.png)

Establishing a business as a non-resident anywhere in the world isn’t easy.

There’s more paperwork. The rules are stricter. And the scrutiny is a lot more intense than what locals deal with.

Some countries like the U.S. still open the doors.

In 2023, immigrants started nearly one in five new businesses which is 19% of all new U.S. businesses, even though immigrants make up only about 14% of the population.

Whether you’re thinking of a café in Austin or opening a factory in New Jersey, the U.S. offers infrastructure, opportunity, and legal pathways to help non-residents build set their business in U.S.

All you need is the right direction.

Here’s your step-by-step guide to establish your business in U.S.

(This guide is for brick and motor businesses only. The ones that need a physical location in U.S.)

Step 1: Choose the Right Business Entity In U.S

First things first, if you want to start a business in the U.S., you need to pick a legal structure. That structure is called an entity. There are two entity options that don’t require you to be a U.S. citizen or resident.

Let’s understand the difference between both and the right structure for your business.

Here’s a quick takeaway:

• If you’re an NRI planning to start a café, boutique, grocery store, or wellness centre, an LLC is usually a good option. It’s easy to set up, and taxes are simpler.

• But if you’re aiming to raise money, bring in shareholders, or build a fast-scaling startup, then a C-Corp might make more sense. That’s the structure most investors look for, especially if you’re planning to issue stock or bring on venture capital.

LLC (Limited Liability Company)

A Limited Liability Company is one of the most flexible ways to start a business in the U.S. The name as it suggests protects your personal assets.

If your business takes on debt or gets sued, your house or savings won’t be at risk.

Latest data from the U.S. Small Business Administration shows there are over 33 million small businesses in the country. That’s 99.9 percent of all businesses in the U.S.

For these businesses established by non-resident Indian’s LLC is the perfect entity. Whether you're opening a store, running a consultancy, or selling products online, an LLC keeps things simple and clean.

Here’s why LLC might be the right fit:

• Pass-through taxation. The company doesn’t pay taxes separately. Profits go to you, and you pay tax just once on your personal return.

• Fewer rules. No need for annual meetings, complex filings, or too much red tape.

• Flexible setup. You can be the sole owner or have multiple members.

• Limited liability. Your personal assets stay safe even if the business runs into trouble.

If you're just getting started or want to keep your structure lean, an LLC is usually the way to go.

C-Corp (C-Corporation)

A C-Corp is a more formal business structure. It’s treated as a separate entity from you. That means the business exists on its own and can keep running no matter what happens with the founder.

Most high-growth startups prefer this structure, especially if they want to raise capital or issue shares to investors.

Here’s why a C-Corp might be the right fit:

• Separate taxation. The company pays corporate taxes, and you pay tax again if you take dividends. This is called double taxation, but it can be planned for.

• Investor-friendly. C-Corps are the standard for raising VC funding and offering stock options.

• Formal structure. You’ll need a board, company bylaws, and regular filings.

• No ownership limits. You can bring on as many shareholders as you want, including foreign ones.

If your goal is to grow fast, bring in outside money, or eventually sell or go public, a C-Corp gives you the structure and credibility to do it.

Another business structure that works in U.S is the S-Corporations. It is (benefits) But this structure is not available for NRIs.

IRS mentions:

"To qualify for S corporation status, the corporation must have only allowable shareholders which include individuals, certain trusts, and estates and may not include partnerships, corporations or non-resident alien shareholders."

Step 2: Applying for a U.S. Business Visa (E-2 or L-1)

This goes without saying- to start a business abroad you must get a business visa from that country. In U.S. There are 8-10 different business visas NRIs and Indians can apply for.

We will be discussing the two visas that can have the most advantages for businesses.

1. E-2 Treaty Investor Visa

The E-2 visa is a temporary visa for people who invest money in a U.S. business and plan to create jobs.

It is for countries with a trade treaty with the U.S. However, Indian citizens are not directly eligible since India doesn’t have an E-2 treaty. Some NRIs still qualify if they hold a second passport from a treaty country like Grenada or the UK.

Below are the requirements to be approved for the E-2 treaty Investor visa.

•Invest a “substantial” amount which can cost you around $100,000 or more and you must show the source of the find.

•You must own 50% of the business and manage day-to-day operations.

•Passive investments (like stocks or rental properties) are not considered for E-2 treaty visas.

