Avoid Payment Delays. Let Karbon Handle Intermediary Banks

We take care of routing, compliance, and documentation—so your funds arrive on time, every time.

.png)

International transactions usually take 1 to 5 days, and when the money arrives, it’s often less than what the sender paid for.

A big reason for this (apart from your bank’s own charges and exchange markups) is intermediary banks. They charge routing fees, can hold funds for compliance checks, and sometimes cause unexpected delays.

In this guide, you’ll learn exactly how intermediary banks work, why they’re needed, how much they charge, and what you can do to avoid surprises when sending or receiving money abroad.

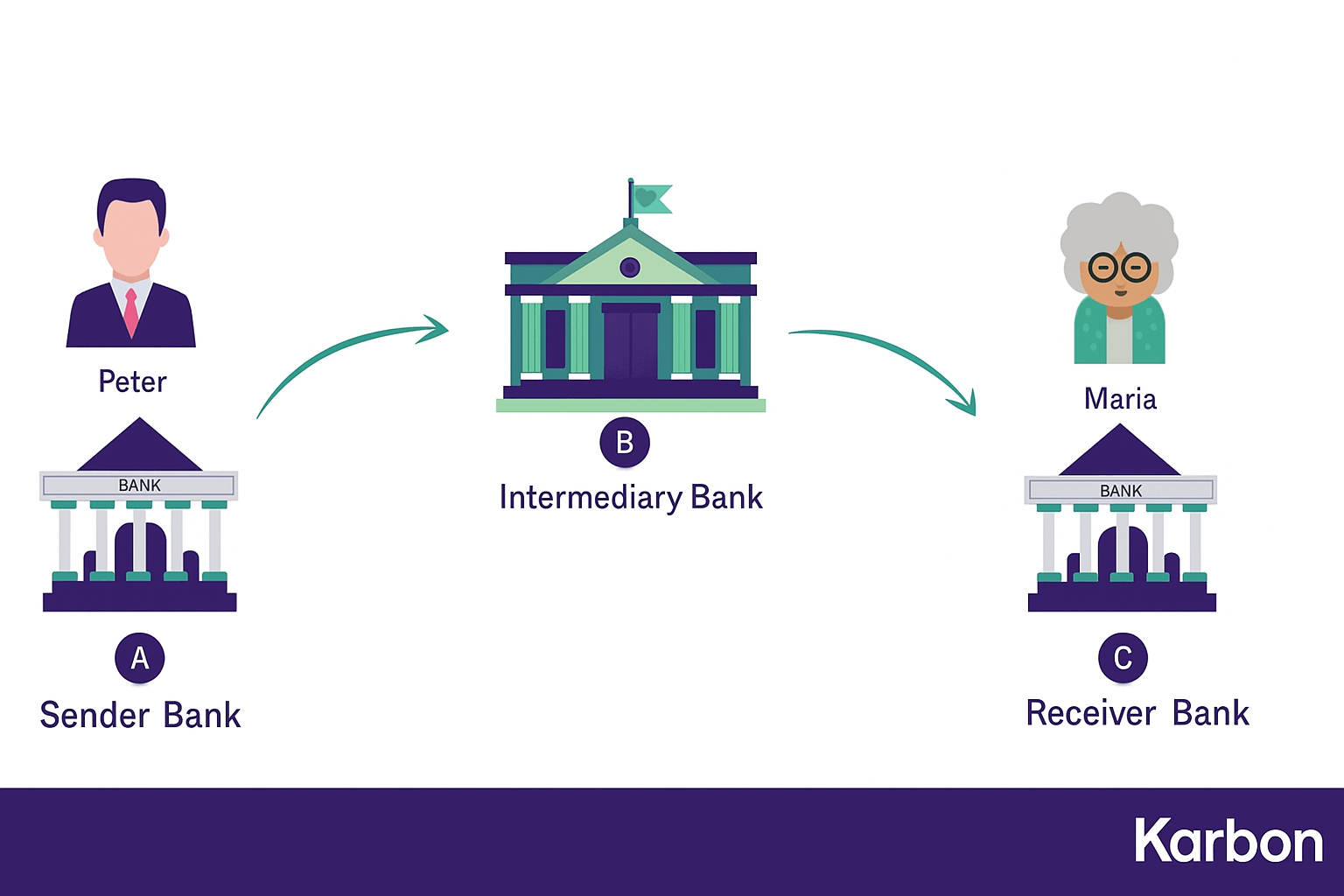

When you send money internationally, the funds don’t always move directly from your local bank to the recipient’s bank. This is because not all banks around the world have direct relationships with each other.

These transactions are carried out with one or more banks that act as a link between the sending and receiving banks. This middle bank is called an intermediary bank.

Let’s say David in the US wants to send $500 USD to a freelancer, Ravi, in India. David’s local bank in the US does not have a direct banking relationship with Ravi’s bank in India. So, David’s bank cannot directly push the money to Ravi’s bank account.

This is where an intermediary bank steps in.

Note: If David is sending USD 500 to a USD account that Ravi holds abroad (say, an NRE USD account), then there’s no need for converting the currency.

For businesses handling multiple international payments every month, manually tracking incoming transactions across bank statements can become difficult. Many finance teams now use bank statement OCR software to automatically extract payment data and simplify reconciliation.

Without an intermediary bank, David’s bank would have to maintain expensive accounts and partnerships with thousands of foreign banks. This is not practical for most banks.

This is the main question that keeps coming up when sending/ receiving money from abroad( and most probably the reason you are here): How much will they deduct from the amount I am about to receive?

Who will pay the bank fees- sender or receiver?

Intermediary banks don’t move your money for free. They charge a correspondent fee to handle, route, and clear your funds between banks that don’t talk to each other directly.

On top of that, the sending and receiving banks add their own charges too.

Here’s an approximate fee per transaction:

When you send an international wire transfer (especially using SWIFT), your bank’s wire transfer form or online banking portal usually has a section where you choose the charge option:

