Key takeaways

- App stores are the merchant of record, they collect money, deduct commission, convert currency, then send your net proceeds to India.

- Payouts typically land 45 to 60 days after the revenue month, plan your cash flow accordingly.

- Set up PAN, GSTIN, accurate bank details, and Apple’s W-8BEN to avoid holds and withholdings.

- Google’s base commission is 15% up to the first million dollars, subscriptions can drop to 10% in year two, and its alternative billing reduces fees by 4 percentage points.

- Apple’s Small Business Program charges 15% up to $1 million, then 30% on the rest, subscription fees can reduce after year one.

- Expect FX markups of roughly 1% to 2.5% and inbound wire fees from banks and intermediaries.

- Download e-FIRA for every inward remittance, it is your proof of foreign exchange, learn it with this e-FIRA guide.

- Ensure correct RBI purpose codes like P0802 purpose code for software services revenue.

- Build a two month runway, forecast payouts two months ahead, and keep documentation clean for taxes and audits.

- For direct client work, platforms like Karbon Business can speed up international collections with low fees and auto e-FIRA.

Understanding how app store payments flow to India

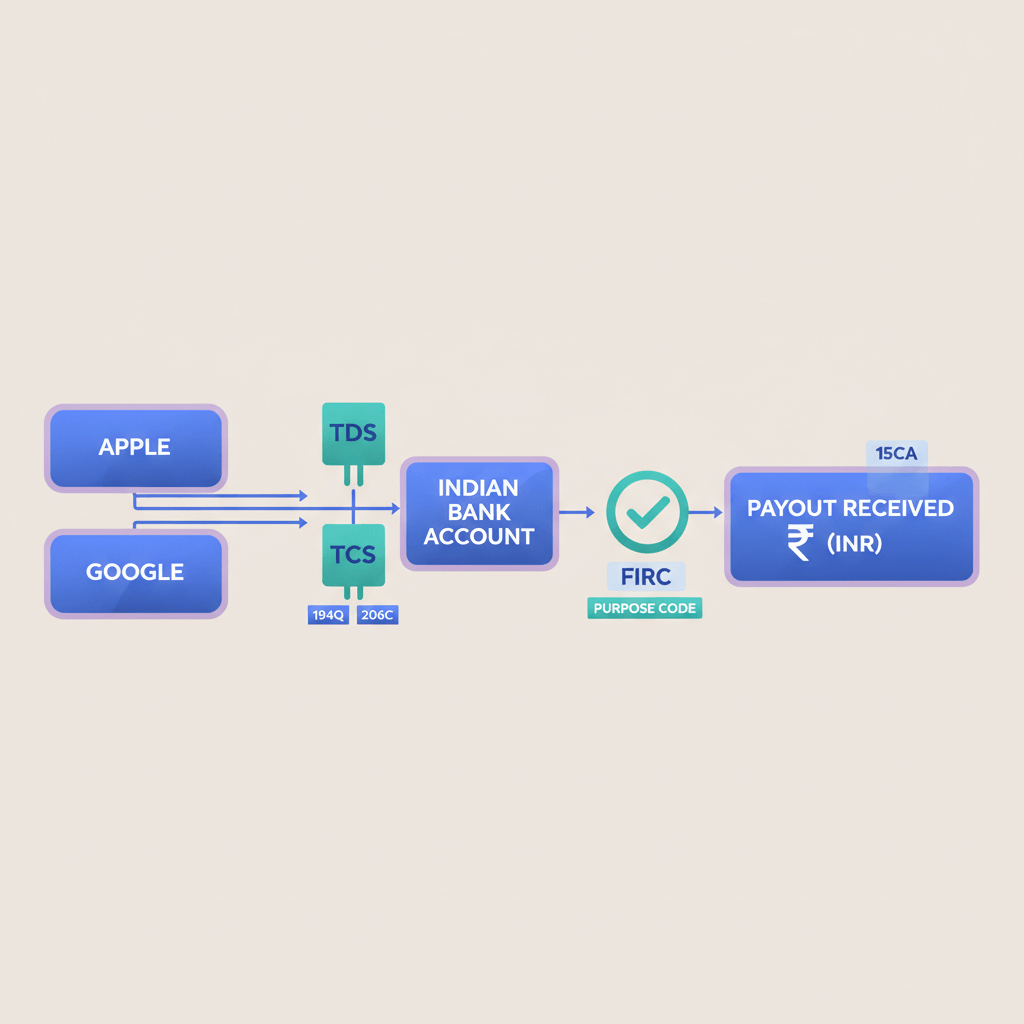

When a user purchases your app or an in-app item, Apple or Google acts as the merchant of record. They collect the payment, manage refunds, deduct their commission, then settle the net amount to you as an inward remittance into India. That remittance moves through SWIFT, gets converted to INR, and finally appears in your bank account.

