Key takeaways

- DTAA lets Indian freelancers avoid paying income tax twice on the same foreign earnings, you either get zero or reduced foreign withholding, then pay tax only once in India with credit for any tax paid abroad.

- Your essential DTAA pack is simple, a Tax Residency Certificate, Form 10F, a no permanent establishment declaration, plus the right payer form like W-8BEN for US clients.

- Share these documents with the client before your first invoice so withholding is waived or reduced at source, if tax is still withheld, claim Foreign Tax Credit in India via Form 67.

- Most freelance income is business profits under treaties, if you have no PE abroad, the client’s country usually should not tax you, US and UK “make available” tests often push services out of FTS and back to business profits.

- File Form 67 before or with your ITR to claim FTC, without it, you can lose the credit and overpay tax.

- A payment partner that provides fast e-FIRA, unified statements, and stores compliance docs reduces friction, platforms like Karbon Business add INR settlement speed and zero FX markup.

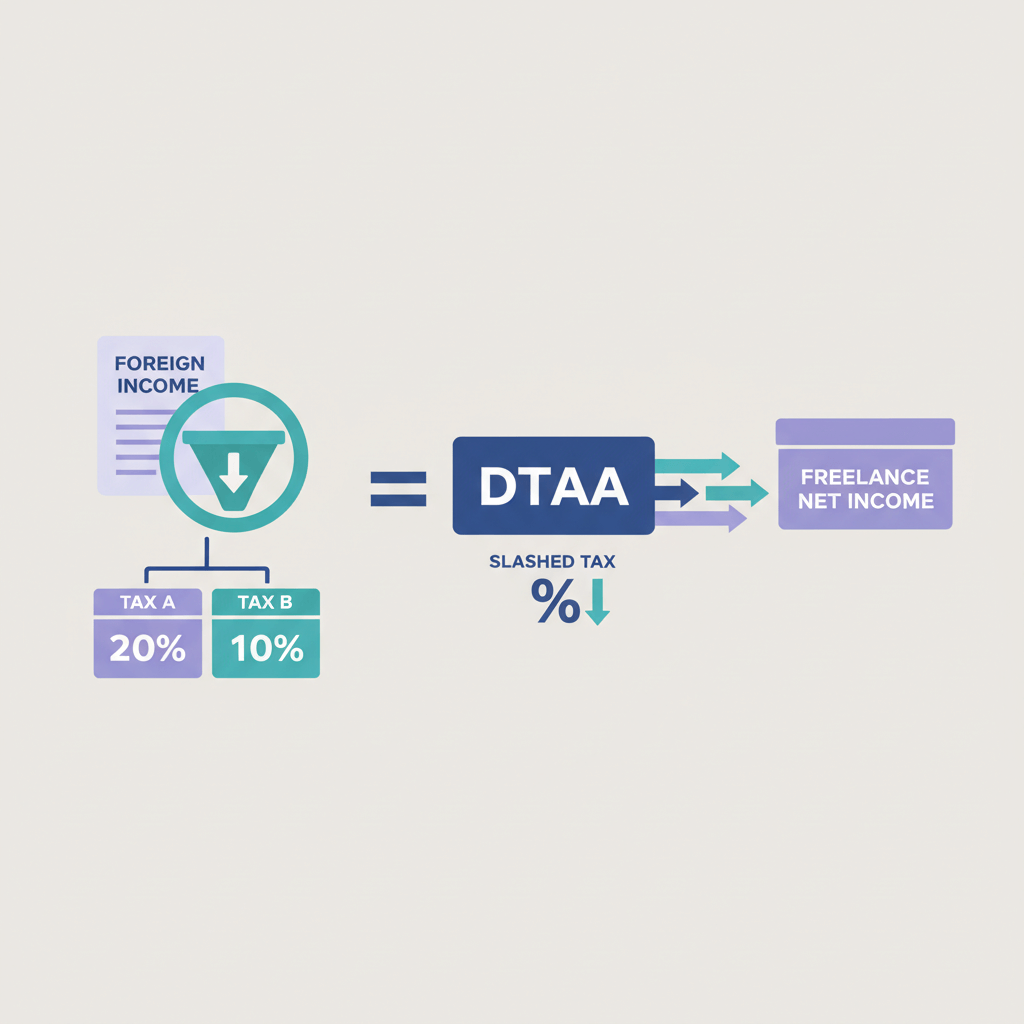

DTAA for Freelancers in India, how it works to stop double taxation from foreign clients

Invoice a US client for five thousand dollars, they may withhold ten to thirty percent under their local rules, then India taxes the same income again. That is double taxation, and it silently drains your margins. The solution is DTAA, a treaty framework that decides which country can tax your freelance income, and ensures you pay tax only once, typically at your Indian rate.

