Let’s say you’ve secured an international order worth ₹37,50,000 (around $50,000).

The buyer won’t pay until 60 days after receiving the shipment. In the meantime, you need to cover:

• Production costs: ₹15,00,000 (around $20,000)

• Packaging expenses: ₹1,50,000 (around $2,000)

• Shipping charges: ₹2,25,000 (roughly $3,000)

That’s about ₹18,75,000 (roughly $25,000) you need to cover before payment arrives. Without enough working capital, your business is at risk of cash flow strain, affecting day-to-day operations.

With export finance, you can secure a loan or credit line to bridge that gap, letting you continue operations smoothly while waiting for the buyer’s payment.

What is Export Finance?

Export finance helps businesses manage the money side of their international sales. When you sell goods to customers in other countries, you often have to wait a while to get paid. In the meantime, you still have costs to cover, like production and shipping.

Export finance provides the funds you need to keep operations moving while you wait for payment. It's like a loan or credit line that covers the gap between sending goods and receiving international payment. With this financial support, businesses can keep running without cash flow problems.

It also lets exporters offer flexible payment terms to international buyers, like allowing them to pay in installments or later. This makes the deal more appealing to buyers, who are more likely to purchase if they have more time to pay.

Who Provides Export Finance?

When it comes to funding exports, there are different financial institutions and government-backed agencies. Here’s a closer look at a few important sources of export finance:

1. Commercial Banks

Commercial banks remain the most common source of export finance for Indian businesses. They offer both pre-shipment and post-shipment credit facilities tailored to the exporter’s needs.

Popular options include packing credit to fund raw materials and production costs, post-shipment credit against export bills, and bill discounting or negotiation for faster access to funds. Many banks also offer Pre-shipment Credit in Foreign Currency (PCFC), allowing exporters to borrow at competitive international rates.

Best banks in India like SBI, HDFC Bank, ICICI Bank, Axis Bank, and Bank of Baroda have dedicated trade finance teams to assist exporters across industries.

2. Export Credit Agencies (ECAs)

Export Credit Agencies (ECAs) help reduce the risks associated with international trade, particularly the risk of non-payment by foreign buyers.

How?

They offer insurance and guarantees that protect exporters and lenders. In India, the Export Credit Guarantee Corporation of India (ECGC) is the primary agency that provides these services.

ECGC insures around 40% of the total export credit disbursed by banks in India. This means that if a foreign buyer fails to pay due to issues like political instability, financial problems, or non-payment for other reasons, ECGC steps in to cover the loss.

- Premium Rate: ECGC charges a premium ranging from 0.06% to 0.13% of the shipment value, based on the risk level.

- Eligibility: Available to registered Indian exporters with creditworthiness involved in exporting goods or services.

- Claim Period: Claims for unpaid credit should be filed within 6-12 months after the due date (depends on the policy).

- Policy Renewal: Policies are renewable annually, and exporters must update credit risk information to maintain coverage.

3. Specialised Financial Institutions

The Export-Import Bank of India (EXIM Bank) is the country’s flagship institution dedicated to promoting cross-border trade and investment.

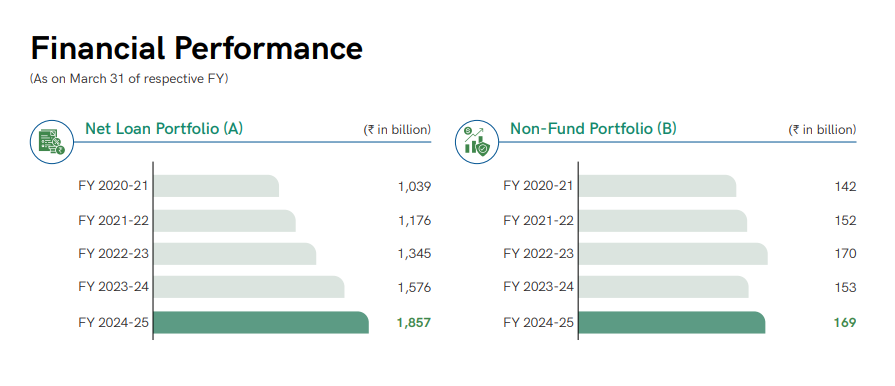

EXIM Bank’s net loan portfolio has grown from ₹99,400 crore in FY 2019-20 to ₹1,85,600 crore in FY 2024-25. This reflects its growing influence in financing exports and India’s international trade.

The bank provides both pre-shipment and post-shipment credit, as well as buyer’s credit and supplier’s credit.

In addition to its support for exporters, EXIM Bank also funds overseas investments by Indian companies and provides Lines of Credit (LoCs) to foreign governments and financial institutions. This indirectly boosts demand for Indian goods and services by fostering trade partnerships with other nations.

4. Non-Banking Financial Companies (NBFCs)

Non-Banking Financial Companies (NBFCs) have become an increasingly popular option for exporters, especially for MSMEs (Micro, Small, and Medium Enterprises) that may not have the required collateral or extensive paperwork for traditional bank loans.