Most developers see funds 30 to 60 days after the revenue month. Earn ₹50,000 in January, expect a credit in early March. This lag exists because of monthly batching, processing windows, cross border wires, and correspondent banks.

Treat app store payouts like a slow moving train, predictable once you understand the timetable, but not something you can rush.

Setting up your developer accounts to receive payouts

Required documents and information

- PAN as your tax identifier, required by both stores.

- GSTIN if registered, helpful for compliance and reconciliation.

- Bank details that match exactly, account name, account number, IFSC, branch address.

- For Apple, a valid W-8BEN, without this, Apple may withhold 30% for US taxes.

Pro tip: Names must match letter for letter with bank records, a single mismatch can bounce your payment and add another month of waiting.

Choosing the right bank account

Use an account that can receive international wires via SWIFT, confirm with your branch if needed. Many developers keep a dedicated business account for clean bookkeeping, easier GST returns, and audit readiness. Avoid third party or joint accounts that do not match your developer profile.

Google Play Store fees and payout process

Current commission rates

- 15% on the first $1 million per year, 30% beyond.

- Subscriptions are usually 15% in year one, then 10% from year two.

- With Google’s alternative billing, fees drop by 4 percentage points on eligible transactions.

Result, many Indian indie developers effectively operate at a 15% or 11% fee on most revenue, until they scale past $1 million.

The Indian context and timeline

Deadlines and policies shifted repeatedly in India. Google extended the Play Store deadline for India developers after regulatory pressure. The CCI dismissed interim relief pleas around billing challenges, while broader antitrust findings followed on other fronts. Despite the turbulence, the standout change remains the lower 15% slab for small developers, though many still felt it was not enough, as covered by this TechRadar piece.

How Google pays Indian developers

- Earnings are summed at month end, payouts start around the 15th of the next month.

- SWIFT wire typically arrives in 3 to 7 business days, expect late next month or early the following month.

- FX conversion uses Google’s rate, usually 1% to 2% over mid market, plus your bank’s inward remittance fee, commonly ₹250 to ₹750.

Apple App Store fee structure and payouts

Commission rates

Under the Small Business Program, Apple charges 15% on the first $1 million per calendar year, then 30% on the surplus. Long running subscriptions can reduce to 10% from the second year for continuing subscribers.

Payment schedule

- Monthly payouts usually around the 7th for the prior month.

- Minimum threshold of $150, short months roll forward.

- Wires land in 5 to 10 business days, with a contracted FX rate that commonly adds 1.5% to 2.5% over interbank.

Understanding the fees that reduce take home

App store commission

On ₹1,00,000 in gross, 15% leaves ₹85,000 before FX and banking costs. The commission buys global distribution, payments, and fraud handling, yet it materially shapes your margins.

Foreign exchange markup

If the mid market is ₹83 but you receive ₹81.50, that 1.5 difference is the markup. On $10,000, 2% is about ₹16,600, not a small line item. Timing payouts is limited, so plan conservatively.

Inward remittance and banking charges

Expect your bank’s fee, sometimes a small percentage service fee, and occasional intermediary deductions of $10 to $30 that arrive as unexplained shortfalls.

GST and tax implications

Exports of services are zero rated for GST, you still report them properly. Commissions and certain services can trigger GST conditions, speak with a CA who understands cross border digital services. Income tax applies on business profits, account for advance tax if relevant.

Compliance and documentation, FIRC and e-FIRA explained

What is FIRC?

A Foreign Inward Remittance Certificate confirms foreign currency was received and converted into your account. It lists sender, amount, purpose code, and date.

The shift to e-FIRA

RBI moved to digital advice, most banks issue e-FIRA automatically via net banking. Learn details in this practical e-FIRA guide. Download each PDF, keep it with your payout records.

