Key takeaways

- Withholding tax means your client deducts tax before paying you, in India this is TDS for domestic clients, foreign clients follow their own country’s rules modified by tax treaties.

- Indian freelancers typically face TDS under Sections 194J, 194C, 194H, and 194M, always share your PAN or Section 206AA can force a 20% deduction.

- For foreign clients, submit treaty documents like W-8BEN for US, a Tax Residency Certificate and Form 10F to claim DTAA benefits, often resulting in zero withholding.

- If foreign tax gets deducted, claim Foreign Tax Credit in India via Form 67 before filing your ITR, attach 1042-S or similar certificates.

- Reconcile Form 26AS and AIS regularly, collect Form 16A, pay advance tax on time, and file ITR by the due date to avoid interest and higher TDS rates under Section 206AB.

- Export services are zero-rated under GST, file a Letter of Undertaking to avoid paying IGST upfront, maintain e-FIRA for proof of inward remittance.

- Use compliant payment solutions like Karbon Business for fast INR settlement, local currency accounts, and auto e-FIRA, which simplifies documentation.

Why Withholding Tax Confuses Indian Freelancers

Picture this, Rahul in Bangalore sends a ₹1 lakh invoice, his Indian client deducts 10% TDS under Section 194J, then a US client asks for W-8BEN to avoid 30% withholding. Both feel like money leaving your invoice before you get it, yet they are governed by different rules and reliefs.

Withholding is a global concept, TDS is the Indian mechanism for domestic payments, tax treaties handle cross-border relief.

In India, resident clients deduct TDS under specific sections of the Income Tax Act. Foreign clients apply their country’s withholding laws, though Double Taxation Avoidance Agreements, DTAA, typically reduce or eliminate withholding if you work from India without a permanent establishment abroad.