To get an E-2 visa you must apply at a U.S. embassy or consulate and fill out the DS-160 form. They will also ask you to put together a solid business plan, showing proof of your investment, and invite you to an interview.

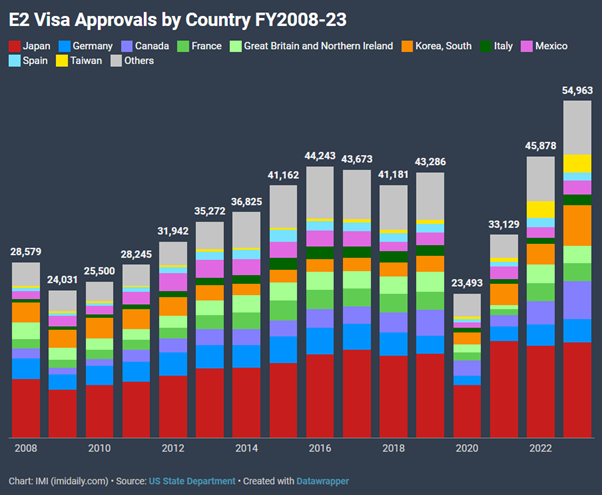

The good news?

Approval rates for E-2 visas have been going up. In 2023 54,000 E-2 visas were issued. It’s a rise of 20% from the previous year.

Source: IMI Daily

There are family perks too. Your spouse can apply for a work permit, and you can go to school in the U.S.

2. L-1 Intracompany Transferee Visa

If you’ve already got a business up and running outside the U.S., and you're thinking about expanding into the American market — the L-1 visa is best for you.

This visa lets you transfer your own employees, including yourself of course, to the U.S. to open and run a new branch, office, or affiliate. It’s built for business owners who want to grow across borders.

But there are a few things the U.S. government wants from you first.

What are the requirements?

• The U.S. government wants to ensure you're the right fit to build and lead a business there. That’s why they require at least 1 year of experience in a managerial or executive role within the past 3 years.

• Your foreign company (the parent or main branch) must remain active and have a direct relationship with your U.S. business. The U.S. entity should be a branch, affiliate, or subsidiary, not an entirely new or unrelated company.

• If you’re launching a new U.S. office, you must provide:

•A strong business plan

•Proof of office lease or premises

•Evidence of growth potential and market demand

Start by registering your U.S. entity. Then, submit Form I-129 to USCIS. Once it's approved, complete the visa process through a U.S. embassy or consulate.

The L-1A visa is valid for 1 year when setting up a new office. It can be extended to, up to 7 years, depending on how your business performs.

What other visa options do you have to set up a business in U.S?

If you don’t qualify for the E-2 or L-1 visa, you still have options. Many founders go for the B-1 Business Visitor Visa just to explore and set up meetings. And if you've got a bigger budget, the EB-5 investor visa lets you invest in a U.S. business and get on the path to a Green Card.

Step 3: Form Your U.S. Business Legally (State Registration and EIN)

The next step is to legally form your business in the U.S. This includes registering your company with a state, getting a federal tax ID (EIN), and completing new owner-reporting requirements.

Choose a State and Register the Business

In the U.S., businesses are registered at the state level. Each state runs its own rules, and the federal government stays out of it.

There’s a big win for businesses in this. States in U.S compete to attract businesses.

For example, more than 1.8 million businesses are registered in Delaware, even though the state has under a million people.

And Florida, Texas, and California continue to lead in small business growth because of their tax setups and local incentives.

How can you register your businesses in State of U.S?

Businesses are registered at the state level usually through the Secretary of State’s website.

You file formation documents like:

• If you're forming an LLC, you’ll file an Articles of Organization.

• If you're forming a C-Corp, you’ll file an Articles of Incorporation.

Businesses can pay the filing fee online or by mail. Once the application is verified and approved you will receive a certificate of confirmation from the state.

Tip: Check if your business name is available before filing. It must meet naming rules and include terms like “LLC” or “Inc.” Some states, like New York, also require publishing a notice in a newspaper.

Appoint a Registered Agent

If you don’t have a U.S. address, you need a registered agent in the state. This person or service receives official mail and legal documents on your behalf.

You can hire a registered agent service for a yearly fee. Many online services offer this during company formation.