Why you need this documentation

For tax filing, audits, export benefits, and RBI scrutiny, e-FIRA is your evidence. It feels like paperwork, but it protects you during compliance checks.

Purpose codes for app revenue

Ask your bank to use the right RBI code. For software or digital services, banks often use P0802 purpose code or P1001. Correct coding prevents reconciliation issues later.

Typical payout timeline, from sale to bank credit

Month 1, revenue accrual

January sales accumulate in your console, app stores pool the gross.

Month 2, processing and initiation

Mid February, stores deduct commission and start the wire. The payment enters SWIFT and moves through correspondent banks.

Month 2 to Month 3, international transfer

Expect 3 to 10 business days in transit, longer for first time or large value checks.

Month 3, credit to your account

Early March, INR credit arrives, your bank posts e-FIRA within 24 to 48 hours. Net result, about 45 to 60 days from earning to usable funds.

Managing cash flow when payouts are delayed

Strategies to smooth cash flow

- Maintain a two month runway of expenses as buffer.

- Bridge using consulting or retainers while app revenue is in transit.

- Consider a small credit line if growth demands upfront spend.

- Use milestone based contracts for services to reduce gaps.

Forecasting inward remittances

Track revenue by month, forecast cash arrival two months out, and align ad spend with payout timing. Spend in January, plan to see the INR only by March.

Visibility reduces stress, and it empowers better product and hiring decisions.

Tools and platforms to receive international payments efficiently

For direct client work, specialized platforms beat raw bank wires on cost, speed, and FX transparency.

- Karbon Business gives Indian developers USD, GBP, EUR, and CAD receiving accounts, flat 1% fee, zero FX markup at mid market, INR settlement in 24 to 48 hours, and automatic e-FIRA in 24 hours.

- Wise Business offers multi currency accounts with transparent fees and real rates.

- Payoneer supports receiving accounts in several currencies and marketplace integrations.

- PayPal is universal for clients, although fee heavy.

- RazorpayX International focuses on Indian businesses, feature availability varies.

Compare based on volume, currencies, need to hold balances, and appetite for FX risk management.

Common issues and how to troubleshoot them

Payout delayed beyond normal timeline

Check your console status first. If sent, ask your bank’s forex desk to trace using the SWIFT reference. Intermediary compliance checks can add a week, especially for first payments.

Incorrect bank details

Mismatched names or wrong IFSC causes bounce backs. Correct the info, then wait for the next cycle. Triple check before your first payout.

Missing or incorrect tax forms

For Apple, fix W-8BEN promptly to avoid 30% US withholding. If already withheld, you may need to file for a refund, which is slow, so prevention is key.

Exchange rate disputes

App stores set their rates contractually. Raise a support ticket if needed, but plan future cash flows assuming a 1% to 2.5% spread.

Tax obligations and record keeping for app developers

Income tax filing

Report under business income, keep bank statements, payout reports, and all e-FIRAs together. Cross verify gross, commission, and net.

Advance tax payments

If your profits are material, pay quarterly to avoid interest. A CA can help you estimate based on trailing twelve months revenue and growth.

GST compliance

Exports are zero rated, still file returns if registered. Claim eligible input credits on tools and services to reduce net tax outflow.

Maintaining proper documentation

Keep a single repository for e-FIRAs, bank credits, purpose codes, console statements, and vendor invoices. It pays off during audits and diligence.

Planning for growth, scaling your app business in India

When to formalize your business structure

Beyond ₹20 to 30 lakhs a year, consider a private limited or LLP for liability protection, easier financing, and better tax planning.

Hiring and payroll

Handle TDS, PF, and professional tax properly. Outsource payroll if it saves time and reduces compliance risk.

Expanding payment options for users

Localize payment methods to lift conversions, UPI and local cards in India, country specific methods abroad. This does not change store payouts, but it helps if you sell directly via web or SaaS.

Comparing app store payouts with direct client payments

Pros of app store payouts

- Global reach, fraud handling, chargebacks managed for you.

- No chasing invoices, automated monthly settlement.

Cons of app store payouts

- High commissions versus direct rails.

- No control over payout timing.

- Opaque FX, usually worse than specialized providers.