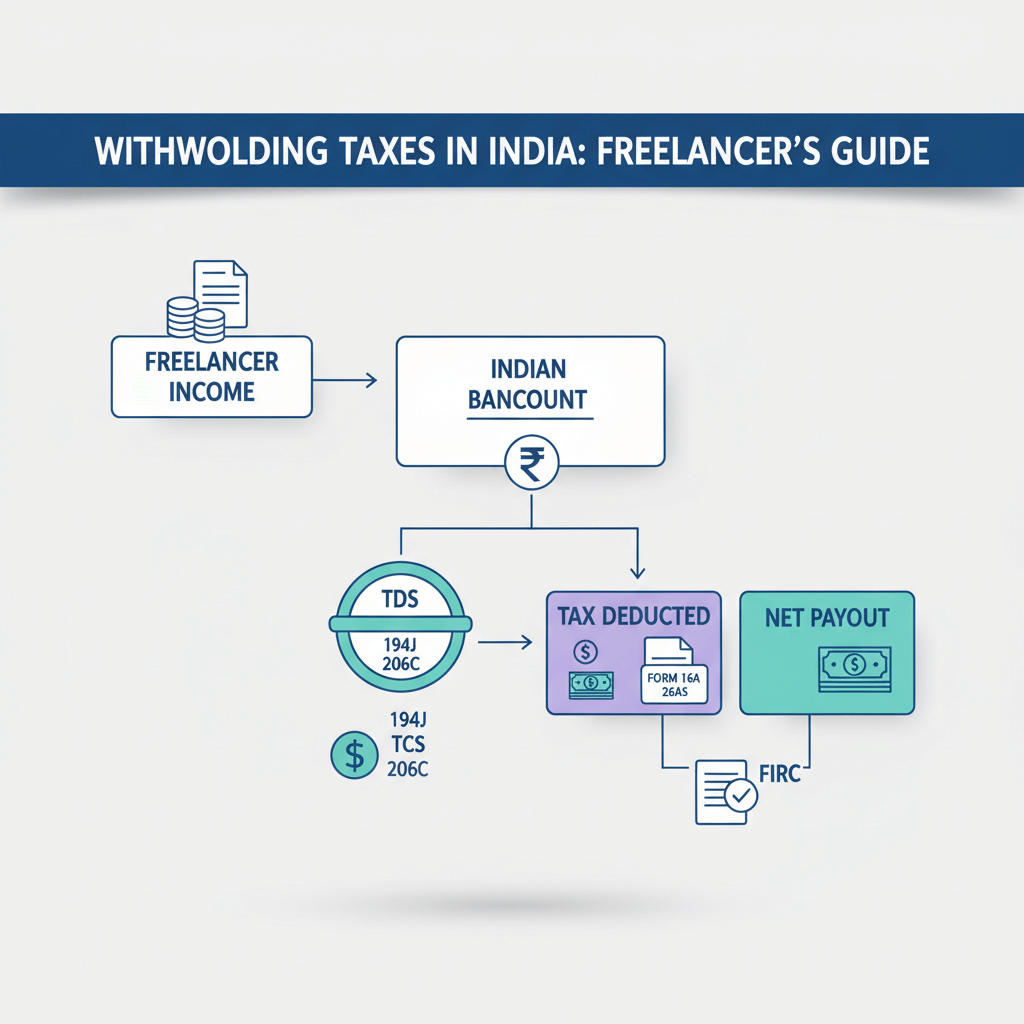

TDS for Freelancers, Understanding Domestic Withholding

TDS is advance tax collection, not a penalty. Deductions get credited to your PAN, visible in Form 26AS and AIS, and you claim these credits in your ITR. If deducted amounts exceed your final tax, you receive a refund.

Common TDS Sections and Rates for Freelancers

- Section 194J, professional and technical services, common for developers, designers, consultants, writers, and marketers, 10% on payments exceeding ₹30,000 per client per year.

- Section 194C, contract work, 1% if payer is an individual or HUF, 2% for companies, thresholds ₹30,000 single payment or ₹1 lakh aggregate.

- Section 194H, commission and brokerage, 5% above ₹15,000 aggregate per year.

- Section 194M, payments by individuals or HUFs not subject to audit, 5% if their aggregate payments to contractors and professionals exceed ₹50 lakh in a year.

- Section 206AA, no PAN, 20% TDS applies regardless of section.

- Section 206AB, higher TDS for specified persons who have not filed returns, file your ITR on time.

How TDS Appears in Your Records

Check Form 26AS quarterly, reconcile with Form 16A from clients, review AIS for more details. Pay advance tax on time, 15% by June 15, 45% by September 15, 75% by December 15, 100% by March 15 if your estimated liability exceeds ₹10,000.

Presumptive taxation under Section 44ADA lets professionals with receipts up to ₹50 lakh declare 50% as taxable income, TDS credits still offset your final tax.

Fixing Common TDS Problems

- Wrong section used, ask for a corrected Form 16A, claim credit anyway in ITR if needed.

- No PAN shared, push rates to 20%, share PAN immediately, claim excess via ITR.

- Expect low tax, apply for a lower or nil deduction certificate under Section 197 to improve cash flow.

TDS is tax you already owe, collected early, organize your records and you will get every rupee back through credits or refunds.

Withholding Tax on Cross-Border Payments from Foreign Clients

Foreign clients follow their country’s withholding rules, yet India’s treaties often reduce withholding to zero when you work from India and have no permanent establishment abroad.

Typical Scenarios by Client Location

- US clients, submit W-8BEN with your PAN, under India US DTAA, independent services performed from India usually face 0% withholding. Marketplaces often require W-8BEN to avoid 30% default withholding.

- UK and EU clients, commonly no withholding on exported services, confirm country specific rules as needed.

- Singapore, Australia, and other DTAA countries, provide treaty documents like TRC and Form 10F to apply reduced or nil withholding.

How to Use DTAAs Effectively

A treaty decides which country can tax your income. For independent services, taxing rights typically lie with India, your residence country, if you keep work in India and have no foreign fixed base.

- Obtain a Tax Residency Certificate, prove Indian tax residency for the year.

- Prepare Form 10F, client may request it to apply treaty benefits.

- Submit W-8BEN for US clients, other countries have similar forms.

- Keep proof that services were performed from India, contracts, emails, delivery logs.

Claiming Foreign Tax Credit If Tax Is Withheld

If foreign withholding happens, file Form 67 before your ITR, attach foreign tax certificates like 1042 S, payment proof, and bank statements, convert to INR using RBI reference rate for the payment date. FTC reduces Indian tax rupee for rupee, up to tax due on that foreign income.

Withholding Rules India, Quick Reference Table

| Scenario | Withholding Treatment |

|---|---|

| Indian resident client → Indian resident freelancer | TDS under Sections 194J, 10%, 194C, 1 to 2%, or 194H, 5%, based on work type and thresholds, PAN required or 20% under Section 206AA, reconcile via Form 26AS, claim in ITR. |

| Non resident foreign client → Indian resident freelancer | No Indian TDS at source by the foreign client, foreign withholding depends on their laws, apply DTAA using TRC, Form 10F, W-8BEN, claim FTC via Form 67 if withholding still happens. |

Getting Paid Smoothly, Practical Invoice and Contract Tips

- Share PAN early, ask which TDS section applies to budget net receipts.

- Add a gross up clause for large contracts, client bears any withholding so you receive the agreed net amount.