These are standard SWIFT charge codes, not just a random note. They’re built into the SWIFT MT103 payment message that banks use to communicate with each other.

Finding details concerning intermediary banks is useful in international payments. Below are some ways to obtain this information:

- If you require details regarding an intermediary bank, then your own bank is the most credible source. You may contact their customer care executives or relationship managers and ask for the relevant details like the intermediary bank’s SWIFT or IBAN. An MT103 document is the more technical term, you can ask for a SWIFT MT103 document and it will contain all the details of your international payment, including intermediary bank information. A lot of these financial institutions will advertise this information on their website or send it by email on request.

Look up websites that specialize in listing intermediary bank codes. These websites should allow you to enter the name of the banking institution or financial organization to receive the relevant SWIFT information. This strategy is mostly useful when you are aware of the account’s recipient and their respective bank but require the intermediary information to perform the transaction.

It is possible that the recipient’s bank already has an intermediary bank for these kinds of transactions. Request the recipient’s bank information to check if it has a corresponding bank and SWIFT code or other specific routing instructions. That way you can be sure the payment will reach its destination without delays.

Occasionally, some bank documents like invoices, payment confirmations, and statements may have the intermediary bank’s details. Ensure you check the documents for details like the routing number, SWIFT code, or the names of intermediary banks. If the recipient is the same, this will be helpful if you wish to make payments repeatedly.

Payment Service Providers, like Karbon, do not require you to worry about intermediary banks, as they tend to take care of that. PSPs tend to focus on intermediary payments and will have a network of banks to work with. So, instead of manually searching for intermediary bank details, with Karbon, you can feel confident knowing the transactions get routed properly.

Using these approaches can help maintain the efficiency and effectiveness of your international payments whilst reducing unnecessary hurdles.

For businesses engaged in global trade, especially those based in India, understanding intermediary bank charges can seem daunting—but it doesn’t have to be.