NBFCs offer flexible financing solutions that help exporters unlock working capital tied up in unpaid export invoices. These solutions include invoice discounting, trade receivables financing, and supply chain finance. This flexibility allows businesses to access quick funds without having to wait for long approval processes or commit significant collateral.

Major NBFCs like Tata Capital and Aditya Birla Finance, as well as niche trade finance NBFCs, cater specifically to small and mid-sized exporters. In FY 2023-24, NBFCs provided 13.6% of India's GDP in credit, demonstrating their growing role in supporting the economy.

- Share of NBFCs in SCBs' Credit: NBFCs accounted for 24.5% of the outstanding credit provided by Scheduled Commercial Banks (SCBs) as of March 2024.

- Credit to MSMEs: NBFCs provided 7.6% of total credit to the MSME sector in 2023, helping to bridge the financing gap for smaller businesses.

By providing these tailored solutions, NBFCs have become vital players in ensuring that exporters, particularly in the MSME sector, can access the funds they need to grow and compete internationally.

5. Private Trade Finance Platforms

The rise of private trade finance platforms is transforming the way exporters access financing. These new-age fintech platforms provide fast, paperless options that are ideal for smaller exporters or businesses seeking quick working capital without the hassle of traditional bank loans.

Platforms like Drip Capital, KredX, and TradeCred specialize in offering export factoring, receivables financing, and short-term trade credit entirely online. This digital-first approach makes it easier for businesses to get paid faster, without needing to pledge significant collateral or wait weeks for traditional loan approvals.

This gap highlights just how crucial finance is for small exporters who may struggle with cash flow. Without access to timely financing, businesses can miss out on growth opportunities and face difficulties in managing their working capital. Export finance helps fill this gap, enabling businesses to handle the financial strain of international trade and expand globally.

What Are the Types of Export Finance?

Export finance can be broadly classified into several key types:

Pre-shipment Finance

- Also called packing credit.

- Funds working capital needs for procuring raw materials, manufacturing, packing, and shipping.

Post-shipment Finance

- Finance against export bills after goods are shipped.

- Includes export bill discounting, factoring, and advances against export receivables.

Supplier’s Credit

- Short-term credit extended to the overseas buyer by the exporter to boost sales.

Buyer’s Credit

- Credit provided to the foreign buyer by a bank or financial institution, secured by the exporter.

Export Factoring

- Selling export receivables to a factoring company for instant cash flow.

Benefits of Export Finance

Export finance offers multiple advantages:

- Improves Cash Flow: Get immediate funds without waiting for overseas payments.

- Competitive Edge: Offer better payment terms to buyers.

- Risk Reduction: Export credit insurance protects against buyer default or political risks.

- Business Expansion: Access to working capital helps you handle large or multiple orders.

Eligibility for Export Finance

Eligibility varies by lender and scheme, but generally includes:

- Registered exporter with a valid Import Export Code (IEC).

- Confirmed export order or Letter of Credit (LC).

- Satisfactory credit history and compliance with RBI/FEMA guidelines.

- For certain schemes, exporters must meet minimum turnover or shipment value requirements.

Terms and Conditions

While terms differ by bank or financial institution, some common points include:

- Interest rates may be lower than regular working capital loans.

- Loans are usually short-term, linked to shipment cycles.

- Collateral or personal guarantees may be required.

- Export proceeds must be repatriated within a specified period (generally 9 months).

Final Thoughts

Export finance is a lifeline for exporters aiming to compete globally. It frees up working capital, secures timely payments, and helps manage the risks of trading across borders. If you’re planning to expand internationally, talk to your bank, ECGC, or a trusted export finance advisor to choose the best solution for your business.

1. Why is export finance important for my business?

Export finance is crucial because it helps maintain steady cash flow while waiting for payments from international buyers. Without it, exporters can face financial strain covering production, shipping, and other costs before receiving payment. It ensures that your business can continue operations, accept larger orders, and expand internationally without worrying about cash flow gaps.

2. How does export finance reduce risks for exporters?

Export finance provides tools like credit insurance and guarantees to protect exporters from non-payment risks, whether due to political instability or buyer insolvency. For example, ECGC insures up to 40% of export credit disbursed by banks, ensuring that you aren’t left with major losses if something goes wrong with your international transactions.

3. Can export finance help my business grow?

Yes! Export finance gives your business the working capital to take on larger orders, accept longer payment terms, and manage multiple export transactions simultaneously. It allows you to offer flexible payment terms to buyers, making your business more attractive to international customers and boosting your competitiveness in the global market.

4. How do I choose the right export finance option for my business?

The right export finance option depends on your business's needs. Pre-shipment finance is ideal if you need funds for production before shipment, while post-shipment finance helps after goods have been shipped. NBFCs are a great option for MSMEs seeking quicker processing with less paperwork. Talk to your bank or financial advisor to find the solution best suited to your export volume and business goals.

5. How can I speed up the financing process for exports?

You can speed up the process by choosing digital trade finance platforms like Drip Capital or KredX, which offer fast, paperless financing options. These platforms provide quick access to working capital without the lengthy approval times of traditional banks, making them an excellent choice for small and medium-sized exporters looking to manage cash flow efficiently.