Apply for an EIN (Tax ID)

An EIN is like a Social Security Number for your business. You need it to pay taxes, hire employees, and open a bank account.

If you don’t have a U.S. Social Security Number (SSN), fill out IRS Form SS-4 and apply:

•By phone (fastest): Call the IRS at +1-267-941-1099 (Mon to Fri, 6 am to 11 pm ET)

•By fax: Send Form SS-4 to the IRS. It takes about 2 to 3 weeks

•By mail: Not recommended. Too slow

Note: On the form, if you don’t have an SSN, write “N/A” in the SSN field.

File Beneficial Ownership Info (BOI)

Filing a Beneficial Ownership Information (BOI) report with FinCEN is a part of a new U.S. law, and it applies to all new businesses. You must report who owns and controls the company within 30 days of registration.

Businesses can file it for free, online.

Tip: Don’t skip it. There are penalties for not filing.

The state can request a few other documents or procedures like:

• A sales tax permit if you're selling goods

• Employer registration if you plan to run payroll

• A DBA (Doing Business As) name if you're using something different from your legal entity name.

By the end of this step, you should have your formation certificate, a registered agent, your EIN, and a filed BOI report.

Keep all these documents safe. You’ll need them when opening bank accounts, applying for permits, or talking to partners and vendors.

Step 4: Open a U.S. Business Bank Account as a Non-Resident

You’ll need a U.S. bank account to get paid and manage expenses.

All banks in U.S. don’t let non-resident business owners create an account with them. Big ones like Chase, Bank of America, and Wells Fargo usually do. You can call ahead and confirm.

Some banks will ask you to be physically present to open an account with them.

So, plan a U.S. trip with your company docs, passport, and ID. You’ll fill out forms, show proof of ownership, and sign a W-9 form. The process can take up to 3 weeks.

What You Need?

Bring these documents when opening the account:

•Company formation papers like Articles of Incorporation and your state registration certificate

•EIN confirmation letter from the IRS (Form CP 575)

•Details of owners holding 25% or more, including full name, birth date, passport, and address

•Two forms of ID for the person opening the account (one must be a passport)

•Proof of your personal address, such as a utility bill or bank statement from your home country

•Proof of U.S. business address. Some banks accept your registered agent’s address. Others ask for a lease or utility bill

Banks ask new NRI business account holders to deposit a few 100 dollars to open an account. You can send the money by wire or cashier’s check.

Paying Back to India

If your U.S. business needs to send money to India, whether it's to pay suppliers, freelancers, or your remote team, Karbon’s international payout solution makes the process simple and cost-effective.

Instead of using traditional SWIFT transfers, which come with $25 fees, currency conversion charges, and heavy documentation, Karbon lets you pay directly to an Indian recipient’s virtual USD account.

Since this is treated as a local payout in the U.S., you avoid the paperwork and skip FX commissions entirely. The only charge you will be paying is $1 per transaction (the standard local transfer fees).

Step 5: Get Local Business Licenses and Permits

Before you open your doors, you need to make sure you have the proper licenses and permits in place.

These vary depending on your business type and where you’re located. Some are federal, but most come from state or local authorities.

If you are a regulated industry you will have to apply for approval from federal authorities. These industries include alcohol, food production, firearms, or interstate transportation, etc. For restaurants, salons, gyms, or retail shops, you’ll deal with state and city-level permits.

Common Licenses and Permits includes:

• Business license or tax registration with your state and city

• Health permits if you’re handling food, issued after inspection

• Professional licenses for specific roles like stylists or trainers

• Liquor license for alcohol sales, which takes time to get

• Zoning clearance to make sure your business type fits the location

• Certificate of Occupancy from the fire or building department

• Environmental permits if you handle waste or chemicals

• Sign permits for any outdoor signage

• Building permits if you’re doing any remodelling

• Music or sidewalk seating permits, depending on your setup

Check your state’s business portal for exact requirements.

Sites like CalGold (California) or Texas Department of Licensing are good places to start. Also check with your city’s Small Business Office or Chamber of Commerce.

Step 6: Find and Lease a Business Space in the U.S.

Your business address affects everything including customer traffic, operations, and legal compliance. So, lock this down right.

Here’s what you should do:

Choose a location that fits what you're doing.

•A restaurant needs high foot traffic, preferably near offices or busy streets.