Karbon is made specifically for businesses that don't want the hassle of managing international payments not only because it is streamlined but it is also cost-effective. We also provide free FIRA and SWIFT MT103 copies which enable you to get a bird’s eye view of your international transaction.

With Karbon, you can simplify the entire process. From ensuring proper payment routing to eliminating unnecessary complexities, Karbon is the trusted partner for Indian businesses seeking efficient and reliable cross-border payment solutions.

Yes. If your wire instructions are incomplete, contain errors, or if the payment is flagged during compliance checks (for example, anti-money laundering or sanctions screening), the intermediary bank can hold, delay, or reject the funds. This is why it’s so important to use clear, complete SWIFT details, including correct beneficiary and bank info, to avoid your money getting stuck midway.

If your payment is delayed, the first thing you should do is contact your bank to confirm the details of the transaction, including the intermediary bank's information. If errors are found, request updated payment instructions. At the same time, inform the recipient so they can check with their bank if there are any issues on their side. Double-check all intermediary bank details before making a transaction to avoid future delays or rely on trusted payment solutions like Karbon, which manage intermediary bank requirements for you.

Yes. SBI uses intermediary (or correspondent) banks for most incoming foreign currency wires.

Normally, you don’t have to give intermediary bank details to the sender. When you want to receive an international wire, your Indian bank provides the full wire instructions. This includes:

You share these instructions exactly as given with the sender (the person or business overseas). When the sender fills out the wire form at their bank (or online), they just copy-paste or enter these details into the required fields.

Both terms are correct. When acting as a middle link between two banks that don’t have a direct relationship, HSBC acts as an intermediary bank — technically called a correspondent bank in banking terms. Large global banks like HSBC, Citibank, JPMorgan Chase, and Standard Chartered maintain vast networks of correspondent accounts so smaller banks can route cross-border payments through them.

International transactions usually take 1 to 5 days, and when the money arrives, it’s often less than what the sender paid for.

A big reason for this (apart from your bank’s own charges and exchange markups) is intermediary banks. They charge routing fees, can hold funds for compliance checks, and sometimes cause unexpected delays.

In this guide, you’ll learn exactly how intermediary banks work, why they’re needed, how much they charge, and what you can do to avoid surprises when sending or receiving money abroad.

When you send money internationally, the funds don’t always move directly from your local bank to the recipient’s bank. This is because not all banks around the world have direct relationships with each other.

These transactions are carried out with one or more banks that act as a link between the sending and receiving banks. This middle bank is called an intermediary bank.

Let’s say David in the US wants to send $500 USD to a freelancer, Ravi, in India. David’s local bank in the US does not have a direct banking relationship with Ravi’s bank in India. So, David’s bank cannot directly push the money to Ravi’s bank account.

This is where an intermediary bank steps in.

Note: If David is sending USD 500 to a USD account that Ravi holds abroad (say, an NRE USD account), then there’s no need for converting the currency.

For businesses handling multiple international payments every month, manually tracking incoming transactions across bank statements can become difficult. Many finance teams now use bank statement OCR software to automatically extract payment data and simplify reconciliation.

Without an intermediary bank, David’s bank would have to maintain expensive accounts and partnerships with thousands of foreign banks. This is not practical for most banks.

This is the main question that keeps coming up when sending/ receiving money from abroad( and most probably the reason you are here): How much will they deduct from the amount I am about to receive?

Who will pay the bank fees- sender or receiver?

Intermediary banks don’t move your money for free. They charge a correspondent fee to handle, route, and clear your funds between banks that don’t talk to each other directly.

On top of that, the sending and receiving banks add their own charges too.

Here’s an approximate fee per transaction:

When you send an international wire transfer (especially using SWIFT), your bank’s wire transfer form or online banking portal usually has a section where you choose the charge option:

These are standard SWIFT charge codes, not just a random note. They’re built into the SWIFT MT103 payment message that banks use to communicate with each other.

