirm, screenshot the submission, and track status daily.

Step 5: Post mortem

Identify gaps, update SOW templates, onboarding checklists, and client screening.

Process references, check the credit card chargeback process and the universal chargeback process.

Prevention tactics for services and digital work

Use bank transfers for larger payments

For invoices above 500 USD, encourage ACH, SEPA, or FPS instead of cards. Bank transfers carry far lower chargeback risk. Learn how to position this in your proposals using negotiate client payment method.

Platforms with virtual foreign accounts, like Karbon Business, let clients pay locally, you receive INR quickly, and you reduce disputes.

Enforce 3D Secure on card links

3DS adds authentication and can shift liability away from you for fraud claims. Enable it on every link, and streamline your checkout flow with payment links for freelancers in India.

Write clear scopes with milestones

Specify deliverables, timelines, payment schedules, and exclusions. Require written sign offs at each milestone.

Use recognizable billing descriptors

Ensure your descriptor includes your brand or project type, confusing descriptors trigger “unrecognized” disputes.

Display a clear refund policy

Show terms on invoices and payment pages, clients who understand terms are less likely to dispute.

Respond to complaints within 24 hours

Quick, professional communication defuses disputes early, a voluntary refund often costs less than a chargeback.

Verify clients and log changes

Check company domains, LinkedIn profiles, and do a video call. Track scope changes in writing. For more tactics, explore fraud prevention for Indian freelancers.

India-specific notes on reversals, compliance, and taxes

Reversals debit upcoming INR payouts or your linked bank account, maintain a buffer for four months post card payment.

RBI and FEMA compliance requires export invoices and remittance proof, e-FIRA is essential for tax and audit, though issuers decide based on delivery evidence first.

GST applies on platform fees, not on reversed transaction amounts.

Deep dives are available in refunds and chargebacks for Indian freelancers.

How Karbon Business supports Indian freelancers with chargeback management

- 3DS-enabled links reduce fraud disputes and shift liability for unauthorized transactions.

- Real-time alerts through dashboard and WhatsApp keep you on deadline.

- Auto e-FIRA in 24 hours simplifies compliance and tax records.

- Evidence repository centralizes invoices, links, transaction IDs, and e-FIRAs for quick representment.

- Virtual USD, GBP, EUR, CAD accounts help you transition larger projects to ACH, SEPA, or FPS to minimize chargeback exposure.

- Responsive support under 20 minutes helps with reason codes, rebuttal letters, and packaging evidence.

Explore best practices in fraud prevention for Indian freelancers.

Tools and platforms for receiving international payments with lower chargeback risk

- Karbon Business Karbon Business, virtual foreign accounts, flat one percent fee, zero FX markup, 3DS links, auto e-FIRA, fast support.

- Wise Business, solid multi currency accounts, limited India compliance automation.

- Payoneer, broad coverage, higher FX spreads and slower INR settlement.

- PayPal, easy to accept, higher fees and merchant unfriendly dispute workflows.

- Razorpay X International, India centric, card first flows with typical chargeback risks.

- Tazapay, B2B escrow, milestone protection through holdbacks.

Recommendation: for amounts above 500 USD, prefer bank transfers to avoid card disputes. For smaller invoices, use 3DS links and rigorous documentation, see payment links for freelancers in India.

Real story, how a Mumbai UX designer won a chargeback

Priya delivered wireframes and prototypes for a 1,200 USD project. A Visa consumer dispute arrived 60 days later, “services not as described.” She identified the code, assembled signed SOW, milestone approvals, Figma access logs, 3DS authentication, and e-FIRA, then submitted a concise rebuttal within seven days. The issuer reversed the chargeback in 18 days. Lessons, mandate written approvals, use milestone billing, and prefer ACH for projects above 1,000 USD. See similar cases in refunds and chargebacks for Indian freelancers.

Practical resources, templates and checklists

Chargeback response memo template

Dispute ID: [Transaction ID]

Reason Code: [e.g., Visa 13.5]

Due Date: [Response Deadline]

Narrative:

The transaction on [date] for [amount] was valid and delivered per the agreed scope. Evidence attached:

1. Signed Scope of Work, deliverables clearly met.

2. Client approval emails, dated for each milestone.

3. Delivery proof, links and logs with timestamps.

4. Authentication, 3D Secure result and AVS or CVV match.

Request: Reverse chargeback and restore funds.

Attachments: [List file names]

Pre payment checklist

- Enable 3D Secure on the payment link.

- Use a recognizable billing descriptor.

- Display refund and delivery terms on invoice or payment page.

- Verify client identity via LinkedIn, domain, or a quick video call.

- Secure a signed contract or SOW with clear deliverables.

Evidence gathering checklist

- Signed contract or SOW.

- Invoice with payment terms.

- Milestone approval emails or messages.

- Delivery proof, code repos, design files, access logs.

- Communication logs, email, Slack, WhatsApp.