With the right documents in place, your foreign client can pay you gross, or at a reduced withholding rate, and any tax deducted abroad becomes a credit against your Indian tax using Form 67. For a practical explainer, read how NRIs can claim benefits under DTAA, and a field guide tailored to solo service providers here, DTAA for freelancers.

What DTAA is, and why Indian freelancers should care

DTAA is a treaty between India and other countries that prevents the same income from being taxed twice. It clarifies taxing rights between the source country, your client’s country, and the resident country, India for most freelancers, then offers relief through exemption or foreign tax credit.

Resident country versus source country

Your resident country is where you are taxed on worldwide income, India for most freelancers. The source country is where the client is based. DTAA determines who gets to tax your freelance service income, and how relief works when tax is paid abroad.

Permanent establishment, the PE question

PE means a fixed place of business in the client’s country, an office, a fixed desk, or a dependent agent. If you have no PE and you deliver services from India, business profits are typically taxable only in India under most treaties.

Business profits versus fees for technical services

Most freelance work is business profits. Some treaties define fees for technical services, but US and UK treaties include a “make available” test, if your work does not transfer know how that enables the client to perform it independently, it is not FTS. Designers, content writers, most developers, and consultants usually fall back to business profits.

Withholding tax, what clients try to deduct

Foreign payers may withhold by default. Your job is to prove Indian residency and no PE, so they either do not withhold, or apply treaty reduced rates. That proof is your TRC, Form 10F, a no PE declaration, and any payer specific form like W-8BEN.

The numbers behind DTAA

Ignorance is expensive. Many freelancers overpay by tens of thousands of rupees each year. With proper DTAA use, foreign withholding drops to zero or a small rate, then you pay Indian tax once. If tax was deducted abroad, you claim FTC in India so your total tax does not exceed what you would have paid in India anyway.

How DTAA works for freelancers, step by step

Step 1, confirm you are an Indian tax resident

If you spend one hundred eighty two days or more in India during the financial year, you are a resident, your global income is taxable in India, and you can use DTAA.

Step 2, find the India–client country treaty

Search for the specific treaty and note the business profits article, the FTS article if any, reduced rates, and the PE definition.

Step 3, map your service to the right article

Freelance services usually fall under business profits, not FTS, especially where “make available” applies. No PE abroad means taxation in India only.

Step 4, share documents before your first invoice

Send your TRC, Form 10F, a short no PE declaration, and the country form like W-8BEN to the client’s finance team. Ask them to confirm no or reduced withholding.

Step 5, if tax is withheld anyway, claim FTC via Form 67

File Form 67 online before or with your ITR, attach proofs, and offset Indian tax by the foreign tax paid, limited to the Indian tax on that income.

Fast flow to remember

Invoice → Share TRC, 10F, no PE, W-8BEN → Client waives or reduces withholding → If any tax withheld, file Form 67 for FTC in India.

The essential DTAA documents you need

Tax Residency Certificate, TRC

The IT Department issues the TRC as the official proof that you are an Indian tax resident for a stated period. It should show your name, PAN, address, and the covered financial year. Apply via Form 10FA, receive Form 10FB, allow two to four weeks, apply early each year.

Form 10F

Form 10F complements the TRC with additional residency particulars often requested by foreign payers. Download from the e filing portal, fill and keep on file with your TRC.

Self declaration of no permanent establishment

A short signed letter that you have no fixed place of business, or dependent agent, in the client’s country, and that services are delivered from India. Clients rely on this to apply treaty relief.

W-8BEN for US clients

For US payers, W 8BEN is mandatory. Fill your name, address, country of tax residence, cite the treaty article for business profits or independent personal services, sign and date. Valid for three years.