Finding details concerning intermediary banks is useful in international payments. Below are some ways to obtain this information:

- If you require details regarding an intermediary bank, then your own bank is the most credible source. You may contact their customer care executives or relationship managers and ask for the relevant details like the intermediary bank’s SWIFT or IBAN. An MT103 document is the more technical term, you can ask for a SWIFT MT103 document and it will contain all the details of your international payment, including intermediary bank information. A lot of these financial institutions will advertise this information on their website or send it by email on request.

Look up websites that specialize in listing intermediary bank codes. These websites should allow you to enter the name of the banking institution or financial organization to receive the relevant SWIFT information. This strategy is mostly useful when you are aware of the account’s recipient and their respective bank but require the intermediary information to perform the transaction.

It is possible that the recipient’s bank already has an intermediary bank for these kinds of transactions. Request the recipient’s bank information to check if it has a corresponding bank and SWIFT code or other specific routing instructions. That way you can be sure the payment will reach its destination without delays.

Occasionally, some bank documents like invoices, payment confirmations, and statements may have the intermediary bank’s details. Ensure you check the documents for details like the routing number, SWIFT code, or the names of intermediary banks. If the recipient is the same, this will be helpful if you wish to make payments repeatedly.

Payment Service Providers, like Karbon, do not require you to worry about intermediary banks, as they tend to take care of that. PSPs tend to focus on intermediary payments and will have a network of banks to work with. So, instead of manually searching for intermediary bank details, with Karbon, you can feel confident knowing the transactions get routed properly.

Using these approaches can help maintain the efficiency and effectiveness of your international payments whilst reducing unnecessary hurdles.

For businesses engaged in global trade, especially those based in India, understanding intermediary bank charges can seem daunting—but it doesn’t have to be.

Karbon is made specifically for businesses that don't want the hassle of managing international payments not only because it is streamlined but it is also cost-effective. We also provide free FIRA and SWIFT MT103 copies which enable you to get a bird’s eye view of your international transaction.

With Karbon, you can simplify the entire process. From ensuring proper payment routing to eliminating unnecessary complexities, Karbon is the trusted partner for Indian businesses seeking efficient and reliable cross-border payment solutions.

Yes. If your wire instructions are incomplete, contain errors, or if the payment is flagged during compliance checks (for example, anti-money laundering or sanctions screening), the intermediary bank can hold, delay, or reject the funds. This is why it’s so important to use clear, complete SWIFT details, including correct beneficiary and bank info, to avoid your money getting stuck midway.

If your payment is delayed, the first thing you should do is contact your bank to confirm the details of the transaction, including the intermediary bank's information. If errors are found, request updated payment instructions. At the same time, inform the recipient so they can check with their bank if there are any issues on their side. Double-check all intermediary bank details before making a transaction to avoid future delays or rely on trusted payment solutions like Karbon, which manage intermediary bank requirements for you.

Yes. SBI uses intermediary (or correspondent) banks for most incoming foreign currency wires.

Normally, you don’t have to give intermediary bank details to the sender. When you want to receive an international wire, your Indian bank provides the full wire instructions. This includes:

You share these instructions exactly as given with the sender (the person or business overseas). When the sender fills out the wire form at their bank (or online), they just copy-paste or enter these details into the required fields.

Both terms are correct. When acting as a middle link between two banks that don’t have a direct relationship, HSBC acts as an intermediary bank — technically called a correspondent bank in banking terms. Large global banks like HSBC, Citibank, JPMorgan Chase, and Standard Chartered maintain vast networks of correspondent accounts so smaller banks can route cross-border payments through them.

W-8BEN for Indian Freelancers: Upwork Guide to 0% Withholding

Swati Saraf

February 17, 2026

W-8BEN for Indian Freelancers: Upwork Guide to 0% Withholding

Swati Saraf

Join 2,000+ freelancers and SMEs already saving on international payments with Karbon.

Save 50% - Start Now