- Collect documents, invoices, contracts, Form 16A, foreign tax certificates, TRC, Form 10F, payment receipts, bank statements.

- Use compliant channels, Karbon Business offers USD, GBP, EUR, and CAD virtual accounts, local transfers like ACH or SEPA, INR settlement in 24 to 48 hours, zero FX markup, mid market rates, a flat 1% platform fee, and auto e FIRA for RBI compliance.

- Alternatives include Wise Business, Payoneer, PayPal, RazorpayX International, and WorldFirst, compare fees and settlement times.

Withholding Tax Calculations, Real Freelancer Examples

Example 1, Domestic TDS, Section 194J

You invoice ₹1,00,000 in June, client deducts 10% TDS under Section 194J.

- Invoice, ₹1,00,000

- TDS, ₹10,000

- Amount credited, ₹90,000

Form 16A and Form 26AS show the credit, if your final tax is ₹25,000 and you paid ₹15,000 advance plus ₹10,000 TDS, you break even. If your tax is lower, expect a refund.

Example 2, US Client with DTAA Relief

Invoice $3,000 for services delivered from India, submit W-8BEN in advance, DTAA applies, withholding is 0%, you receive the full amount. If W-8BEN was not submitted, 30% withholding occurs, client issues 1042 S for $900 withheld, file Form 67 in India to claim FTC, limited to Indian tax due on that income.

Refunds, Reconciliations, and Key Deadlines

- Review Form 26AS and AIS monthly or quarterly, match Form 16A and invoices, fix mismatches fast.

- Advance tax schedule, June 15, 15%, September 15, 45%, December 15, 75%, March 15, 100%, interest applies for short or late payment.

- ITR due date, July 31 for non audit cases, October 31 if audit applies.

- Form 67 for FTC must be filed before ITR, upload foreign tax certificates and proofs.

- e FIRA is auto issued within 24 hours for foreign inward remittances, critical proof for GST refunds and export income, Karbon Business provides auto e FIRA.

- GST compliance, register at ₹20 lakh turnover, export services are zero rated, file LUT to export without paying IGST, keep contracts and bank proofs.

Common Withholding Mistakes Freelancers Make and Quick Fixes

- Wrong TDS section, ask for a corrected Form 16A, claim credit anyway in ITR.

- No PAN given, 20% TDS applies, share PAN, claim excess via ITR.

- Ignoring DTAA, submit TRC, Form 10F, W-8BEN early.

- 26AS mismatch, wait for the quarter, then request challan and TDS return acknowledgment, file corrections.

- No reconciliation before ITR, always review 26AS and AIS, use portal correction requests.

- Missed Form 67, you cannot claim FTC after ITR, file Form 67 as soon as foreign tax certificate arrives.

GST and Compliance for Freelancers Providing Export Services

Income tax and TDS matter, yet GST is equally important for service exports.

- GST registration threshold, ₹20 lakh turnover, ₹10 lakh in special category states.

- Zero rated exports, invoice foreign clients without GST, still claim input tax credit.

- File a Letter of Undertaking to export without paying IGST upfront.

- Return filing, report export invoices in GSTR 1, claim credits in GSTR 3B.

- Documentation, contracts, invoices, delivery proof, bank statements, e FIRA for inward remittance proof.

- Tax audit readiness, keep clean books, consider a CA review annually.

Your Action Checklist, Taming Withholding Tax India

For Indian clients:

- Share PAN early, confirm applicable TDS section.

- Collect Form 16A and reconcile with Form 26AS and AIS.

- Apply for Section 197 lower or nil deduction certificate if liability is low.

For foreign clients:

- Obtain a Tax Residency Certificate, prepare Form 10F, submit W-8BEN where applicable.

- State performance location as India, confirm no foreign permanent establishment.

- Add a gross up clause for large engagements.

- Use Karbon Business or similar platforms for local currency receiving, fast INR settlement, and auto e FIRA.

Documentation:

- Maintain client wise folders, contracts, invoices, Form 16A, foreign tax certificates, TRC, Form 10F, W-8BEN copies, bank statements.

- Back up to cloud, label clearly by client, financial year, and document type.

Filing and compliance:

- Review 26AS and AIS monthly.

- Pay advance tax by all four deadlines if liability exceeds ₹10,000.

- File Form 67 before ITR for FTC claims.

- File ITR by July 31, or October 31 if audit applies.

- Register for GST at ₹20 lakh turnover, file LUT, and returns for zero rated exports.

Ongoing habits:

- Negotiate and review withholding clauses.

- Update clients if PAN or bank details change.

- Consult a chartered accountant annually, track Finance Act changes.

- Monitor DTAA updates and RBI guidelines for foreign payments.