When direct payments make sense

For high value projects, negotiate milestones and use a platform like Karbon Business to receive locally in client currency, settle to INR fast, and auto generate e-FIRA, which lifts margins and reduces admin.

Building a sustainable financial foundation

Financial systems to put in place early

- Dedicated business bank account for clean books.

- Use Zoho Books, Tally, or QuickBooks for accurate P and L and reconciliations.

- Set aside 30% of net receipts for taxes to avoid surprises.

Working with a chartered accountant

A CA with digital and cross border expertise pays for itself, through accurate filings, better structure, and fewer compliance headaches.

Continuous learning and adaptation

Regulations and store policies evolve. Review agreements annually, subscribe to RBI updates, and revisit your payment stack as you scale.

What worked at ₹50,000 a month may not be optimal at ₹5,00,000 a month.

Final thoughts, take control of your app revenue

Payouts need not be a black box. Once you understand the timeline, commissions, FX, and documentation, the process becomes routine. Focus on building great products, while your financial ops run predictably in the background.

Minimize fees where you can, remain compliant, and choose tools that respect your time and margins. Every rupee saved in FX or remittance is a rupee you can reinvest in your next release, your team, or your growth roadmap.

FAQ

How long does Google Play or Apple take to pay Indian developers, and why is it so delayed?

Most developers see funds in 45 to 60 days because stores batch monthly, process settlements, convert currency, then send SWIFT wires that can take a week in transit. Plan expenses two months ahead to stay comfortable.

Which is better for cash flow, Google Play or Apple payouts for India?

Both run monthly cycles with similar timelines, Apple often triggers around the 7th and Google around mid month. The bigger difference is FX rate and bank fees, so monitor the effective INR you receive rather than the brand label.

Can I reduce app store commissions as an Indian developer, especially on Google Play?

You benefit from the 15% slab up to $1 million, subscriptions can drop to 10% after year one, and Google offers an alternative billing path that trims fees by 4 percentage points on eligible transactions. Evaluate policy fit before implementing.

What documents do I need to start receiving payouts in my Indian bank account?

PAN, GSTIN if registered, accurate bank details, and for Apple a valid W-8BEN. Keep your bank account name exactly matching your developer profile to avoid bounce backs.

What is e-FIRA and do I really need it for every app store payout?

e-FIRA is your bank’s electronic advice confirming foreign inward remittance. Yes, download it for every payout, it supports GST filings, income tax, audits, and any RBI queries. It is quick to fetch via net banking on most banks.

Which RBI purpose code should my bank use for app store remittances?

Typically P0802 for software services, sometimes P1001 for other business services. Ask your bank to tag it correctly, it helps during reconciliation and compliance checks.

How do Indian freelancers or indie developers manage the 60 day wait for money?

Maintain a two month buffer, forecast receipts two months out, and consider a working capital line if you are scaling. Many devs pair app income with consulting retainers to smooth cash flow.

Is there a faster and cheaper way to receive international client payments than direct bank wires?

Yes, platforms like Karbon Business provide local receiving accounts in USD, GBP, EUR, and CAD, charge a flat 1% fee, settle INR in 24 to 48 hours, and auto issue e-FIRA, which is often faster and cheaper than traditional wires.

Do I need a company to receive international payments, or can I use a personal account?

You can start as a sole proprietor, but use a dedicated account that accepts SWIFT wires. As you cross ₹20 to 30 lakhs a year, consider a private limited or LLP for cleaner compliance and better tax planning.

How much money do banks and FX markups actually eat from my payout?

Expect 1% to 2.5% FX spread plus ₹250 to ₹750 bank fees, and occasional intermediary fees of $10 to $30. Over a year, this adds up, which is why developers compare options that give mid market rates.

What if Apple withheld 30% due to a missing W-8BEN, can I recover it?

Submit a correct W-8BEN immediately to stop future withholding, then consult a tax professional about reclaiming past amounts, the process can be lengthy, so prevention is best.

For client projects, why do many Indian freelancers prefer Karbon Business over PayPal or raw SWIFT?

Because Karbon Business offers mid market FX with zero markup, flat 1% fee, INR in 24 to 48 hours, and automatic e-FIRA. PayPal is convenient but fee heavy, raw SWIFT can be slow with opaque deductions, so freelancers optimize for speed, cost, and compliance.