Supporting proofs to retain

Keep invoices, bank credits or e FIRA, client withholding certificates or platform statements. These back your Form 67. To cut leakage on deductions, see this primer on how to minimise TDS on foreign payments.

How to obtain a TRC in India, quick process

- Eligibility, you are usually resident if you spent at least one hundred eighty two days in India during the year.

- Apply, log in to the e filing portal, submit Form 10FA with your PAN, address, and the FY period.

- Issuance, Form 10FB is generated after verification, download multiple copies.

- Timeline, two to four weeks is common, apply in April or May to stay ahead.

Claiming DTAA with foreign clients, real life workflow

Onboarding the client

Add a line in your contract, “Payments are subject to the DTAA between India and the client’s country, the freelancer is a resident of India with no PE in that country, withholding should follow treaty rules.”

Then send an email to the finance team with TRC, Form 10F, no PE letter, and the payer form. Ask them to confirm no or reduced withholding before the first invoice.

Invoice note you can paste

“Subject to India–[Country] DTAA. No withholding required, per Article [X] business profits, income is taxable only in India. TRC and supporting documents available on request.”

How DTAA relief is calculated, simple examples

Two common outcomes

- Exemption at source, client pays the full amount with zero withholding, you pay Indian tax on the full receipt.

- Reduced withholding plus FTC, client withholds at a lower treaty rate, you claim FTC in India, total tax equals your Indian liability on that income.

Example 1, no withholding

Invoice five thousand dollars, client pays full, you report the INR equivalent as business income and pay Indian tax once.

Example 2, withholding plus FTC

Invoice five thousand dollars, fifteen percent withheld abroad, you still report the gross in India and claim FTC via Form 67, your total tax equals the Indian tax that would have been due on that income. For a primer on concepts, see this note on double taxation.

Filing in India, how to secure your Foreign Tax Credit with Form 67

- When, file Form 67 online before or with your ITR deadline.

- How, enter country, gross income, tax paid, dates, currency and exchange rate, attach proofs, submit and save the acknowledgment.

- Proofs, withholding certificate, bank statement or e FIRA, TRC, Form 10F, invoices, and any payer form you filed.

Important, FTC is capped at the Indian tax on that income, you cannot claim more credit than your Indian liability.

Treaty nuances freelancers should check

US and UK, the “make available” test

Most freelance services do not “make available” technical knowledge, so they are treated as business profits. If you have no PE, taxation lies in India, and US withholding can be zero when W 8BEN is on file and the treaty article is cited correctly.

Treaties with FTS and higher source withholding

Some older treaties apply higher FTS rates at source, if withheld, claim FTC in India and your total tax will not exceed the Indian tax on that income.

Common mistakes that cost money, and how to avoid them

- Missing or mismatched TRC period, client rejects treaty relief, always obtain a TRC for the same FY as the services delivered.

- Forgetting Form 10F or W 8BEN, default withholding applies, send both before the first invoice.

- Not filing Form 67, you lose FTC, file it before or with your ITR.

- Creating PE risk by long onsite stints, extended presence or a fixed desk abroad can trigger PE, keep trips short and documented as occasional.

- Misclassifying services as FTS, most freelance work is business profits, check the treaty and document your position.

- Not collecting withholding certificates, without proof, FTC can be denied, request certificates or platform statements every quarter.

Practical checklist you can copy

- Read the India–client country DTAA, note business profits, FTS, and PE rules.

- Get your TRC for the current FY, prepare Form 10F and a no PE declaration.

- Complete payer forms, W 8BEN for US, equivalents elsewhere.

- Email the finance team with all documents, ask for written confirmation of no or reduced withholding.

- Add a DTAA note to every invoice, save bank credits and e FIRA, collect withholding certificates if any.

- At year end, file ITR and Form 67 with all proofs attached.

How a payment partner reduces DTAA paperwork friction

Operational gaps, not just tax rules, create most headaches. Look for centralized storage of compliance docs, automated e FIRA within twenty four hours, unified statements per currency, fast INR settlement, and competitive FX so your books match your invoices. Karbon Business provides flat one percent platform fee, zero FX markup, automatic e FIRA, local USD, GBP, EUR, and CAD receiving details, and twenty four to forty eight hour INR settlement, which makes Form 67 reconciliation fast and clean.

