When you send €10, €20, or €70, you rarely worry about the method. Small payments carry low risk.

But when you’re moving a larger or urgent sum, every factor matters: how much will it cost, how long will it take, and is it safe?

One of the most common questions is: Which is better, ACH or wire transfer? Both send money electronically, but they differ in speed, cost, and security.

This guide breaks down an ACH vs wire transfer comparison to help you choose the best option for your next payment.

What Is an ACH Transfer?

An ACH transfer is an electronic payment that moves money from one country to another using the Automated Clearing House network or similar local clearing networks abroad. Instead of sending money instantly, banks bundle these payments together and process them in groups, just like domestic ACH.

How does an international ACH transfer work?

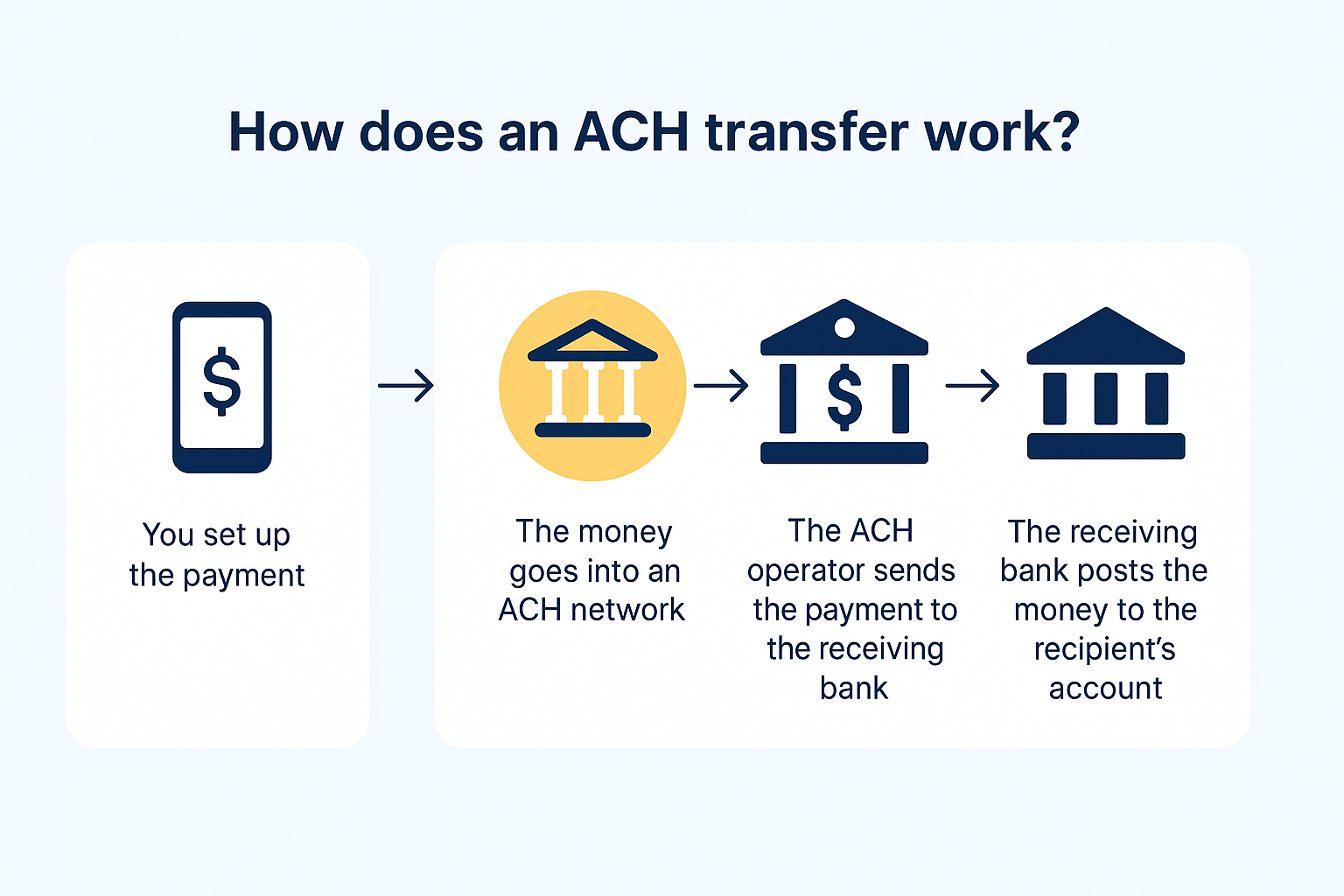

- You set up the international payment through your bank or payment platform.

- Your bank collects the payment details and sends them through its ACH operator or a partner network that connects to the recipient’s country.

- The payment instructions pass through local clearing networks in the receiving country.

- The recipient’s bank receives the instructions and credits the money to the recipient’s account.

This process usually takes 3 to 5 business days because it involves more checks, currency conversion, and cross-border banking partners.

International ACH transfers are commonly used for:

- Paying overseas contractors or freelancers

- Sending recurring pension or salary payments abroad

- Making international business payments when speed is not urgent

Because payments are processed in bulk and often use existing banking relationships, international ACH transfers are usually cheaper than wire transfers. But they can be slower and not all countries or banks support them.

What Is a Wire Transfer?

A wire transfer is another way to move money electronically, but it works differently. Instead of batching transactions, banks handle wire transfers individually and in real time. The money is sent directly from one bank to another through secure networks like SWIFT or Fedwire.