- 3D Secure or AVS or CVV match results.

- Auto generated e-FIRA for compliance.

Final thoughts, discipline and documentation protect your international earnings

You cannot eliminate chargebacks completely, but clear contracts, milestone approvals, strong evidence trails, and quick responses drastically improve outcomes. For Indian freelancers, currency conversion, compliance, and time zones add complexity, yet they are manageable with the right platform and routine. Encourage bank transfers for larger projects, enable 3DS for card links, and track every approval in writing. When a dispute lands, treat it like a process, read the code, collect evidence methodically, submit early, and learn from the result. For deeper reading, revisit refunds and chargebacks for Indian freelancers and the authoritative chargeback process.

FAQ

Chargeback aagaya after two months, as an Indian freelancer what is the first thing I should do?

Log in to your processor dashboard immediately, note the reason code and deadline, then assemble signed SOW, milestone approvals, delivery logs, and 3D Secure results. Submit a concise rebuttal within 7 to 10 days, even if your notice allows longer. If you use Karbon Business, you will get real time alerts and a centralized evidence trail that makes this faster.

How can I reduce chargebacks on international card payments without losing clients?

Push larger projects to ACH, SEPA, or FPS, keep card payments for smaller invoices, enable 3D Secure, clarify scope and refund terms, and respond to complaints within 24 hours. Platforms like Karbon Business offer 3DS links and virtual foreign accounts, so you can accept bank transfers with minimal friction.

Client says “service not as described,” how do I win this dispute?

Submit a signed SOW, milestone sign off emails, timestamped delivery proof, and communication logs showing approvals. Keep your narrative factual and map each piece of evidence to the reason code. Karbon Business support can help you structure the memo and package your files cleanly.

Is 3D Secure really useful for freelancers in India or will it reduce conversions?

3DS adds a short authentication step, but it shifts liability for many fraud disputes away from you. For services, the slight friction is worth the protection. If your platform enforces 3DS by default, like Karbon Business payment links, you get lower fraud risk with minimal impact on completion rates.

Chargeback fee is more than my invoice, should I fight or accept?

If the disputed amount is small and you lack strong documentation, accept and move on, then fix your process. If the amount is significant and you have contracts, approvals, and delivery logs, fight. Always weigh your evidence strength against fees and time, and set a policy to avoid emotional decisions.

How do currency conversion and forex impact my chargeback losses?

You may receive funds at one INR rate, then lose them at a different rate when reversed, which can magnify your loss. Hold a buffer for four months after card payments, and consider platforms that let you hold foreign currency temporarily or accept local bank transfers to reduce forex exposure.

What documents should I always keep ready for international disputes?

Signed SOW, invoice, milestone approvals, delivery proof, communication logs, 3D Secure or AVS or CVV results, and e-FIRA. Store them for at least 13 months. Karbon Business automatically generates e-FIRA and keeps transaction histories accessible, which speeds up representment.

Are EU or US clients more likely to win chargebacks against Indian freelancers?

Cardholder protections are strong in EU and US, which means faster provisional credits, not guaranteed wins. Issuers still rely on evidence. If you provide clear scope, approvals, and delivery proof, you can win many consumer disputes regardless of the client’s region.

How to write a solid rebuttal letter for the bank as a freelancer?

Keep it one page, cite the reason code, list evidence in order, and map each item to the claim. Avoid emotional language, stick to dates, approvals, and delivery records. Many freelancers use platform support, Karbon Business offers quick guidance to format and submit correctly.

Can I avoid card rails completely for big projects and still get paid fast?

Yes, use ACH for US clients, SEPA for EU, and FPS for UK. With virtual USD, EUR, GBP accounts you can accept local transfers and settle to INR quickly. Karbon Business provides these accounts, plus e-FIRA for compliance, so you reduce chargeback risk and maintain speed.

Client paid via card then asked for refund, should I issue refund or wait for chargeback?

If the complaint is valid, issue a voluntary refund quickly, it saves fees and keeps your chargeback ratio healthy. Document the refund and send a credit note. If the complaint is not valid, explain your scope, offer reasonable support, and prepare evidence in case they file a chargeback.

What billing descriptor should I use so clients do not dispute as “unrecognized”?

Use your brand or service type, for example “YourName-UXDesign” or “YourStudio-WebDev.” Avoid generic gateway codes. Some platforms allow custom descriptors on payment links, configure this before sending a link.

Do I still need e-FIRA if it does not help the chargeback decision?

Yes, e-FIRA is essential for RBI and FEMA compliance, tax filings, and audit trails, even if issuers focus on delivery proof. It strengthens your documentation. Karbon Business auto generates e-FIRA within 24 hours, removing bank follow ups.

My dispute window says 45 days, can I wait till the last week?

Do not wait. Aim to submit within 7 to 10 days, weekends and holidays reduce your effective window, and evidence retrieval takes time. Set alerts and internal SLAs, and keep checklists ready so you do not scramble at the end.