Compliance disclaimer

This article is educational. Always verify the specific India–country DTAA article, confirm residency and PE facts, and file Form 67 and your ITR with a qualified CA. Laws change, facts differ, documentation is critical.

Final thoughts

Double taxation is avoidable. Secure your TRC, share your DTAA pack before invoicing, cite the right treaty article, and file Form 67 on time. Do this once, then templatize it, and you will keep more of every foreign dollar you earn.

FAQ

How can I avoid double taxation if I am an Indian freelancer billing US clients?

Share a DTAA pack before your first invoice, TRC, Form 10F, a no PE declaration, and W 8BEN citing the business profits or independent personal services article, ask the client to apply zero withholding. If any tax is deducted, file Form 67 and claim FTC in India. Payment partners like Karbon Business help by generating e FIRA quickly for Form 67 support.

Is W-8BEN mandatory for Indian freelancers receiving money from US companies on contract?

Yes, US payers rely on W 8BEN to confirm you are not a US taxpayer and to apply treaty benefits. Combine W 8BEN with your TRC, Form 10F, and a no PE declaration for smooth zero or reduced withholding. Keep copies in your records and refresh W 8BEN every three years.

What documents do I need to give my UK or EU client to stop withholding on my invoices?

Provide your Indian TRC, Form 10F, a brief no PE declaration, and any country specific form the payer requests. Reference the business profits article in correspondence. Ask for written confirmation from their finance team that no or reduced withholding will apply from the first payment.

Client already deducted tax on Upwork or direct wire, how do I claim it back in India?

Collect a withholding statement or certificate from the client or platform, then file Form 67 online before or with your ITR. Enter gross income, tax withheld, and exchange rate, attach TRC, invoices, and e FIRA. Your Indian tax is reduced by the foreign tax paid, limited to the Indian tax on that income.

Do I need TRC and Form 10F even if I am getting paid via PayPal or Payoneer?

Yes, your DTAA eligibility depends on residency and PE status, not the payment rail. Keep TRC and Form 10F ready, share them with clients or platforms if requested, and save platform tax statements to support Form 67. For faster documentation like e FIRA and unified statements, consider Karbon Business.

What is the deadline for filing Form 67 for Foreign Tax Credit in India?

File Form 67 before or along with your ITR by the applicable due date. If you miss it, the FTC can be denied, and you may overpay Indian tax despite foreign withholding. Set a calendar reminder a few weeks before your ITR filing.

Which exchange rate should I use when claiming FTC for DTAA in Form 67?

Use the RBI reference rate or the rate evident from your bank credit on the date of receipt, then keep a consistent policy and document it. Attach the bank advice or e FIRA for that transaction to support the rate you used.

Will short business travel to the client’s office create a permanent establishment risk for me?

Short, occasional visits usually do not create PE, but extended, regular presence, a fixed desk, or a dependent agent can. Keep trips brief, avoid fixed facilities abroad, and document services as delivered from India. If you expect long onsite work, get a CA to assess treaty PE thresholds.

Does DTAA have anything to do with GST on export of services?

No, DTAA is about income tax, while GST is an indirect tax. Export of services is typically zero rated under GST, so you do not charge GST to foreign clients. Handle GST and DTAA as separate compliance tracks with your accountant.

Is Karbon Business a good option for receiving international client payments as a freelancer in India?

Yes, if you want quick INR settlement, zero FX markup, and clean documentation for taxes, Karbon Business offers local currency receiving accounts, automatic e FIRA, and unified statements that make Form 67 prep easier. Many freelancers prefer this over piecing together statements from multiple tools.

How do I calculate Foreign Tax Credit if USD to INR moved between invoice and payment dates?

Compute FTC on the INR value you report as income, generally using the rate on the date of receipt or an accepted reference rate. Keep the rate source, bank advice, and e FIRA attached to Form 67. Consistency and evidence matter more than minor rate differences.

Can I claim DTAA benefits without hiring a CA, is it practical for a solo freelancer?

You can prepare the basics yourself, TRC, Form 10F, no PE letter, W 8BEN, and Form 67, many freelancers manage this with checklists. That said, a CA adds value when your client mix spans multiple countries, when there is PE ambiguity, or when an assessment notice arrives. Using a payments platform like Karbon Business also reduces the admin by generating compliant statements and e FIRA automatically.