How Does International Wire Transfer Work?

- You tell your bank to send money and provide the recipient’s name, bank name, account number, and often a SWIFT code for international wires.

- Your bank checks the details and debits your account.

- The money moves directly through a secure network such as SWIFT for international transfers.

- If your bank does not connect directly, intermediary banks help pass the money along.

- The recipient’s bank receives the funds and credits the recipient’s account.

Wire transfers are faster than ACH. Domestic wires often clear the same day, while international wires can take 1 to 3 business days depending on the banks involved.

Wire transfers are ideal when you need to send large sums of money quickly. They are often used for:

- Closing real estate deals

- Paying large invoices to suppliers

- Urgent international transfers

- Sending funds for emergencies

Domestic wire transfers are usually completed within a few hours, often on the same business day. International wire transfers may take one to three business days, depending on time zones, currency exchange, and the banks involved.

Unlike ACH transfers, wire transfers come with a higher cost. Banks typically charge fees for both sending and receiving wires. Domestic wires usually cost $15 to $30, while international wires can cost $30 to $50 or more.

ACH vs Wire Transfer: Key Factors

1. Speed

- ACH Transfer: International ACH payments are possible but less common and can be slow. They often take three to five business days or longer, depending on the countries involved and the banks’ networks.

- Wire Transfer: Wire transfers are the standard for international payments. Funds typically arrive within one to three business days, sometimes faster if all details are correct and there are no hold-ups with intermediary banks.

2. Cost

- ACH Transfer: Some banks offer international ACH services through partners, but fees vary and may include currency conversion charges. The cost is usually lower than a wire transfer but not always by much once exchange rates and hidden fees are included.

- Wire Transfer: International wires cost more upfront. Sending money abroad by wire usually costs $30 to $50 or higher per transfer. The recipient’s bank may also charge to receive the funds, and currency conversion fees often apply.

3. Reversibility

- ACH Transfer: International ACH payments can sometimes be reversed if there is an error or fraud, but the process is complex and depends on the banks involved.

- Wire Transfer: International wires are generally final. Once the money leaves your bank, it is very difficult to recall. This makes accuracy extremely important.

4. Security

Both methods use secure global networks to protect your money during international transfers.

- ACH Transfer: International ACH is less common, but when available, it moves through trusted banking partners and regulated clearing houses. Payments can be slower, which sometimes makes stopping a suspicious transaction possible.

- Wire Transfer: International wires use global networks like SWIFT, which are reliable and secure. However, wire transfers are a common target for fraud, especially in international business. Always verify recipient details and instructions.

5. Typical Use Cases

- ACH Transfer: Some businesses use international ACH for payroll to overseas employees or paying international contractors when speed is not critical and cost savings matter.

- Wire Transfer: Wire transfers are the default choice for large international payments. They are used for paying suppliers abroad, purchasing property in another country, or sending urgent personal transfers where fast delivery is a priority.

Pros and Cons of ACH And Wire Transfer

Pros and Cons of ACH:

Pros and Cons of Wire Transfer:

When Should You Use ACH And Wire Transfer?

Choosing between an ACH vs wire transfer depends on how fast you need the money to arrive, how much you are sending, and how much you want to spend on fees.

When to Use ACH

- Paying employees through direct deposit

- Scheduling automatic bill payments

- Transferring money between your own accounts

- Sending non-urgent payments under a few thousand dollars

When to Use Wire Transfer

- Closing a time-sensitive business deal

- Paying a large invoice quickly

- Sending funds internationally where speed matters

- Buying real estate or vehicles

One common mistake is using a wire when an ACH would do the job just fine. For example, if you are paying your vendor every month, an ACH transfer saves money over time.

How Much Do You Pay For International Transfer?

Cost is often the deciding factor when comparing ACH vs wire transfer.

ACH Fees

- Many banks offer free incoming and outgoing ACH transfers.

- Some may charge a small fee for same-day or expedited ACH, usually $1–$5.

Wire Transfer Fees

- Domestic outgoing wire: $15–$30

- Domestic incoming wire: Some banks charge $10–$15

- International outgoing wire: $30–$50+

- Exchange rate markups may add hidden costs for international wires

Always check with your bank for exact fees because they vary widely.

ACH vs Wire Transfer: Quick Comparison Table

Final Thoughts

When it comes to ACH vs wire transfer, the right choice depends on your priorities. If you want to save money and can wait a few days, ACH is the better option for routine payments. If you need funds to arrive quickly or need to move large sums across borders, paying extra for a wire transfer may be worth it.

Before you send money, weigh the speed, cost, and level of urgency — and always double-check the details to avoid costly mistakes.

FAQs on ACH vs Wire Transfer

1. Which is safer, ACH or wire transfer?

Both are secure when used properly, but ACH has the advantage of being reversible in some cases. Wire transfers are final, so you must double-check recipient details.

2. Why are wire transfers so expensive?

Wire transfers require manual processing and real-time settlement between banks. The cost covers the secure network fees and administrative work involved.

3. Can I do an international ACH transfer?

Some banks offer international ACH, but it is less common and slower than an international wire. For urgent cross-border payments, wire transfers are still the standard.

4. How do I decide between ACH vs wire transfer for my business?

Use ACH for regular payroll and vendor payments where speed is not critical. Use wire transfers for large, time-sensitive payments or when dealing with international suppliers.