•A gym works well near residential areas or business parks.

•A factory should be in an industrial zone, not a commercial or residential one.

Before locking in a location, check zoning laws. These rules decide which businesses can operate in which areas. You can find this info on your city’s planning website or by calling the local zoning or building department.

Check the Building’s Legal Status

Make sure the space has a valid Certificate of Occupancy (CO). This proves it's approved for your type of business. If you are planning to add a kitchen, gym equipment, or ventilation, the building must meet local fire, plumbing, and accessibility codes.

If it’s an older building, you will have to upgrade it for ADA (Americans with Disabilities Act) compliance.

Commercial leases need a strong commitment financially. Read every clause.

Standard leases hold you responsible for property tax, insurance, and maintenance (called “triple net”).

Before you sign:

•Have a lawyer review it

•Ask for subleasing rights

•Add an exit clause if your visa gets denied

•Cap annual rent hikes

Get Your Permits and Insurance

If you are doing any kind of renovations, get your landlord’s sign-off and then apply for city permits. After the rennovation is done, the city will inspect and issue a new CO if needed. You can’t legally open without it.

Some businesses could need health permits, noise permits, or special use approvals.

And don’t forget about insurance:

•General liability (usually required by your landlord)

•Property insurance for equipment and inventory

•Workers’ comp if you hire employees

Handle all this early. It saves money, stress, and unwanted surprises down the line.

Step 7: Hiring Local Employees in the U.S.

If you plan to hire staff like cooks, sales reps, or trainers, you’ll need to follow U.S. labour rules from day one.

Start by getting your EIN and registering with your state’s tax department so you can handle payroll taxes.

For better management of staffs, you can get a payroll software. These tools are easy to manage. Some of the payroll tools we would recommend is Gusto, ADP, or Paychex. They are good

The next thing is to be specific about the job roles of the staff. Small businesses generally hire employees but label them as contractor.

If you treat someone like an employee but label them a contractor to avoid taxes or paperwork, that’s called misclassification. It can get you into legal trouble.

The IRS or your state can hit you with back taxes, penalties, and interest.

If you misclassify an employee as a contractor, here’s what the IRS can hit you with:

•$50 fine per W-2 you failed to file for the employee

•1.5% of wages paid, plus 40% of FICA taxes (Social Security and Medicare) the employee should have paid, and 100% of the employer’s FICA taxes

•Up to $1,000 per misclassified worker and 1 year in prison if the misclassification was intentional