Conclusion, Confidence Over Confusion

Withholding tax India becomes simple once you separate domestic TDS from foreign client withholding and apply the right treaty documents. Share PAN, reconcile statements, and use Section 197 when cash flow is tight. For foreign work, submit W-8BEN, TRC, and Form 10F early, claim FTC via Form 67 if needed, and keep solid documentation like e FIRA.

Smart contracts, clean records, and compliant payment solutions such as Karbon Business reduce friction, speed up settlement, and keep your exports audit ready. Laws evolve, consult a qualified CA for tailored advice as your income grows, and use the checklist above to stay organized, confident, and compliant.

Disclaimer, this guide is general information, not tax advice, consult a chartered accountant for your specific situation.

FAQ

How can I stop a US client from cutting 30% withholding on my freelance invoices?

Submit Form W 8BEN with your Indian PAN before the first payment, certify Indian tax residency, and rely on the India US DTAA which generally brings withholding to 0% for independent services performed from India. If any withholding still happens, claim Foreign Tax Credit in India via Form 67. Platforms like Karbon Business help you keep documentation organized for smooth filing.

Is TDS and foreign withholding the same thing for Indian freelancers?

No, TDS is India’s domestic withholding on payments from resident clients, foreign withholding comes from the client’s country laws. DTAAs usually reduce or eliminate foreign withholding when you work from India, while TDS credits show up in your Form 26AS and are claimed in your ITR.

What documents should I give my foreign client to apply treaty benefits quickly?

Provide a Tax Residency Certificate, Form 10F, and country specific forms like W 8BEN for US clients. State clearly in the contract that services are performed from India, with no foreign permanent establishment. Keep copies in a client folder, Karbon Business users often maintain these alongside auto e FIRA for inward remittance proof.

How do I claim Foreign Tax Credit if withholding already happened on a payout?

File Form 67 on the income tax portal before your ITR, attach foreign tax certificates like 1042 S, payment proofs, and bank statements, convert to INR using RBI reference rate for the payment date. You receive FTC limited to Indian tax on that foreign income, any excess foreign tax beyond India’s tax cannot be refunded.

My Indian client deducted TDS under 194C, but I am a designer, should it be 194J?

Design and other professional services typically fall under Section 194J, 10%. Request a corrected Form 16A and ask the client to file a correction statement, you can still claim the credit in your ITR, however proper section classification keeps records clean and reduces scrutiny.

Can I avoid cash flow issues if my tax liability is low for the year?

Yes, apply for a lower or nil deduction certificate under Section 197, once issued, share it with your clients so they deduct at the specified lower rate, this improves cash flow because you do not wait for refunds later.

Do I need to charge GST to foreign clients for exported services?

No, exports are zero rated. File a Letter of Undertaking to export without paying IGST upfront, then file regular GST returns showing export invoices, maintain e FIRA and bank statements as proof of foreign inward remittance.

What is e FIRA, and is it enough for compliance during audits?

e FIRA is electronic Foreign Inward Remittance Advice, auto generated for each foreign inward remittance, it is key evidence for export income, GST, and tax filings. Using Karbon Business gives you auto e FIRA within 24 hours, which saves follow ups with banks and supports audit trails.

Which platform is best to receive international payments in India with low fees and fast settlement?

Compare options by fees, FX markup, settlement speed, and compliance. Karbon Business offers local currency accounts in USD, GBP, EUR, CAD, INR settlement in 24 to 48 hours, zero FX markup with mid market rates, a flat 1% platform fee, and auto e FIRA. Alternatives include Wise Business, Payoneer, PayPal, RazorpayX International, and WorldFirst.

How should I organize documents for TDS and DTAA, so ITR filing is smooth?

Maintain a client wise folder with contracts, invoices, Form 16A, Form 26AS and AIS snapshots, TRC, Form 10F, W 8BEN, foreign tax certificates like 1042 S, and bank statements. If you receive through Karbon Business, include auto e FIRA for each inward remittance, this makes Form 67 and ITR preparation straightforward.

What happens if I forget to file Form 67 before ITR for FTC?

FTC cannot be claimed if Form 67 is filed after your ITR. As soon as you receive foreign tax documentation, file Form 67, then submit your ITR. If you miss it, you may end up paying full Indian tax on that income despite foreign tax already withheld.

If I work from India for a US startup, will they still add VAT or sales tax in my payment?

No, US sales tax or EU VAT do not apply to your exported services performed from India, however US payers may withhold tax unless you provide W 8BEN and apply DTAA. Ensure your contract clarifies service location as India, keep TRC and Form 10F ready, and use platforms like Karbon Business for clean payment trails.