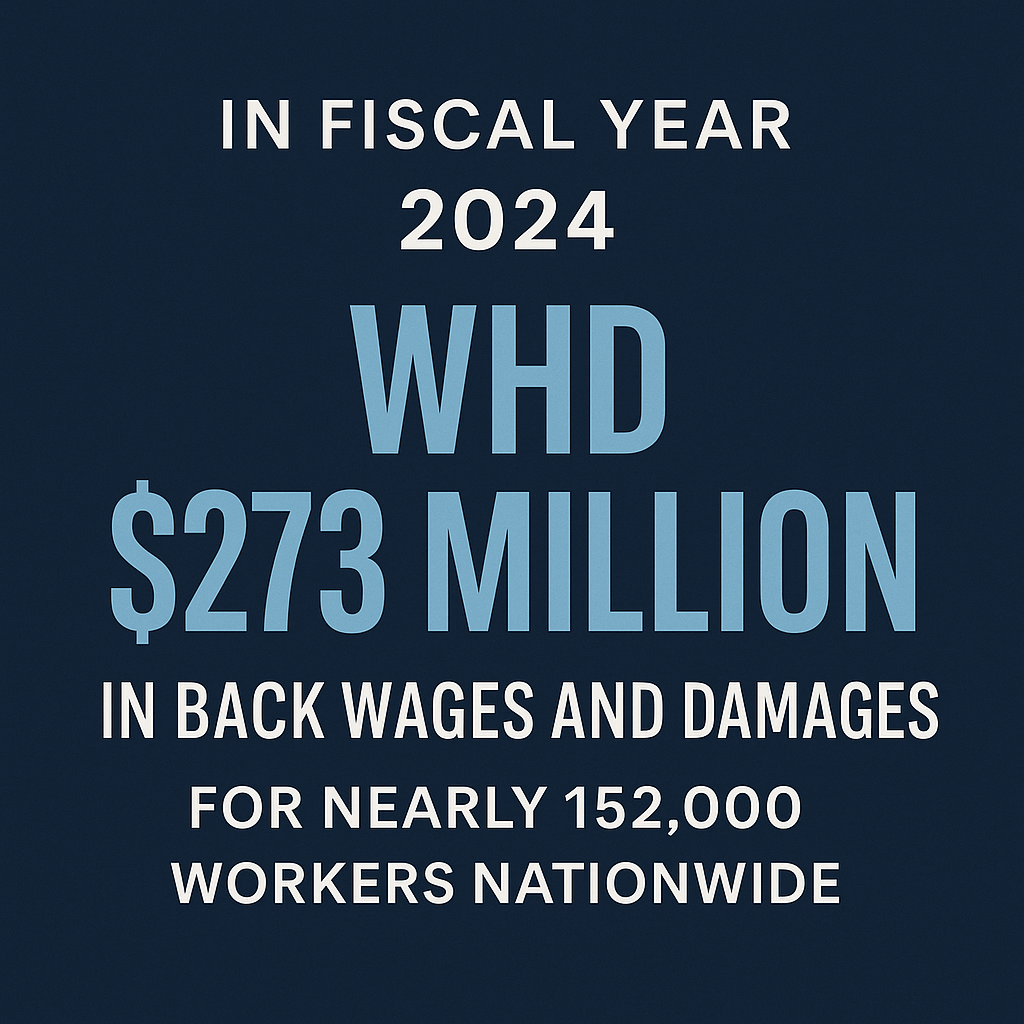

The U.S. Department of Labor (DOL) recovered $273 million in back wages for over 152,000 workers in 2024 due to unpaid minimum wage, overtime, or misclassification.

Here’s what you need to do:

•Collect Form I-9 and W-4 from every new hire

•Report new hires to your state within 20 days

•Pay at least the local minimum wage and overtime after 40 hours

•Post required labour law notices in the workplace

•Track work hours and pay employees on time

•Withhold taxes and file quarterly payroll returns

•Provide workers’ comp insurance, usually required even for one employee

Hiring legally protects your business and builds trust with your team. Get it right, and you’ll avoid issues later.

Step 8: Comply with Tax Obligations (Federal, State, and Local)

Once your business is up and running, taxes are part of the deal. In the U.S., taxes come in three layers: federal, state, and local. What you pay depends on your business structure and where you're operating.

Federal Taxes

If you’re a C-Corp, you’ll pay 21 percent corporate tax using Form 1120. If you take dividends, those get taxed again, usually 30 percent for non-residents unless a tax treaty reduces it.

If you have an LLC, profits usually pass directly to you. Single-member LLCs file Form 1040-NR, while multi-member LLCs file Form 1065 and issue a K-1 to each owner.

If your U.S. LLC is making money, you must file a tax return, even if you’re a non-resident.

Some businesses must pay an estimated taxes four times a year:

April 15, June 15, September 15, January 15

If you hire employees, you’ll handle:

•Income tax withholding

•FICA (Social Security and Medicare)

•FUTA (Federal Unemployment Tax)

LLC owners who work in the business can owe self-employment tax (15.3 percent). For non-residents, this depends on tax treaties. Talk to a CPA who understands international tax rules.

State Taxes

Every state play by its own rules. Florida and Texas have no state income tax. California, on the other hand, does. It charges C-Corps and LLCs differently.

They can collect sales tax if you sell products or taxable services. Register for a sales tax permit, then collect, report, and pay regularly.

Other state taxes include:

•Annual franchise tax

•LLC minimum tax (like California’s $800 fee)

•State unemployment tax

Even with no sales, you still need to file a zero return to avoid penalties.

Local Taxes

Your city or county can tack on more. You will also have to pay the following:

•Business license fees

•Extra local sales tax

•Property or equipment taxes

•Restaurant or gym-specific local taxes

Some cities, like New York City, even charge local payroll tax if you hire employees.

Bottom line: Stay compliant and file everything on time, because penalties add up fast.

Conclusion:

Starting a business in the U.S. as an Indian non-resident is doable if you take it step by step. Yes, there’s paperwork. Yes, there are rules. But with a proper guide and little help from a good CPA and immigration expert, you can launch confidently.